What makes biblical museum ministry donations tax-deductible is not the spiritual importance of the work, but the legal and operational facts that place a gift within the IRS rules for charitable contributions. Many Christian donors assume that if a museum is “biblical,” giving to it is automatically deductible. In practice, deductibility turns on the ministry’s tax-exempt status, how the gift is structured, and whether the donor receives a benefit in return.

Biblical museum ministries sit at an unusual intersection: they are educational institutions, evangelistic storytellers, preservation efforts, and public-facing cultural organizations. That complexity can bless the church, but it also creates avoidable donor risk. Wise giving asks both, “Is this faithful?” and “Is this properly handled?” Scripture commends integrity not only in our intentions but in our administration: “We aim at what is honorable not only in the Lord’s sight but also in the sight of man” (2 Corinthians 8:21).

The core legal test is qualified charitable status

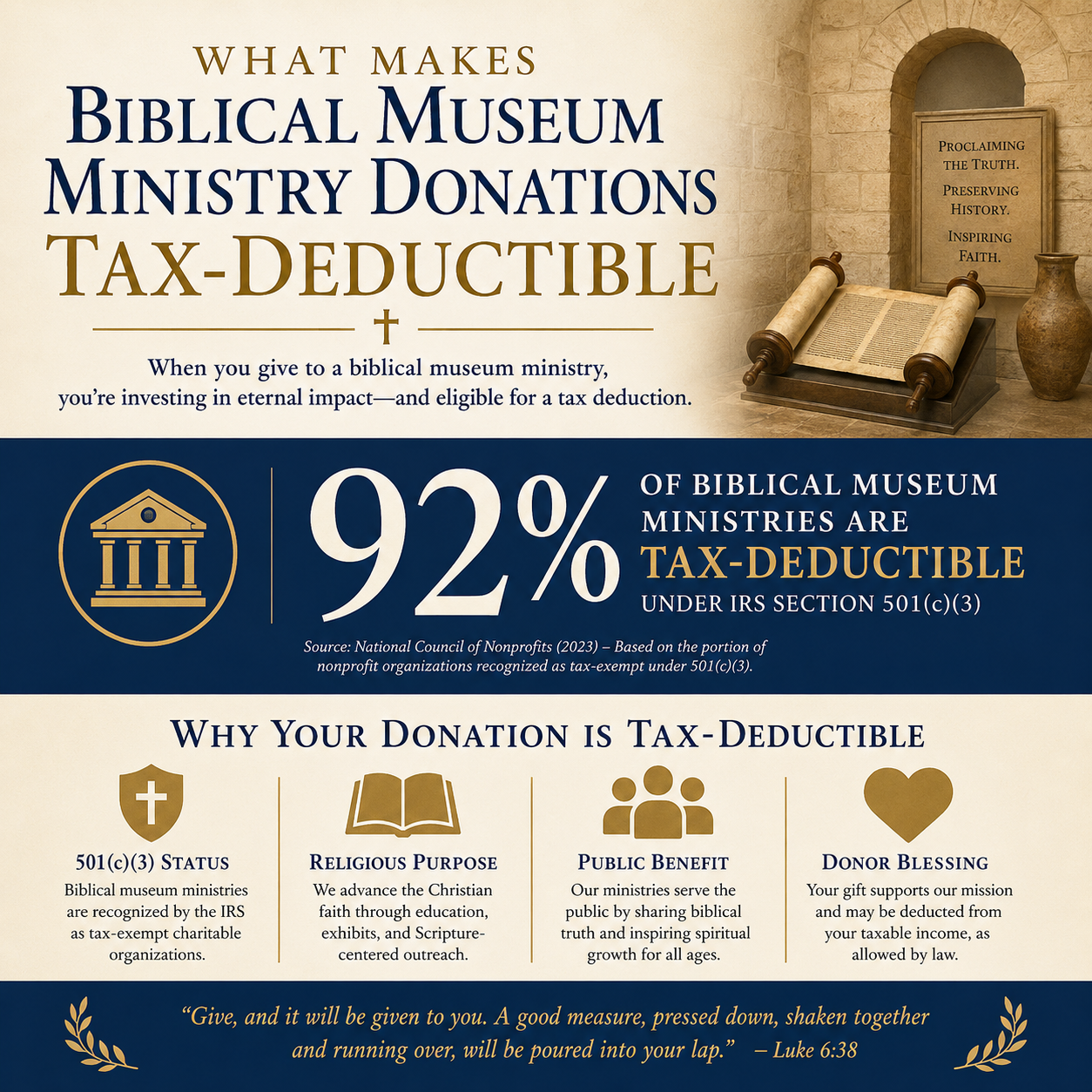

Most tax-deductible giving begins with IRS recognition

In the United States, a donation is generally tax-deductible only when it is made to a qualified organization under Internal Revenue Code Section 170. For most ministries, that means the recipient is recognized as tax-exempt under Section 501(c)(3) and is eligible to receive deductible charitable contributions. The IRS maintains a searchable database donors can use to confirm an organization’s status and eligibility before giving, including whether the organization has had its status revoked. IRS Tax Exempt Organization Search.

What this means in practice is straightforward: if a biblical museum ministry is not a qualified 501(c)(3) (or is a related entity that is not eligible to receive deductible gifts), the donor’s good intentions do not create a deduction. Some museums operate with multiple entities—an operating nonprofit, a supporting foundation, a separate LLC for retail or media work. Deductibility is determined at the entity level, not at the brand level.

Church affiliation does not automatically extend deductibility

Christian donors often ask whether a museum ministry “counts like a church.” Some museums are formally integrated with a church, but many are not. Even when a museum’s theological commitments are explicit, the legal classification is typically as a public charity with educational purposes rather than a church. The practical lesson is not suspicion; it is clarity. Donors should know which legal entity is receiving the gift and whether that entity can provide a contemporaneous written acknowledgment for the contribution.

For donors who want a broader lens on what strong biblical museum ministries tend to look like—doctrinal clarity, disciplined governance, and credible public claims—our work at Most Trusted tracks those patterns across Biblical Museum Ministries as a category with distinct risks and distinct opportunities for Christian witness.

Deductibility hinges on the difference between a gift and a purchase

Quid pro quo rules apply to museums in predictable ways

A contribution is deductible to the extent it is a gift rather than a payment for goods or services. Museums regularly offer benefits that blur that line: admission tickets, membership levels, donor events, exhibit openings, catalogs, or special tours. The IRS treats these as “quid pro quo” contributions when part of the donor’s payment secures a benefit in return. The deductible portion is generally limited to the amount that exceeds the fair market value of the benefit. The IRS explains this framework and the required disclosure rules for charities. IRS guidance on quid pro quo contributions.

Christians genuinely disagree about whether certain museum benefits are spiritually “neutral.” The IRS question is narrower: did the donor receive something of measurable value? A gala dinner is rarely “just a ministry event” for tax purposes. A membership that provides free admission is not the same as a donation with no return benefit, even if the donor’s motive is philanthropic.

When a museum membership is partly deductible

Museum memberships often illustrate the rule best. If a donor pays for a membership that includes tangible benefits—admission, discounts, parking, store credits—the ministry should disclose the fair market value of those benefits, and the donor can generally deduct only the amount above that value. If the ministry cannot or will not provide a clear disclosure, the donor is left to guess. That is not a minor administrative issue; it is a test of whether the organization is willing to be plain and accountable.

Noncash gifts require disciplined documentation and credible valuation

Artifacts, collections, and intellectual property are not casual donations

Biblical museum ministries sometimes receive noncash gifts: rare books, coins, ancient Near Eastern artifacts, original artwork, archival collections, or rights to educational media. These gifts can be spiritually meaningful and strategically important, but they raise serious tax and ethical questions. The IRS requires more documentation as the claimed value rises, and qualified appraisals may be required for certain contributions. Donors should treat this as an act of stewardship, not bureaucratic nuisance. The IRS outlines the framework for noncash charitable contributions and the documentation expected. IRS Publication 561.

Because museum ministry is connected to public history, donors should also consider reputational and legal risk. Provenance questions, import restrictions, and cultural heritage concerns have shaped the museum field for years. Donors are not typically responsible for a museum’s acquisition policies, but donors can unintentionally underwrite practices that later bring public scandal and weaken Christian credibility. Verification and transparency are not optional for a public-facing institution that speaks in the name of biblical truth.

Use-related rules can limit deductibility

The tax treatment of noncash gifts can also depend on whether the charity’s use is related to its exempt purpose. For museums, the ministry’s “related use” of a donated item—exhibition, preservation, educational programming—can matter for how deductions are calculated in certain circumstances. Donors should not attempt to improvise this analysis. When a gift involves significant value, professional tax counsel is a normal part of faithful administration.

- Confirm the receiving entity is eligible to receive tax-deductible gifts.

- Ask what benefits, if any, are provided in exchange for the gift.

- Request written acknowledgment that reflects IRS requirements.

- For noncash gifts, obtain appropriate valuation support and forms.

- Clarify any restrictions and ensure they are accepted in writing.

Restricted gifts must be handled with governance strength and clarity

Restrictions protect donor intent but increase operational demands

Many donors give to biblical museum ministries with a specific purpose in mind: a traveling exhibit, conservation work, scholarship programs for students, translation projects, or the acquisition of an important collection. Restricted gifts can be a virtue because they protect donor intent and focus resources. They also create compliance obligations. A ministry that accepts restrictions must be able to track them, honor them, and report on them with accuracy.

The harder question is whether a ministry’s systems match its ambitions. Across our verification work at Most Trusted, the ministries that meet The Most Trusted Standard tend to show basic competence in fund accounting, clear gift acceptance policies, and board-level oversight that does not treat donor restrictions as administrative inconvenience. These are not cosmetic matters. Mishandled restrictions can become legal exposure, pastoral scandal, and a direct contradiction of Christian teaching about truthfulness.

Written acknowledgments and disclosures are spiritual integrity in administrative form

Deductibility often turns on paperwork donors do not see until tax season. A contemporaneous written acknowledgment, a clear description of what was given, and a statement about whether goods or services were provided in exchange are not mere formalities. They are part of the moral discipline of handling other people’s money faithfully. When ministries are careless here, donors are forced into unnecessary risk, and the ministry signals that it has not internalized the weight of public trust.

Donors seeking a wider field of ministry practices that help prevent these failures—gift acceptance policies, disclosures, governance discipline, and transparent reporting—often find clarity by comparing organizations within How to Give Wisely to Biblical Museum Ministries, where the donor questions are concrete rather than aspirational.

Tax deductibility is not a holiness test, but it is a trust test

Deductible does not mean verified, and verified does not mean perfect

A ministry can be fully tax-compliant and still be spiritually shallow, historically careless, or ethically compromised in how it acquires items or frames contested scholarly claims. The opposite is also true: a ministry can be doctrinally serious and culturally constructive while still having underdeveloped administrative practices that expose donors to risk. Christian donors should resist the false comfort that the IRS confers spiritual credibility.

What this means in practice is that deductibility is the beginning of due diligence, not the end. Mature stewardship asks whether the ministry is honest in its public claims, careful with restricted funds, governed by accountable leaders, and transparent about results and setbacks. That is the kind of integrity the church should want in institutions that represent Scripture in the public square.

Where Most Trusted fits for donors who want confidence

Most Trusted exists because many donors have learned that sincere Christian language can coexist with weak controls. We evaluate ministries against The Most Trusted Standard, a 15-criteria framework that examines faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. Our aim is not to replace a donor’s prayerful discernment, but to strengthen it with verifiable evidence, documented policies, and patterns that hold under scrutiny.

For biblical museum ministries in particular, donors are supporting institutions that speak publicly about history, evidence, and truth. That public posture increases the importance of internal rigor. A museum that wants to persuade skeptical visitors should be especially unwilling to cut corners in financial reporting, provenance disclosure, board independence, or donor communications.

FAQs for What makes biblical museum ministry donations tax-deductible

Are donations to a biblical museum always tax-deductible?

No. A gift is generally tax-deductible only if it is made to a qualified organization eligible to receive deductible charitable contributions, and only to the extent it is not a payment for goods or services. Donors should confirm the receiving entity’s status in the IRS Tax Exempt Organization Search and keep the ministry’s written acknowledgment for their records.

If we receive museum tickets or membership benefits, can we still deduct the gift?

Often, yes, but typically only the portion that exceeds the fair market value of what was received. Museums should disclose the value of benefits for quid pro quo contributions. If the ministry cannot clearly separate the gift from the benefit, the donor is left with uncertainty at tax time and should consider giving in a form that does not include material benefits.

Stewardship that honors both the gospel and the public trust

Biblical museum ministry donations become tax-deductible through qualified charitable status, careful separation of gifts from purchases, and disciplined documentation—especially when benefits, restrictions, or noncash assets are involved. For Christian donors, the deeper opportunity is to support institutions that handle money and truth with the same seriousness. When museum ministries operate with integrity that is visible in their governance and their records, they strengthen not only a deduction, but a witness.