What financial statements biblical museum ministries should share is not a cosmetic question about communications. It is a stewardship question about whether donors can verify the ministry’s handling of resources entrusted for the public witness of Scripture, the preservation of artifacts, and the formation of Christian imagination.

Museum ministries sit at a complicated intersection: education, scholarship, public programming, fundraising, and sometimes contested cultural debates. That complexity makes transparent financial reporting more necessary, not less. When financial statements are absent, selectively disclosed, or difficult to interpret, donors are left to infer integrity from branding and storytelling. Mature Christian giving deserves better.

Why museum ministry financial transparency is a theological and fiduciary obligation

Stewardship is measurable

Scripture consistently ties faithfulness to accountable stewardship. Jesus’ parable of the talents assumes that resources are entrusted, deployed, and assessed with evidence (Matthew 25:14–30). For donors, financial statements are not a demand for control; they are a means of testing whether an organization’s public claims cohere with its financial reality.

In the nonprofit context, the baseline expectation of disclosure is also established in law and in the common standards of charitable oversight. The IRS requires tax-exempt organizations to file an annual information return, and many ministries make that filing accessible through their own sites for donor clarity. The public availability of these filings is well-established; for example, the IRS explains public inspection expectations for exempt organization returns on its website (IRS).

Trust is built with verifiable documentation, not assurances

Across our verification work at Most Trusted, we observe that the most credible ministries do not treat financial transparency as a donor relations tactic. They treat it as a normal expression of integrity. They publish the same core statements year after year, provide notes that help a non-specialist interpret them, and avoid reporting choices that obscure related parties or restricted funds.

For readers seeking broader context on the distinct responsibilities and risks in this sector, we address them in Biblical Museum Ministries with attention to both mission and public trust.

The baseline set every biblical museum ministry should publish annually

Audited financial statements when scale and complexity warrant it

The gold standard for a mature museum ministry is an annual independent audit by a licensed CPA firm, with audited financial statements posted publicly. An audit does not guarantee virtue; it does provide a higher level of assurance that the statements are materially correct, prepared according to appropriate accounting standards, and supported by evidence tested by an independent party.

Some ministries are small enough that an audit may be disproportionate in cost. In those cases, donors can reasonably expect at least a reviewed financial statement (a CPA review provides limited assurance) and a clear explanation of why the ministry has not yet moved to an audit.

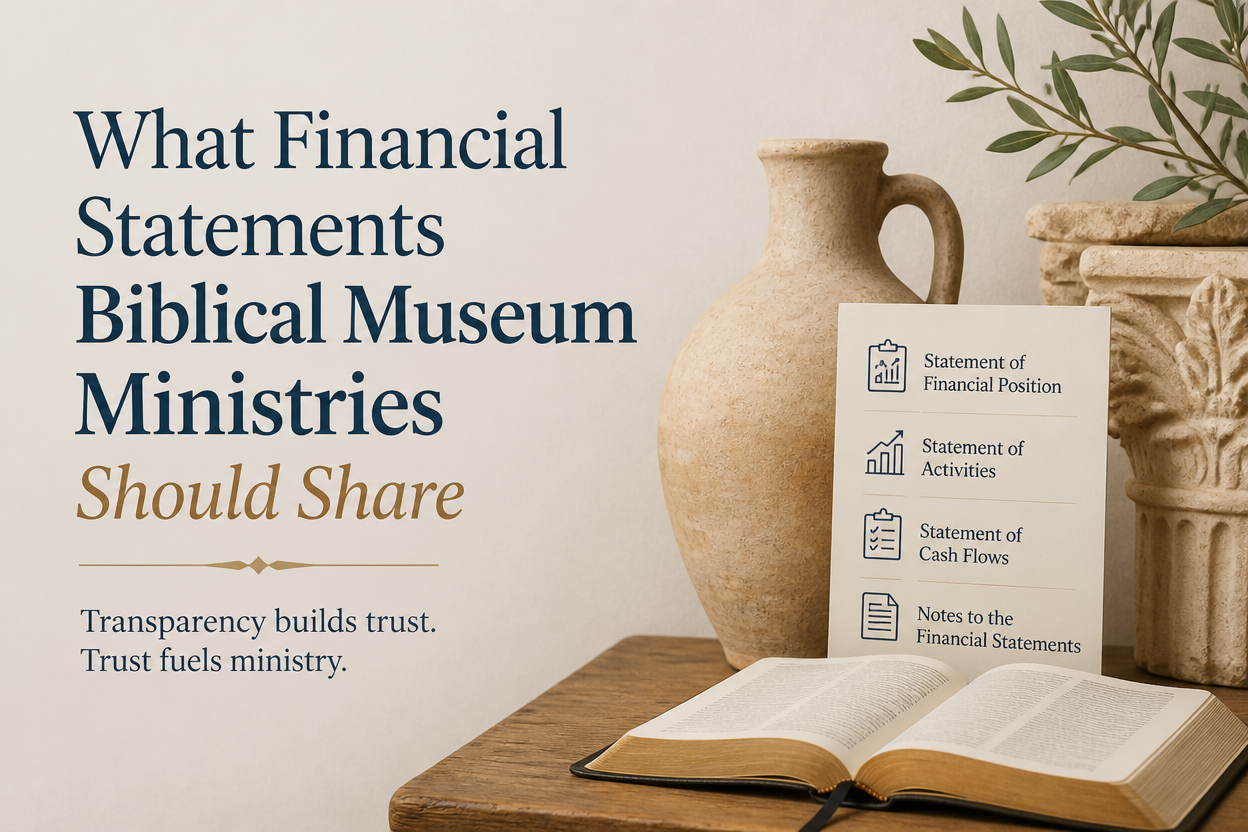

At minimum, publish these four statements

When donors ask what financial statements biblical museum ministries should share, we start with the basic package that permits meaningful evaluation without requiring donors to be accountants. A ministry should publish:

- Statement of financial position (balance sheet): assets, liabilities, and net assets, with clear classification of net assets with and without donor restrictions.

- Statement of activities (income statement): revenues and expenses by nature and, ideally, by function.

- Statement of functional expenses: a clear view of program, management, and fundraising allocations, along with the underlying expense categories.

- Statement of cash flows: the difference between accrual-based surplus and actual liquidity.

- Notes to financial statements: the narrative disclosures that often contain the most donor-relevant information.

When these documents are presented together, donors can evaluate solvency, sustainability, and whether program claims are supported by spending patterns. When one is missing, interpretability collapses.

The disclosures donors should expect in the notes and supporting schedules

Restricted funds and the realities of donor intent

Museum ministries often receive restricted gifts for acquisitions, exhibitions, capital projects, or endowment-like purposes. A financial statement without clear accounting for restricted funds can inadvertently mislead. Donors should be able to see: what restrictions exist, how restricted funds are released, and whether the ministry is carrying restricted balances that have not yet been deployed for their intended purpose.

This is not merely technical. It speaks to honesty before God and neighbor: “Moreover, it is required of stewards that they be found faithful” (1 Corinthians 4:2). Faithfulness includes honoring the terms under which gifts were given.

Related party transactions and conflicts of interest

The museum ministry world can include affiliated entities, founder relationships, and overlapping boards. Donors should expect transparent disclosure of related party transactions in the notes: leases, consulting arrangements, shared services, or any compensation paid to entities connected to insiders. These disclosures are not accusations; they are a normal safeguard that protects both the ministry and the donor community.

For a donor, a related party transaction is not automatically disqualifying. The questions are whether it is disclosed, approved with appropriate conflict-of-interest procedures, priced at fair market value, and documented in board minutes.

Interpreting statements for museum-specific financial realities

Collections accounting and the question of valuation

Museum collections raise unique accounting questions. Many museums do not capitalize collections in the same way they capitalize buildings or equipment, and valuations may not appear as assets in a straightforward manner. Donors should not assume that a balance sheet lacking a large “collection asset” indicates an absence of holdings. Instead, donors should look for a clear collections policy, disclosure about acquisitions and deaccessions, and whether the ministry follows recognized museum ethics for collections care.

What this means in practice is that donors should ask how the ministry funds collections care: conservation, storage, security, and documentation. These costs are ongoing, and they often do not carry the same fundraising appeal as new exhibits. Financial statements should help donors see whether the ministry is maintaining what it already holds.

Capital projects, debt, and liquidity

Many museum ministries undertake large capital projects: new buildings, renovations, immersive exhibits, or major technology investments. These projects can be mission-advancing and financially hazardous at the same time. Donors should look for clear disclosure of debt terms, covenants, interest rates, and maturity schedules in the notes, as well as the ministry’s liquidity profile.

Liquidity has become a central question in nonprofit resilience. The Federal Reserve has documented that many households would struggle to cover an unexpected expense, illustrating how quickly liquidity constraints shape real decisions (Board of Governors of the Federal Reserve System). Ministries are not households, but the analogy is instructive: cash constraints determine what can actually be sustained.

Donors should watch for warning signs that are common in capital-heavy organizations: repeated operating deficits covered by borrowing, unusually aggressive revenue projections tied to attendance growth, or heavy reliance on a small number of large gifts without a clear plan for diversification.

How ministries should communicate financial statements without manipulating donor perception

Do not reduce stewardship to a single ratio

Christian donors often ask for a simple metric: “What percentage goes to programs?” A statement of functional expenses helps, but it cannot bear the whole weight of moral evaluation. Museum ministries must invest in governance, compliance, security, collections care, and development. Underfunding these functions can degrade program integrity over time.

Leaders in nonprofit evaluation have criticized simplistic overhead fixation for years. The “Overhead Myth” letter, signed by Charity Navigator, GuideStar, and the Better Business Bureau Wise Giving Alliance, argues that overhead ratios are a poor proxy for impact and can distort nonprofit behavior (Charity Navigator).

Provide an accessible financial narrative anchored to the statements

Donors benefit when a ministry offers a short narrative that explains major year-over-year changes: a capital campaign, a new exhibit, an expansion in educational programming, a loss of a major grant, or an increase in security costs. The credibility test is whether that narrative is anchored to the published statements and notes, not to selective numbers pulled out of context.

This is also where accountability and transparency standards matter. We evaluate ministries against The Most Trusted Standard, a 15-criteria framework spanning faith commitments, financial integrity, governance, and transparent reporting. The goal is not to pressure ministries into performative disclosure, but to encourage practices that allow donors to give with confidence and to protect the public witness of Christian work. For donors who want a broader framework for these expectations, we address the underlying principles in Accountability and Transparency in Biblical Museum Ministries.

FAQs for What financial statements biblical museum ministries should share

Is a Form 990 enough, or should a museum ministry also publish audited statements?

A Form 990 is a meaningful baseline because it is standardized and widely comparable, but it is not a substitute for audited financial statements in larger or more complex organizations. Donors should prefer ministries that publish both: audited statements for accounting rigor and a Form 990 for standardized disclosure of governance, compensation, and related organizational information.

What if a museum ministry says publishing financial statements could create security risks?

Security concerns can be legitimate for museums, especially regarding detailed information about collections and physical infrastructure. But that concern rarely requires withholding core financial statements. A prudent approach is to publish standard statements and notes while avoiding operational details that would reasonably increase risk. If a ministry declines to publish statements entirely, donors should ask for a concrete explanation of what specific risk is being mitigated and why narrower redactions would not address it.

What faithful transparency makes possible

When biblical museum ministries publish clear, complete financial statements, donors can ask better questions: not only whether a ministry is solvent, but whether it is sustainable, governed well, and truthful about the costs of its calling. Transparency does not eliminate disagreement about strategy or method, but it places those disagreements on the firm ground of shared facts. That is a form of neighbor-love in the financial life of the church.