What financial audits Christian adoption ministries should complete is not a technical question reserved for accountants. For Christian donors, it is a stewardship question: whether the ministry entrusted with vulnerable children is willing to be examined in the light, to be corrected where needed, and to handle sacred responsibilities with verifiable integrity.

Scripture treats financial faithfulness as a moral matter, not mere compliance. Jesus repeatedly ties money to the orientation of the heart (Matthew 6:21), and the early church took pains to administer gifts in a way that would be honorable not only before the Lord but also before people (2 Corinthians 8:20–21). Adoption and family-preservation work adds another layer: the moral weight of decisions that affect a child’s life trajectory, often across borders and legal systems. Mature donors should expect ministries to meet that weight with transparent, third-party assurance.

Why audits matter more in adoption ministry than in many other causes

Christian adoption ministries operate where compassion, legal complexity, and trauma intersect. Money moves across programs that can include counseling, home studies, travel support, grants, placement services, post-adoption care, and in some cases international partnerships. Each of those activities carries distinct financial risks: restricted gifts that must be honored, client funds that must be segregated, vendor relationships that must be arms-length, and program claims that must be grounded in evidence.

What this means in practice is that donors should treat a ministry’s audit posture as a window into its broader posture toward accountability. An organization can publish inspiring stories and still mishandle restricted funds, fail to reconcile cash, or maintain internal controls that would not withstand even modest scrutiny. The question is not whether a ministry is sincere. The question is whether it is governed in a way that anticipates temptation, error, and the pressures that accompany emotionally charged giving.

Adoption-related revenue streams create specific risks

Many adoption-related organizations rely on a mixture of donations, grants, program service revenue, and, at times, pass-through funds intended for specific families. Those streams can blur boundaries unless the ministry maintains clear accounting treatment and documented policies. Donors should be especially attentive to how an organization distinguishes between charitable contributions and fees for services, and how it protects families from conflicts of interest in a process where decisions can feel existential.

Donor confidence is not the same as donor sentiment

Christian donors often give to adoption ministries because the biblical mandate to care for the fatherless is clear, and because the stories are compelling. Yet the field has had to reckon with real failures: perverse incentives tied to orphanage funding, weak safeguarding, and financial opacity that hides unhealthy practices. The risk is not hypothetical. The U.S. Department of Justice has documented the scale of nonprofit fraud across the sector through its investigative work and public reporting, even as most nonprofits act in good faith (U.S. Department of Justice).

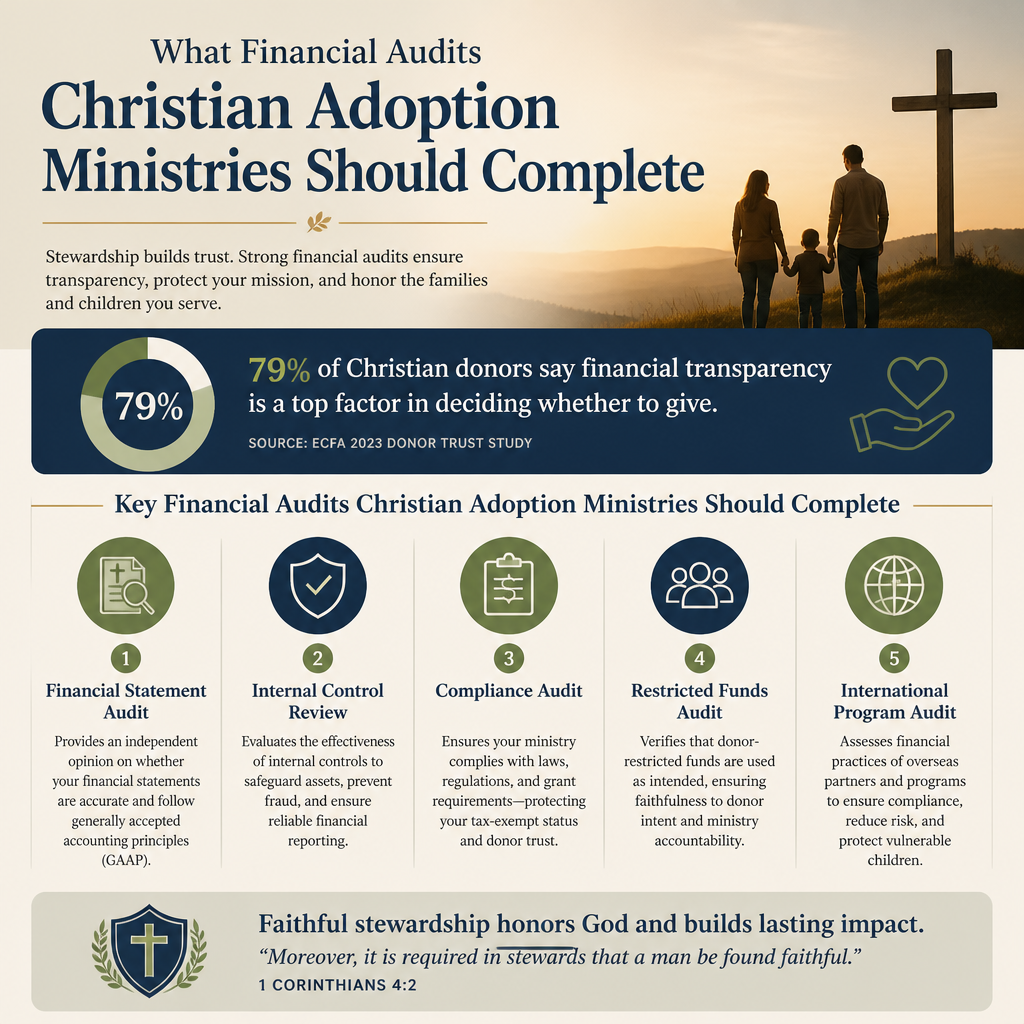

The baseline audit every serious ministry should treat as nonnegotiable

For most established Christian adoption ministries, the financial statement audit is the foundational assurance engagement. A proper audit, performed by an independent CPA firm under recognized auditing standards, tests whether the financial statements are fairly presented and whether material misstatements are likely to be detected. It also typically surfaces internal control findings that a board should treat as governance priorities, not as administrative inconveniences.

We recommend that donors look for audited financial statements that are current, complete, and readable. A ministry’s willingness to publish them is not a guarantee of health, but an unwillingness to do so should raise questions. The ministries that meet The Most Trusted Standard tend to treat audited statements as part of their public witness, not as an internal document to be shared only when pressed.

Audit, review, compilation are not interchangeable

Some organizations publish a CPA “review” or “compilation” and speak of it as an audit. Donors should know the difference. An audit provides the highest level of assurance; a review provides limited assurance; a compilation provides none. These terms have specific meanings in the accounting profession, and the engagement letter and report should state clearly which service was performed (American Institute of CPAs).

What donors should expect to see in the audit package

A serious audit package commonly includes the auditor’s opinion letter, full financial statements, and notes that explain accounting policies, restricted net assets, related-party transactions, and major concentrations of revenue. If the auditor issues a modified opinion or flags significant deficiencies or material weaknesses in internal controls, the board’s response matters as much as the finding itself. A mature board documents corrective actions and timelines, and it can explain them without defensiveness.

Specialized audits and attestations that fit adoption work

Beyond the baseline financial statement audit, certain adoption-related activities call for specialized engagements. Not every ministry needs each of these every year, and Christians genuinely disagree about how far to go when budgets are constrained. Yet donors should recognize that some risks are not optional; they are intrinsic to the work.

Single audit for ministries spending significant federal funds

If a ministry expends a threshold amount of federal awards in a fiscal year, U.S. law generally requires a Single Audit under the Uniform Guidance. This is not merely a financial statement audit with extra paperwork; it includes compliance testing tied to federal program requirements. Ministries that receive federal funding for child welfare, refugee-related services, or other programs should be prepared to disclose whether a Single Audit was required and completed (Electronic Code of Federal Regulations).

Agreed-upon procedures for restricted and pass-through funds

Some adoption ministries manage designated funds for specific families, grants for home studies, or donor-restricted funds for post-adoption care. When those balances are material or when donor concern is high, an agreed-upon procedures engagement can provide targeted testing: confirming that restricted funds were spent as restricted, that disbursements were supported, and that reconciliations occurred. This can be especially valuable where families are emotionally invested and where misunderstandings about “where the money went” can fracture trust.

Cybersecurity and privacy assurance for sensitive family data

Adoption ministries often hold deeply sensitive information: background checks, counseling records, immigration documents, and case notes. Financial audits are not designed to test cybersecurity. A ministry may need a separate security assessment or a SOC-type report, depending on its systems and risk profile. Donors should not assume that an audited ministry is automatically secure. The question is whether leadership has taken proportionate steps to safeguard data that, if exposed, could harm children and families.

Internal control audits and governance practices donors should ask about

Audit reports can be clean while internal controls are still immature. Donors should therefore ask how the ministry structures authority, approvals, and oversight. Adoption work requires ethical clarity about decision-making, especially when money, influence, and pastoral authority intersect.

Key control areas that deserve explicit documentation

We recommend that donors look for evidence that the ministry has formal policies and board oversight in several areas. The specifics will vary by size, but the underlying principle is consistent: no single trusted leader should be able to initiate, approve, and reconcile the same transactions without oversight.

- Segregation of duties for cash handling, disbursements, and bank reconciliations

- Documented gift acceptance and restricted gift compliance procedures

- Related-party transaction policy and annual disclosures

- Whistleblower and fraud reporting mechanism with board visibility

- Expense reimbursement policy with clear approval thresholds

Board-level finance oversight is part of Christian witness

Donors should not equate a charismatic founder with a mature governance structure. A board finance committee that meets regularly, reviews financials, and engages the auditor without management present is a protective measure for the ministry and for the families it serves. This aligns with a biblical pattern: leadership that welcomes scrutiny because it fears God more than embarrassment, and because it understands how quickly good intentions can be compromised.

For donors who want a broader view of accountability expectations in this space, our coverage of Accountability and Transparency in Christian Adoption Ministries names the kinds of evidence that tend to separate admirable intentions from dependable practice.

How to read an audit as a donor without becoming an accountant

Many donors feel a tension here. On the one hand, it seems inappropriate to interrogate a ministry doing holy work. On the other hand, donors know that adoption stories can become a form of fundraising pressure, and that pressure can dull discernment. A disciplined approach to audits allows donors to honor both compassion and prudence.

Start with the auditor’s opinion and the notes

A clean, unmodified opinion is a baseline expectation for mature organizations, though it does not prove operational excellence. Donors should then read the notes for restrictions, liquidity disclosures, related-party transactions, and major concentrations. Heavy dependence on a small number of donors is not inherently wrong, but it increases fragility. Significant related-party activity is not automatically disqualifying, but it demands strong safeguards and transparency.

Pay attention to liquidity and going concern signals

Adoption ministries can experience volatile revenue, especially when public controversies or country program changes occur. Donors should therefore look for liquidity disclosures and any “going concern” language. An organization under severe cash pressure may be tempted to blur restricted funds, delay vendor payments, or underinvest in safeguarding and compliance. None of those outcomes serves children well.

Compare the audit to program claims and fundraising messaging

Audits do not verify program outcomes, but they do show whether spending patterns match the story being told. If a ministry speaks primarily about direct family support yet shows a structure dominated by overhead categories, donors can ask for clearer explanations rather than defaulting to suspicion. The field has been shaped by the “Overhead Myth” statement, in which nonprofit evaluators and philanthropic leaders cautioned donors against simplistic ratios as a measure of effectiveness (Candid GuideStar). The better question is whether spending is aligned to mission, governed well, and evidenced honestly.

Across our verification work at Most Trusted, we find that donors gain clarity when they treat audits as one piece of a larger integrity picture: governance, policies, transparency, and evidence of outcomes. That is why The Most Trusted Standard evaluates ministries across multiple criteria rather than collapsing trust into a single document.

When an audit is necessary but not sufficient for donor confidence

Adoption ministry is not only financial. It is relational, pastoral, and legal. An audit can confirm the faithful presentation of financial statements, but it cannot by itself confirm ethical recruitment practices, trauma-informed care, appropriate safeguarding, or the quality of post-adoption support. Donors should resist the comfort of a single checkbox.

Field controversies require more than financial assurance

The modern orphan care movement has had to reckon with the risk of incentivizing child separation. Best practice increasingly emphasizes family preservation where possible, careful gatekeeping, and partnership with credible local entities. Financial integrity supports that work by reducing pressures that can distort decisions. Yet the core discernment question remains: does the ministry’s model reflect the moral contours of the work, including the dignity of birth families and the long-term needs of children?

Verification should integrate faithfulness, governance, and transparency

Donors often ask what they can reasonably require without burdening a ministry. Our answer is that donors can require clarity proportional to the stakes. If a ministry asks the church to fund life-altering interventions, it should be prepared to show governance competence, audited financials appropriate to its funding sources, and public transparency that does not collapse under scrutiny. This is not distrust. It is a mature form of love for neighbor, protecting children and protecting ministries from avoidable failure.

For readers assessing multiple organizations, Christian Adoption Ministries provides a broader landscape of how donors can think about the category and its integrity signals.

FAQs for What financial audits Christian adoption ministries should complete

Should a small Christian adoption ministry have a full audit every year?

Not always, but a ministry should have a plan that matches its risk. If the organization is small, a CPA review may be an interim step, but donors should understand that a review is not an audit and provides limited assurance. As revenue, complexity, and restricted funding grow, an annual independent financial statement audit becomes a normal expectation, and the board should be able to explain why its chosen level of assurance is responsible.

What is the single biggest audit red flag donors should watch for?

Persistent control problems that leadership treats as normal. A single finding can occur in otherwise healthy organizations, especially during growth. The concern is a pattern: repeated internal control deficiencies, unclear handling of restricted funds, or resistance to transparency. The financial risk is real, but the deeper issue is governance culture: whether the ministry is willing to be corrected for the sake of children, families, and the church’s credibility.

Stewardship that can be examined

Christian donors do not fund adoption ministry merely to feel compassion; we give because the gospel compels tangible mercy, and because children and families deserve trustworthy care. Financial audits are one concrete way a ministry demonstrates that it welcomes examination, honors restrictions, and treats money as a sacred trust. In a field where the moral stakes are unusually high, the most credible ministries are those that pair pastoral concern with verifiable integrity.