Evaluating transparency reports from biblical museum ministries is a stewardship question before it is a communications question. Donors are not merely funding exhibits and educational programming; they are entrusting resources to institutions that claim to handle Scripture, history, and public witness with integrity.

Museums that interpret the Bible operate under uncommon pressures. They sit at the intersection of scholarship, apologetics, tourism, philanthropy, and media scrutiny. The best transparency reporting does not pretend those tensions do not exist. It shows a ministry willing to tell the truth about its governance, finances, claims, and outcomes, even when clarity costs something.

Begin with the purpose of transparency in Christian stewardship

Transparency is not public relations

A transparency report is not fundamentally a donor-facing brochure. In Christian moral reasoning, truth-telling belongs to our discipleship, not merely our brand management. Scripture is unambiguous that God “delights in truth in the inward being” (Psalm 51:6), and the New Testament’s commands against “falsehood” and “deceit” are not suspended for fundraising (Ephesians 4:25). A mature report is shaped by that moral center: it aims to make reality legible for those who support the work.

For biblical museum ministries, the reality donors need is often more complicated than simple “attendance grew” or “impact increased.” The work involves collections, provenance, conservation, interpretive decisions, and academic engagement. When a report reduces complexity into slogans, donors should treat that as a signal. Clarity is good; oversimplification is not the same thing.

Donors have a legitimate claim to verifiable information

Christian donors carry a dual responsibility: generosity and prudence. Jesus’ parables assume careful stewardship even as they commend sacrificial giving (Matthew 25:14–30). What this means in practice is that donors are right to ask whether a museum ministry’s reporting makes it possible to evaluate claims and to identify risk.

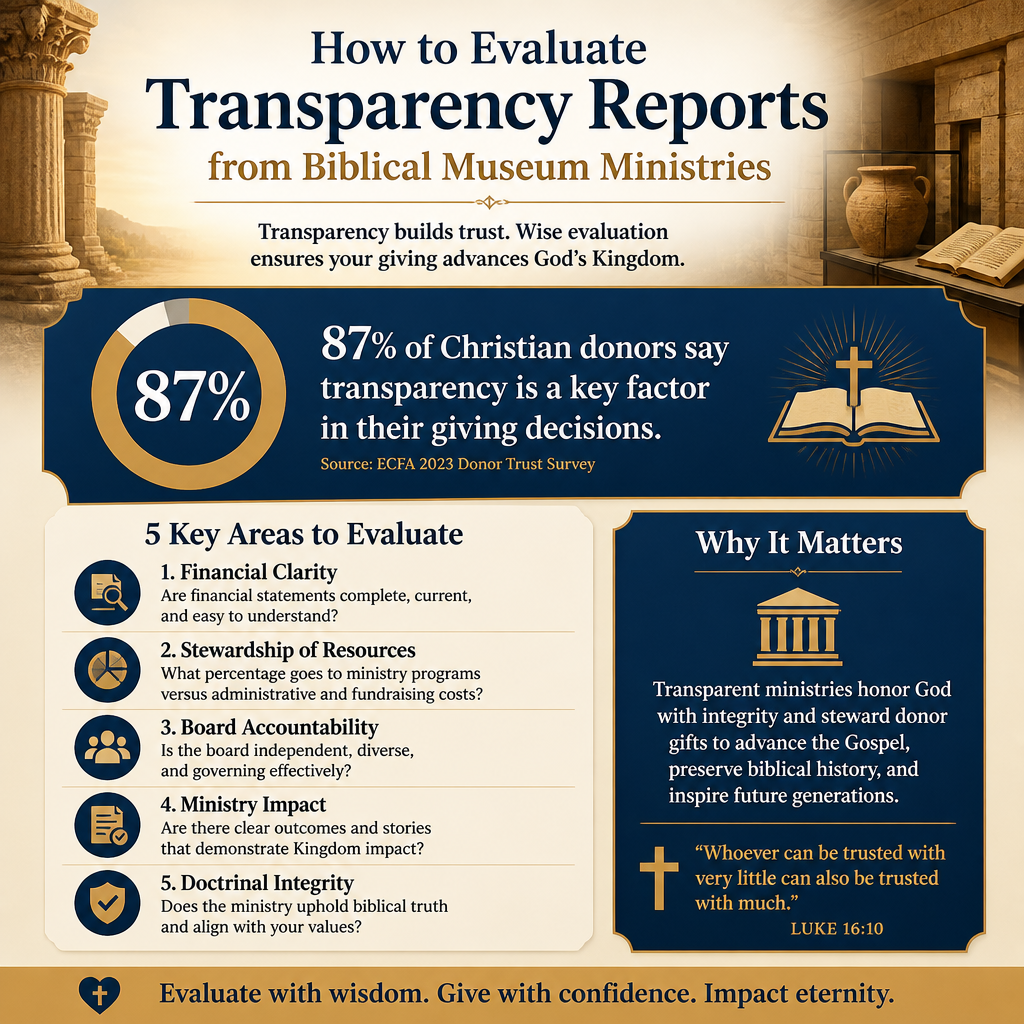

Across our verification work at Most Trusted, the organizations that meet The Most Trusted Standard tend to treat transparency as a discipline of accountability: documents are consistent year to year, numbers reconcile across sources, and leadership communicates with a steady seriousness rather than reactive defensiveness. That posture matters as much as any single metric.

Test whether the report is complete, consistent, and comparable

Completeness includes what is uncomfortable

Many reports describe mission, highlights, and gratitude, then move quickly away from the particulars. Donors should look for whether the report addresses the categories where mistakes are most costly: governance, financial statements, related-party transactions, collections ethics, and measurable outcomes.

A useful first test is whether the transparency report points you to primary documents rather than asking for trust. For U.S. nonprofits, that normally includes the Form 990, audited financials (when applicable), and a clear articulation of governance structures. The Internal Revenue Service makes Form 990 expectations and access central to nonprofit accountability (IRS Charities and Nonprofits).

Consistency across documents is a basic integrity check

Donors should compare the transparency report to other public records. Do revenue totals, program descriptions, and key leaders align with what appears in audited statements, Form 990, and the organization’s website? Minor differences can be normal, but repeated discrepancies suggest weak internal controls or an overly curated narrative.

Comparability over time is also important. A museum ministry may cite a strong year of attendance or donations, but donors need to understand whether that result is typical, cyclical, or driven by a one-time event. Reports that provide multi-year summaries, even in simple tables, are more trustworthy than reports that offer only a single-year snapshot.

Evaluate financial transparency without falling for simplistic ratios

Financial clarity includes how funds are raised, restricted, and spent

Financial transparency is not exhausted by “overhead” percentages. Wise donors already know the problems with simplistic administrative ratios, and the sector has publicly acknowledged that these measures can mislead. The “Overhead Myth” letter signed by GuideStar (now Candid), Charity Navigator, and BBB Wise Giving Alliance argued that overhead ratios are a poor measure of nonprofit performance and can create harmful incentives (Candid).

For biblical museum ministries, donors should look instead for clear explanations of:

- Major revenue streams, including admissions, memberships, gifts, grants, and retail operations

- How restricted gifts are tracked and honored

- Fundraising costs described with enough detail to interpret them responsibly

- Debt obligations and how debt service affects mission spending

- Capital projects and the long-term costs they create

Debt deserves particular attention in museum contexts, where construction and expansion can outpace realistic earned revenue. Transparency requires not only listing liabilities, but explaining the strategy for meeting them without undermining mission integrity.

Audits, controls, and board oversight should be visible

When a ministry is large enough to warrant audited statements, donors should expect them to be readily accessible and current. The report should describe basic internal controls in plain language: who approves expenditures, how conflicts are handled, and how the board exercises fiduciary responsibility.

When donors want to understand what “good governance” looks like, the parent category Accountability and Transparency in Biblical Museum Ministries provides the broader accountability context in which transparency reports should be read. A report cannot substitute for governance, but it can reveal whether governance is functioning.

Look for governance transparency and conflicts of interest

Board composition, independence, and real accountability

Museum ministries often include founders, prominent public figures, and donors with deep personal commitment. That can be a strength, but it also raises predictable risks: concentration of power, blurred lines between board and management, and difficulty correcting course when the institution’s public identity is tied to a single leader.

A credible transparency report names board members, identifies officers, and clarifies whether the board includes independent members with relevant expertise (finance, legal, museum ethics, education). It also describes how often the board meets and how it oversees executive leadership. Donors should be cautious when governance information is hidden or when accountability is described only in vague spiritual terms rather than operational reality.

Related-party transactions and donor influence should be addressed directly

Large gifts, naming opportunities, and vendor relationships are normal in the museum world. What matters is whether the ministry has clear conflict-of-interest policies and discloses material related-party transactions. Donors should expect to see a policy statement at minimum, and ideally a summary of how conflicts are identified and managed.

The purpose is not suspicion for its own sake. It is protection: for the ministry, for donors, and for the credibility of Christian witness. When a museum ministry handles the Bible publicly, the costs of avoidable scandal are borne far beyond the institution itself.

Assess claims, scholarship, and effectiveness with an evidence mindset

Transparency includes epistemic humility and clear boundaries

Biblical museum ministries make claims—about history, archaeology, textual transmission, and cultural impact—that can shape faith and public discourse. Christians genuinely disagree about contested questions in biblical studies and archaeology, and donors should not confuse controversy with misconduct. The more relevant question is whether the institution clearly distinguishes between established evidence, plausible interpretation, and advocacy.

A mature transparency report does not need to litigate academic debates. It should, however, show that the museum has standards: curatorial review, peer consultation, clear citation practices, and a willingness to correct errors. If an institution presents disputed assertions as settled fact without acknowledgment, donors should ask what internal processes govern interpretive integrity.

Effectiveness means more than attendance

Many museums report visitor counts, school groups served, or media reach. Those can be legitimate indicators of scale, but they are not the same as effectiveness. Donors should look for a theory of impact: what the museum believes it is accomplishing (biblical literacy, evangelistic engagement, public apologetics, family discipleship) and how it evaluates whether that is happening.

Where measurement becomes complex—spiritual formation is not easily reduced to survey instruments—transparency is still possible. It may include qualitative research, third-party evaluation of educational programs, or clearly bounded outcome claims. Strong reports resist the temptation to promise spiritual outcomes that cannot be responsibly verified.

For donors seeking the broader landscape of what constitutes healthy practice in this field, Biblical Museum Ministries offers a wider frame for evaluating ministry models, governance realities, and public trust risks that affect museum organizations in particular.

FAQs for How to evaluate transparency reports from biblical museum ministries

Should a biblical museum ministry publish audited financial statements?

When an organization is of sufficient size or complexity, audited financial statements are a strong indicator of financial seriousness, and many donors should reasonably expect them. Smaller ministries may not have an audit due to cost, but transparency should still include accessible Form 990s, clear financial summaries, and governance disclosures that make oversight credible. The key question is whether the reporting matches the organization’s scale, risk profile, and public claims.

What if a transparency report is inspiring but light on documentation?

Inspiration is not a defect, but it is not accountability. Donors should treat a documentation-light report as incomplete and request primary materials: Form 990, board list, conflict-of-interest policy, and financial statements. A ministry’s willingness to provide these promptly and without defensiveness often reveals more than the prose of the report itself.

Donor confidence requires truth that can bear weight

Transparency reports from biblical museum ministries should help donors see the ministry as it is: its governance, its finances, its interpretive standards, and its outcomes. The goal is not cynicism; it is faithful stewardship shaped by truth. When reporting is clear, consistent, and verifiable, donors can give with the quiet confidence that their generosity is strengthening a work built to endure scrutiny as well as enthusiasm.