Knowing how to evaluate financial transparency in Bible distribution ministries is not a peripheral concern for Christian donors. When a ministry asks the church to fund Scripture for the nations, it is asking for more than money; it is asking for trust in its stewardship before God and his people.

Scripture treats stewardship as a spiritual matter with public consequences. Paul assumed that integrity with funds should be demonstrable, not merely asserted: “We want to avoid any criticism of the way we administer this liberal gift. For we are taking pains to do what is right, not only in the eyes of the Lord but also in the eyes of man” (2 Corinthians 8:20–21). Financial transparency is one practical way a ministry “takes pains” to do what is right.

Begin with verifiable documents, not reassuring narratives

Most Bible distribution ministries can tell compelling stories. The more disciplined question is whether their financial reporting allows an informed outsider to confirm how resources move from donor to translated, printed, and delivered Scripture.

At Most Trusted, we evaluate ministries against The Most Trusted Standard, a 15-criteria framework that includes financial integrity and disclosure expectations. We do not assume malice when information is missing, but we do assume that donors need more than marketing claims when they are funding work that often operates across currencies, borders, and complex supply chains.

Start with the IRS Form 990 or audited financial statements

For U.S.-based ministries, the Form 990 is often the most comparable, standardized window into operations. Many donors are unaware that tax-exempt organizations are generally required to make their annual returns available for public inspection, including by providing copies upon request or making them widely accessible online; the IRS explains these public disclosure rules in its guidance for charities and nonprofits at IRS Charities and Non-Profits.

An audited financial statement can add confidence when it is truly independent, timely, and paired with meaningful notes. However, not every audit is equal. Donors should distinguish between a full audit, a review, and a compilation. The audit opinion, the auditing firm’s reputation, and the presence of material weaknesses or going-concern language all matter.

Seek clarity about what “Bible distribution” includes

Bible distribution is not a single activity. It can include translation, licensing, printing, shipping, warehousing, last-mile distribution, digital delivery, Scripture engagement programming, and training for local church partners. Transparency begins when a ministry defines its categories consistently and reports in a way that allows a donor to see what the ministry means by “distribution.”

Trace revenue integrity and the risk points common to this field

The field has had to reckon with recurring temptations: overstated reach, ambiguous restricted giving, and the quiet transfer of ministry funds into related-party ecosystems. These risks are not unique to Bible distribution, but the global nature of the work can conceal them.

Restricted giving should be treated as a sacred obligation

If a donor gives to print Bibles in a specific language, the ministry should be able to show that the funds were used for that purpose, or that the donor was informed and consented to any necessary reallocation. Accounting standards in the United States require nonprofits to disclose net assets with donor restrictions and to report releases from restrictions in a disciplined way; the Financial Accounting Standards Board provides the framework that governs these nonprofit financial statements at FASB.

What this means in practice is that a ministry’s transparency is often visible in its footnotes and its internal controls, not in its fundraising appeals. Ministries that handle restrictions well tend to have clean policies, board oversight, and consistent public reporting that does not shift definitions when convenient.

Related-party transactions deserve daylight

Donors should pay attention when a ministry purchases printing, logistics, consulting, software, or fundraising services from entities owned by insiders, board members, or close associates. Related-party transactions are not automatically improper, but they create conflicts of interest that must be governed and disclosed. A credible ministry will name related parties, describe the nature of the relationship, and explain how pricing was determined as fair.

In Bible distribution, related-party risks can also show up in overseas partner relationships, especially where the ministry funds a local entity that is not independently governed. Transparency is stronger when a ministry can explain how it verifies partner spending and how it prevents cash from becoming untraceable once it crosses borders.

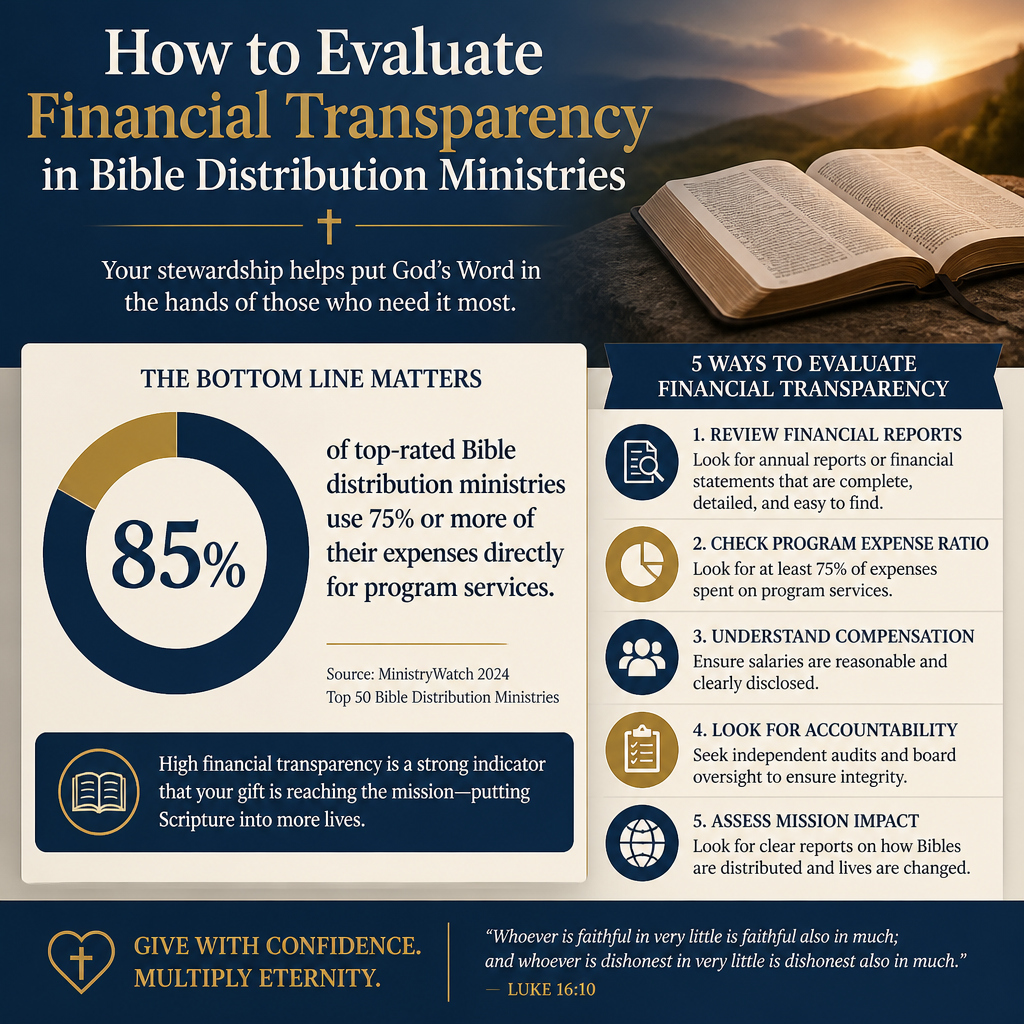

Read expense categories with discernment rather than superstition

Christian donors sometimes default to a simplistic test: “low overhead equals faithful stewardship.” The sector itself has pushed back on that assumption. The joint “overhead letter” signed by GuideStar, Charity Navigator, and BBB Wise Giving Alliance argued that overhead ratios can mislead donors and can punish necessary investments in governance, staff competence, and evaluation; see GuideStar’s summary at GuideStar.

That said, the opposite error is also common: treating efficiency metrics as irrelevant. Mature stewardship does not worship overhead ratios, but it also does not refuse accountability for costs that drift upward without justification.

What healthy spending often looks like in Bible distribution

Many Bible distribution models include meaningful costs outside “program” lines: quality control, safeguarding for field partners, compliance for restricted regions, and systems that prevent fraud. Donors should not penalize a ministry for investing in what keeps the work honest and sustainable.

We recommend asking whether the ministry’s categories are stable and intelligible year over year. If “program services” includes a large share of fundraising communications or executive travel without clear program linkage, the ratio may be high while transparency is low.

A short set of questions that usually clarifies reality

- How does the ministry define “Bible distributed” across print, audio, and digital formats?

- What portion of spending is grants to partners, and what oversight accompanies those grants?

- Do fundraising costs rise proportionally with revenue, or do they accelerate as returns diminish?

- Are executive compensation and benefits clearly reported and board-approved?

- Do the audited statements or 990 show related-party transactions, loans, or unusual vendor concentration?

Demand outcome honesty, not only output volume

Bible distribution ministries often report outputs: Bibles printed, shipped, downloaded, or placed. Outputs matter, but outputs are not the same as outcomes. The church’s concern is not merely that paper moved; it is that Scripture is received, understood, and embedded in the life of local churches in ways that endure.

Christians genuinely disagree about how much a Bible distribution ministry should be responsible for downstream discipleship. Some ministries exist to serve local churches and assume the church will do the formation work. Others integrate Scripture engagement and training. The transparency question is not which model is “more spiritual,” but whether the ministry describes its claims with precision and reports what it can actually verify.

Define “reach” in ways that can be tested

When a ministry reports “people reached,” donors should ask what “reach” means. Is it estimated readership per Bible? Is it household size assumptions? Is it app installs, unique active users, or downloads that may never be opened? Responsible transparency will name the methodology and its limits.

Digital distribution adds both promise and ambiguity. App analytics can be real evidence, but they can also be inflated by marketing-driven installs. Ministries should distinguish downloads from ongoing engagement and avoid presenting projections as observed outcomes.

Evidence of integrity often appears in what is not claimed

Across our verification work, ministries that meet The Most Trusted Standard tend to resist exaggeration. Their reports include constraints: customs delays, partner disruptions, security restrictions, and projects that did not go as planned. This kind of sober reporting is not weakness; it is a hallmark of leadership that does not require constant triumph to sustain donor confidence.

Use governance transparency as a proxy for financial trustworthiness

Financial transparency rarely survives in the absence of governance transparency. A ministry may publish impressive numbers, but if the board is insular, conflicted, or uninformed, donors should expect blind spots.

We encourage donors to view financial disclosure alongside governance disclosure: board composition, independence, conflict-of-interest policy, whistleblower policy, and whether the board reviews audited statements and the Form 990 before filing. For donors seeking broader context on this theme within the field, see Accountability and Transparency in Bible Distribution Ministries.

Board independence and conflicts are not technicalities

Some ministries are founder-led and entrepreneurial. That can be a gift to the church. It can also create environments where financial decisions go unchallenged, especially when family members are employed, when vendors are connected to insiders, or when the founder controls the board. Donors should not assume impropriety, but they should insist on guardrails that make impropriety difficult.

Transparency should be accessible, not buried

Faithful ministries do not make donors hunt for basic facts. A credible “transparency” page typically includes recent audited statements or 990s, a clear articulation of mission and activities, a list of board members, and a reasonable summary of outcomes. When a ministry with substantial revenue provides only curated testimonials and a few infographics, it is asking donors to trust what it will not document.

For donors comparing models and ministry types across the wider landscape, see Bible Distribution Ministries.

FAQs for How to evaluate financial transparency in Bible distribution ministries

Is an audited financial statement enough to establish transparency?

An audit is a meaningful signal, but it is not the whole story. Donors should still read the notes, look for related-party disclosures, consider whether the audit is current, and examine how the ministry reports outcomes. Transparency is stronger when audited statements align with clear public reporting about what the ministry does and how it measures its work.

Should donors avoid ministries with higher administrative or fundraising costs?

Not automatically. Higher administrative costs can reflect necessary investment in controls, compliance, technology, and oversight for global work. The question is whether the costs are explained, governed, and consistent with the ministry’s model, and whether the ministry avoids manipulating categories to appear unusually efficient.

Stewardship requires evidence that can bear weight

Christian donors are not obligated to fund every sincere appeal, but we are obligated to give as stewards who will answer to God. Financial transparency in Bible distribution ministries is one way donors honor that obligation: by supporting organizations willing to be examined, willing to be corrected, and willing to “take pains” to do what is right in the eyes of the Lord and in the eyes of his people.