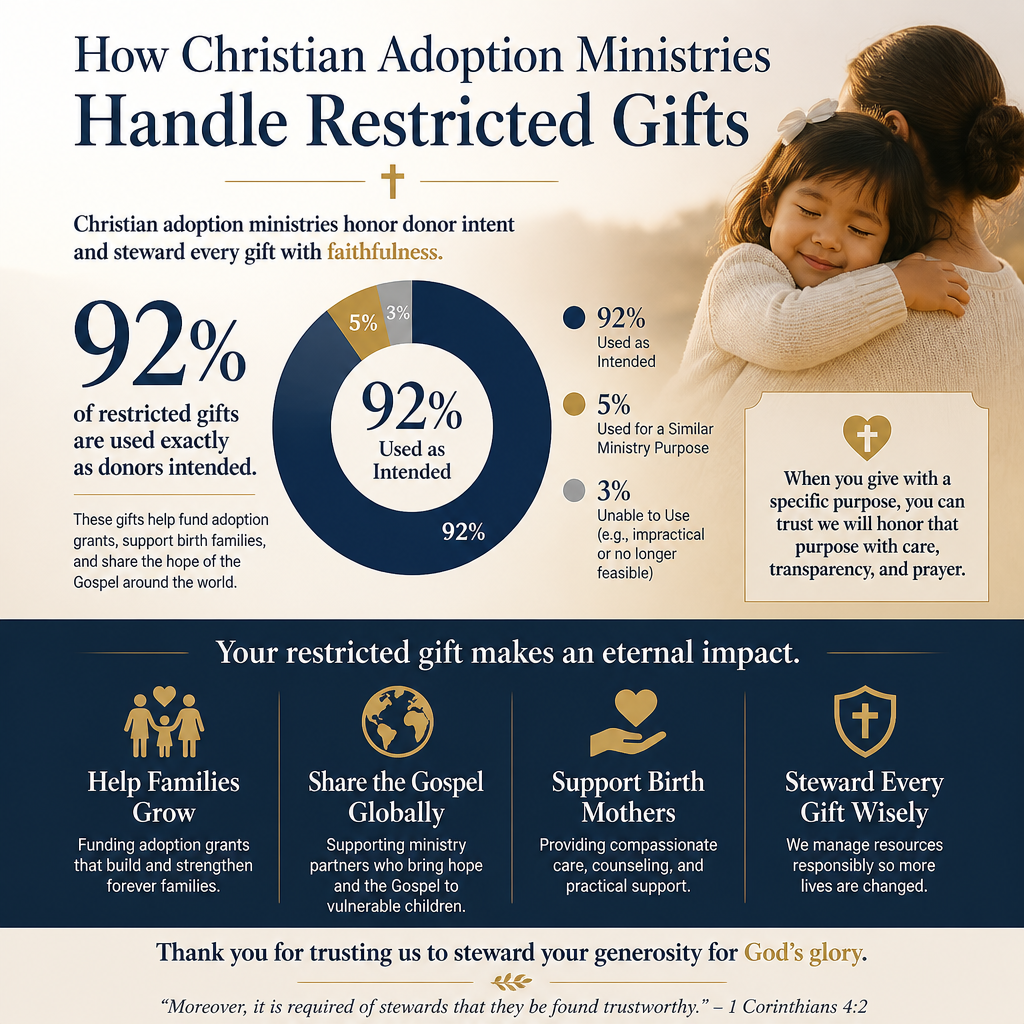

How Christian adoption ministries handle restricted gifts is not a technical footnote to Christian generosity; it is one of the clearest places where integrity becomes measurable. Donors often give with a specific child, family, or program in view, and Scripture treats such commitments as morally serious. “It is required of stewards that they be found faithful” (1 Corinthians 4:2) is not merely a devotional sentiment; it is a governance standard.

Restricted giving also sits inside real complexity. International adoption policies shift. A birth family may choose reunification. An adoptive placement can disrupt for reasons no one can control. A ministry can do everything right and still face a genuine impossibility: the donor’s intent cannot be fulfilled exactly as written. The question is not whether constraints arise, but whether a ministry has the maturity to honor donor intent without distorting the mission, the financial statements, or the truth.

Restricted gifts are a promise, not a preference

Donor intent has spiritual weight

In Christian adoption work, restricted gifts frequently carry pastoral urgency. A donor may give because a specific waiting child’s story has pierced the heart, because a church is rallying around a particular adoptive family, or because a ministry has named a concrete barrier like home study costs or post-adoption counseling. That desire to give “toward something” is not immaturity; it can be a disciplined form of stewardship.

Scripture’s emphasis on honesty in speech and commerce applies directly. “An abomination to the Lord are dishonest scales” (Proverbs 11:1) is a warning against the quiet redefinition of a promise. When a ministry markets a fund as designated for a specific purpose and then treats it as general support when pressure rises, the ministry is not merely making an accounting choice. It is trading away trust.

How restrictions differ from designations

Not every note in a memo line creates a binding restriction. Mature ministries distinguish clearly between (a) donor-imposed restrictions that the organization agrees to honor and (b) donor preferences that guide internal budgeting but do not bind the organization legally or ethically in the same way. The distinction matters because it affects how the gift is recorded, how it is reported, and what happens if the original purpose becomes impracticable.

In most cases, nonprofit accounting in the United States treats donor restrictions as conditions on use, not on organizational control. The organization still owns the funds, but it holds them under obligation to apply them to the specified purpose. That obligation must show up in both internal controls and external reporting.

What strong ministries put in place before they accept restricted gifts

Gift acceptance policies that are actually used

Across our verification work at Most Trusted, the ministries that meet The Most Trusted Standard tend to treat restrictions as a governance question before they become a financial crisis. The most basic safeguard is a written gift acceptance policy approved by the board, paired with trained staff who apply it consistently. Without that, restrictions are accepted ad hoc, often by frontline fundraisers under pressure to say yes.

Healthy policies answer hard questions in advance: What types of restrictions will the ministry accept? What happens if the ministry cannot fulfill a restriction? Who has authority to approve an exception? How will the ministry communicate limitations before a donor gives?

Separate tracking, approvals, and audit-ready documentation

Integrity requires systems, not intentions. A ministry handling restricted gifts well will be able to demonstrate, with documentation, that restricted funds are tracked separately from unrestricted funds, that expenditures are coded to the proper program or fund, and that any transfers or releases are reviewed and approved.

In practice, we look for a short chain of evidence: the donor communication that created the restriction, the accounting entry that recorded it, the internal reports that monitored it, and the expense documentation that shows compliance. Ministries that cannot produce this chain may still be doing good work, but donors should recognize that the organization is asking them to trust what it cannot verify.

- Written restriction language captured at the time of the gift

- Fund accounting or class tracking in the general ledger

- Monthly or quarterly restricted fund reporting to leadership

- Clear approval thresholds for restricted spending and transfers

- Consistent donor receipts that do not overpromise

When a restriction becomes impossible, what faithfulness looks like

Common scenarios in adoption ministry

Adoption ministry is particularly exposed to “impossibility” scenarios because it is built around individual cases, legal timelines, and cross-border policy decisions. A fund restricted to “the Johnson family’s adoption” may become unspendable if the placement changes. A fund restricted to a certain country program may become unusable when the country pauses intercountry adoption. A fund restricted to “adoption fees” may not fit the actual need if the primary burden becomes post-adoption clinical care.

The presence of these scenarios does not justify vague restriction language or casual reassignment. It does, however, explain why prudent ministries state contingencies up front, in plain language, so that donors are not surprised when a case changes.

Ethical options ministries should use in order

When a donor’s original intent cannot be met, faithful handling is ordered and documented. First, the ministry should seek the donor’s written consent to redirect the funds to a closely aligned purpose. Second, if the donor cannot be reached, the ministry should follow its policy and applicable state law to determine whether a variance is permitted, often with board oversight and, in some cases, legal counsel.

In the United States, the legal framework for restricted gifts is often governed by state law influenced by the Uniform Prudent Management of Institutional Funds Act, which provides standards for managing charitable funds and, under certain conditions, modifying restrictions. Donors who want a useful overview of the framework can start with the Uniform Law Commission’s UPMIFA materials at Uniform Law Commission.

What this means in practice is that the ministry should be able to explain, without defensiveness, why a restriction could not be met, what steps were taken to contact the donor, what authority approved the change, and how the revised use remains faithful to the donor’s original charitable purpose.

Transparency signals donors can verify

Financial statements that reflect restricted reality

Donors should not be forced to infer restricted gift stewardship from marketing language. Strong organizations make restrictions visible in their financial reporting. Under U.S. GAAP, nonprofits report net assets with donor restrictions separately from net assets without donor restrictions, and they disclose the nature of those restrictions in the notes when material. The Financial Accounting Standards Board provides the standard for nonprofit net asset classification (ASU 2016-14) at Financial Accounting Standards Board.

Ministries that habitually carry large restricted balances without clear explanation can be signaling either (a) healthy multi-year commitments or (b) restricted funds they cannot responsibly deploy. Donors should press for clarity, because both realities can produce the same outward number.

Public communication that resists emotional fundraising shortcuts

Adoption appeals can become highly individualized and emotionally potent. The ethical temptation is to present every need as immediate and every restricted gift as certain to accomplish an outcome. Mature ministries speak more carefully. They communicate the difference between supporting an effort and guaranteeing an adoption, and they avoid language that implies a donor is “buying” a result.

Donors looking for deeper context on how we evaluate adoption work beyond marketing claims can review the broader landscape of Christian Adoption Ministries. The point is not suspicion. It is stewardship: serious love should not require naïveté.

How we evaluate restricted gift practices under The Most Trusted Standard

What we ask, and why it matters

Most Trusted exists to help Christian donors give with confidence by evaluating ministries against The Most Trusted Standard, a 15-criteria framework spanning faith commitments, financial integrity, governance, and transparent reporting. Restricted gifts touch several criteria at once because they reveal whether a ministry’s internal life matches its public claims.

We do not treat restricted gift handling as a mere compliance checklist. We look for evidence of stewardship culture: boards that understand their fiduciary responsibility, executives who refuse to solve cash flow pressure by borrowing from restricted funds, and finance teams empowered to say no when a restriction cannot be tracked faithfully.

Questions donors should ask before making a restricted gift

Donors do not need to become accountants, but a few direct questions can clarify whether a ministry is prepared to honor a restriction without confusion.

Consider asking:

- Do you have a written policy for restricted gifts and contingencies if plans change?

- How do you track restricted funds in your accounting system, and who reviews the reports?

- Will my receipt and your follow-up reporting clearly state how the funds were used?

- If the original purpose becomes impossible, what is your process for seeking donor consent or returning the gift?

For donors who want a broader accountability lens—beyond restricted gifts alone—the category of Accountability and Transparency in Christian Adoption Ministries provides the adjacent questions that often surface together: reporting, governance, outcome claims, and the integrity of appeals.

FAQs for How Christian adoption ministries handle restricted gifts

Can an adoption ministry move restricted funds to general operations if cash flow is tight?

A ministry should not treat donor-restricted funds as a cash reserve for general operations, even if the intention is to “pay it back.” Ethically, this violates donor intent; operationally, it can create compounding risk if the restricted purpose comes due and the funds are no longer available. If a ministry experiences recurring cash pressure, the responsible remedy is budgeting and fundraising reform, not internal borrowing from restricted accounts.

What should happen if a donor gives to a specific adoption case and that placement falls through?

Best practice is to disclose contingencies before the gift is accepted and to seek the donor’s written direction if the case changes. If the donor cannot be reached, the ministry should follow its documented policy and applicable law to redirect the funds to the closest aligned purpose, with board-level oversight and clear records. Where appropriate and feasible, returning the gift can be the most straightforward way to honor the donor’s intent and preserve trust.

Faithful restricted-gift stewardship protects children, families, and trust

Restricted gifts in adoption ministry are rarely about abstract programs; they are often about concrete families and vulnerable children. That is precisely why restrictions require disciplined care. When ministries honor donor intent with clarity, documentation, and truthful communication, they strengthen the credibility of Christian witness in a field that already carries high emotion and high stakes.

Donors should not be asked to choose between compassion and rigor. The church’s calling to care for the fatherless is not served by sentimental giving untethered from accountability. It is served when generosity is matched by verifiable faithfulness.