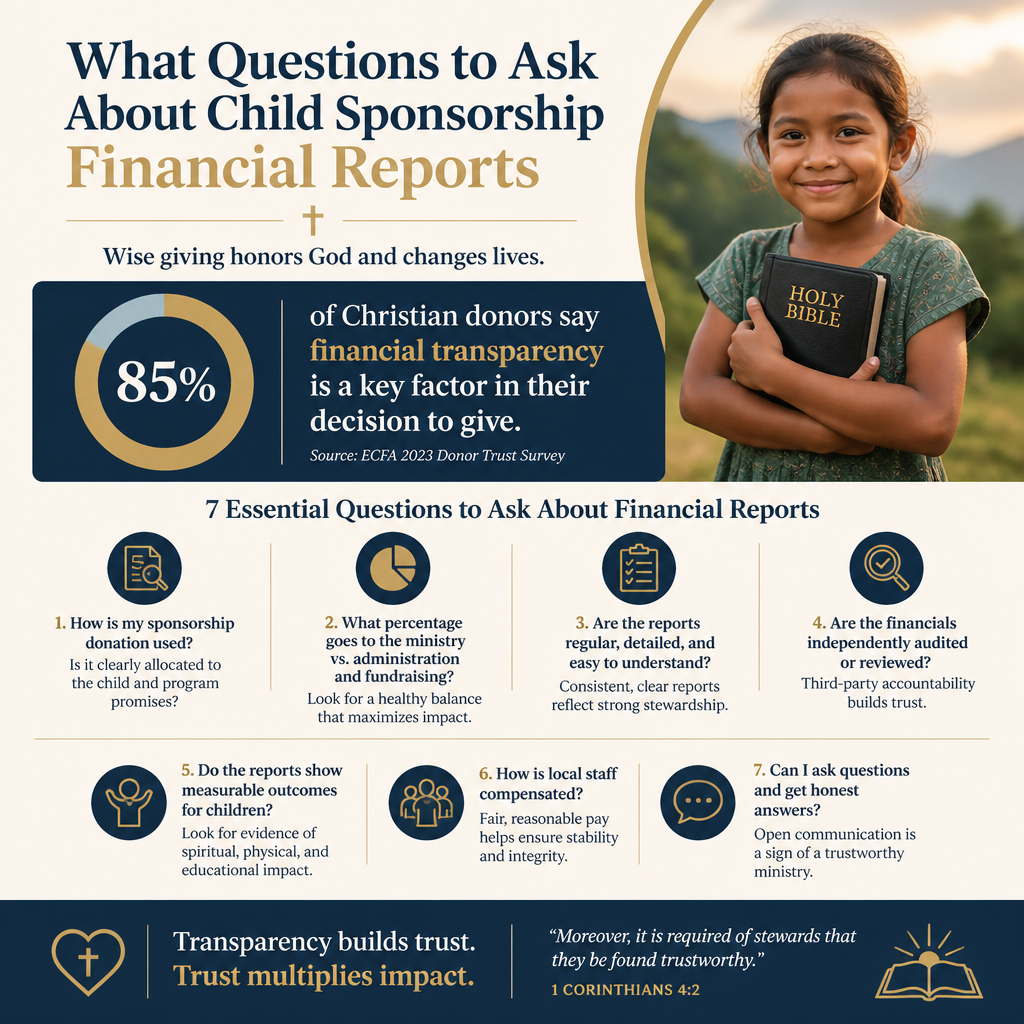

Asking the right questions to ask about child sponsorship financial reports is not a bureaucratic exercise. It is a stewardship practice shaped by Jesus’ repeated insistence that money reveals what we truly love, and by Scripture’s refusal to separate compassion from honesty. Mature Christian donors want more than assurances that “most of your gift goes to the child.” We want financial reporting that can bear the weight of truth.

Child sponsorship sits at the intersection of deep Christian instincts—personal care for a child, long-term commitment, and tangible mercy—and a complex operating reality that includes cross-border transfers, restricted donations, field partner relationships, and program models that vary widely. Some ministry leaders fear donors will misunderstand overhead and compliance. Some donors, shaped by simplistic watchdog metrics, reward under-investment in systems that prevent fraud and protect children. Financial reports are where those tensions become visible.

Start with the promise being made to the sponsor

The first question is not “What is their overhead?” but “What did this ministry promise the donor, and where is that promise defined?” Child sponsorship can mean direct material support to an individual child, or community-based programming where the sponsored child is the relational anchor for shared services like school support, water access, and nutrition. Both models can be faithful; what matters is whether the reporting matches the promise.

Ask where sponsorship revenue is classified and why

Ministries that meet The Most Trusted Standard tend to state clearly whether sponsorship gifts are treated as restricted (designated for a particular program purpose) or unrestricted. That classification shapes every subsequent line item. If a ministry says “your gift supports this child,” donors should see language that explains whether that means individual benefits, community benefits, or both, and how the ministry prevents marketing language from outrunning accounting reality.

Look for alignment between narrative and audited numbers

Annual reports often highlight stories and outcomes. Financial statements present categories and totals. A responsible donor asks whether the organization’s program narrative is consistent with its audited financial statements and footnotes. If the story emphasizes “education sponsorship,” but financial reporting collapses education into a broad “program services” bucket with no further explanation, a follow-up question is warranted.

Trace how sponsorship dollars move from donor to field

Child sponsorship financial reports should help a donor understand not only what the ministry spent, but how funds flow across borders and partners. International work adds layers of currency exchange, local compliance, and partner capacity, and these are not excuses for opacity. They are reasons to report more carefully.

Ask how funds are transferred and controlled

Responsible organizations can describe the mechanisms used to move funds to field offices or indigenous partners: bank transfers, vetted payment platforms, local finance staff, segregation of duties, and reconciliation practices. If an organization works primarily through local partners, donors can ask whether partner financials are reviewed, whether subrecipients are monitored, and whether there are consequences for noncompliance.

Some donors assume that any administrative layer is suspect. Yet Scripture’s concern is not the absence of administration; it is integrity. Paul’s collection for the saints was handled with visible accountability “so that no one should blame us about this generous gift” (2 Corinthians 8:20–21). A ministry that can explain controls without defensiveness is generally a healthier signal than one that offers only marketing guarantees.

Ask how exchange rates and inflation are treated

Sponsorship is often a monthly commitment, while local costs may swing dramatically. Donors should ask whether the ministry uses an average exchange rate policy, how it accounts for currency gains or losses, and how it adjusts budgets in high-inflation environments. These policies should be explained in plain language, with audited reporting as the reference point.

Interrogate program expense without falling for simplistic ratios

The field has had to reckon with an unhelpful donor habit: treating a single “percent to programs” number as a proxy for faithfulness. The Overhead Myth letter signed by GuideStar, Charity Navigator, and the BBB Wise Giving Alliance made the case that overhead ratios alone do not measure performance or integrity, and can pressure nonprofits into under-investing in systems that safeguard beneficiaries and donor funds (GuideStar).

Ask what is included in program and what is excluded

Child sponsorship ministries sometimes classify staff, monitoring, training, safeguarding, and evaluation differently. Donors can ask: Which costs are treated as program delivery, which are treated as administration, and why? A ministry can be transparent about these judgments and still be financially prudent. What deserves scrutiny is inconsistency—especially when program percentages appear unusually high because essential costs were moved elsewhere.

Use a focused set of questions rather than suspicion

Financial reports are complex, and a donor does not need to become an auditor to ask responsible questions. A short, disciplined set of prompts often reveals whether a ministry is operating with clarity and candor:

- What is the ministry’s formal definition of “sponsorship” in its donor materials and financial notes?

- Are sponsorship gifts restricted, and how are restrictions tracked and released?

- What percentage of sponsorship revenue is spent in-country, and what categories does that include?

- What portion funds shared community programs versus individualized support, and how is that decision made?

- How are safeguarding, monitoring, and evaluation funded and reported?

What this means in practice is that donors should reward ministries that can answer with specificity, even when the answers include trade-offs and operational costs. The goal is not to punish administration; it is to test whether resources are governed in the light.

Examine restricted funds, surplus balances, and sponsorship liabilities

Child sponsorship programs often generate timing differences: sponsors give monthly, projects may be seasonal, and capital needs (school fees, water infrastructure, staff training) do not align neatly with a calendar. A mature financial report helps donors distinguish between prudent reserves, restricted balances awaiting program execution, and unhealthy accumulation.

Ask how the ministry accounts for restricted net assets

In audited statements, donors should expect clarity on net assets with donor restrictions and how those restrictions are satisfied over time. The question is not whether restricted balances exist, but whether the organization can explain them and demonstrate faithful use. If restricted balances grow year after year without explanation, donors should ask whether the ministry’s ability to deliver has lagged behind its fundraising.

Ask whether child sponsorship commitments create real obligations

Some ministries describe sponsorship as a “relationship” rather than a legal commitment. Yet if a ministry markets stability to sponsors and families, donors can ask whether leadership budgets conservatively for sponsor attrition, and whether the organization maintains a contingency plan so a child is not abruptly harmed by donor churn. Financial reports may not label this as a “liability” in technical accounting terms, but prudent planning should be visible in notes, risk disclosures, and program continuity practices.

Test transparency by comparing what is published to what is answerable

Transparency is not only what a ministry posts online; it is whether leadership can answer reasonable questions without evasion. Across our verification work at Most Trusted, we observe that healthier organizations treat donor questions as part of their accountability, not as a threat to manage. They publish audited financial statements, provide clear explanations of program models, and maintain governance practices that prevent concentrated control.

Ask for the audited financial statements and the Form 990

For U.S.-based ministries, donors should ask for audited financial statements when available and review the IRS Form 990 for governance and compensation disclosures. The IRS describes the Form 990’s purpose as providing information to the public about a tax-exempt organization’s operations and compliance (Internal Revenue Service). A ministry that resists sharing basic public filings is creating an avoidable credibility problem.

Ask governance questions that connect to financial integrity

Financial reports are downstream from governance. Donors can ask how the board oversees budgets, whether there is an audit committee or independent financial oversight, and how conflicts of interest are disclosed and managed. A child sponsorship model can be emotionally compelling, which makes governance even more important: when donors are moved by compassion, they can become less likely to demand accountability. Scripture does not treat compassion and discernment as rivals.

Donors who want to situate these questions in the broader landscape of sponsorship models and ministry practice will find useful context in Child Sponsorship Ministries. For the narrower question of how donations are categorized and applied in sponsorship programs, How Child Sponsorship Ministries Use Donations sets the financial conversation where it belongs: in the concrete mechanics of stewardship.

FAQs for What questions to ask about child sponsorship financial reports

Should we expect a child sponsorship ministry to report an exact dollar amount that goes to each sponsored child?

Not always. Some ministries provide individualized benefits and can report direct support per child. Others operate community-based sponsorship where the sponsored child anchors a package of shared services; in that model, reporting may be strongest when it shows program budgets, beneficiaries served, and in-country expenditures by category rather than a per-child transfer number. What matters is that the ministry’s reporting matches its stated sponsorship model and does not imply a one-to-one transfer if the program is designed differently.

Is a high program percentage the best indicator that a child sponsorship ministry is trustworthy?

No. Program ratios can be manipulated through classification choices, and they can punish necessary spending on safeguarding, monitoring, internal controls, and evaluation. The more reliable test is whether the ministry provides audited reporting, clear explanations of categories, and answerable detail on fund flows and restrictions. The Overhead Myth statement by major charity evaluators is a helpful corrective for donors tempted to treat a single ratio as the measure of faithfulness (GuideStar).

A donor’s questions are part of the ministry’s accountability

Child sponsorship invites Christians into long obedience in the same direction: steady giving, steady prayer, steady concern for a child’s flourishing. Financial reports are where that concern becomes disciplined stewardship. The ministries most worthy of trust do not merely display generosity; they submit their finances to light, accept scrutiny without resentment, and treat clarity as a form of respect for the Church that funds the work.