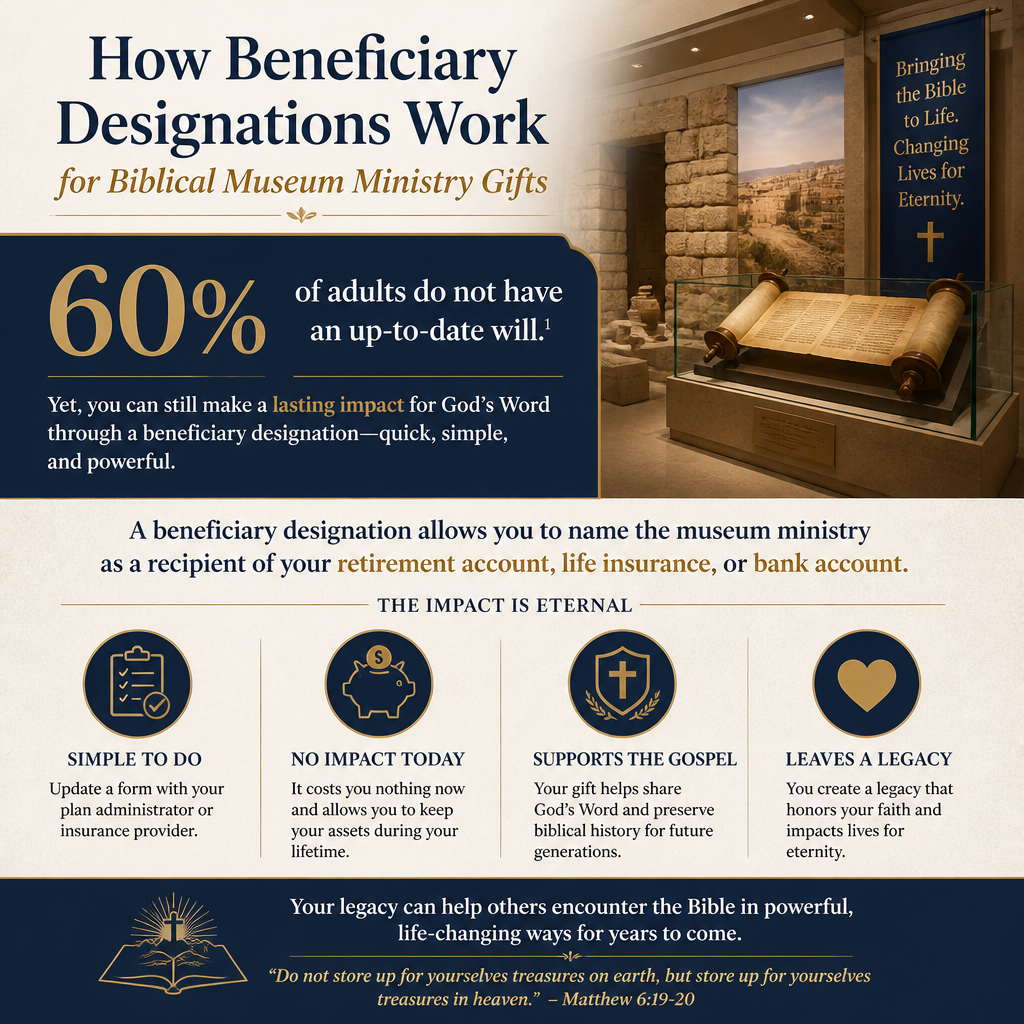

How beneficiary designations work for biblical museum ministry gifts is both simpler and more consequential than most donors assume. These designations can move a meaningful gift to a ministry without the delays, costs, and contestability that sometimes accompany estate administration.

For Christian donors who care about the public witness of Scripture, biblical museums and related ministries can serve a distinct calling: placing the text and story of the Bible before the eyes of the next generation, often in cultural settings where Christian claims are treated as implausible or irrelevant. Yet legacy gifts require more than good intentions. They require clarity, documentation, and a sober evaluation of whether a ministry’s governance and theology can carry donor intent faithfully across time.

Why beneficiary designations matter for biblical museum ministries

What a beneficiary designation is and what it is not

A beneficiary designation is a legal instruction attached to a specific asset—commonly a retirement account, life insurance policy, donor-advised fund, or bank or brokerage account—that names who receives that asset at death. The instruction sits with the account custodian or insurer, not primarily with a will.

What this means in practice is straightforward: if the designation is valid and current, the asset passes directly to the named beneficiary. In many cases it does not pass through probate, and it is usually not governed by the distribution terms in a will unless the beneficiary designation itself points there.

Why this tool fits a ministry-minded estate plan

Scripture consistently frames wealth as stewardship entrusted for a season, not possession secured for a lifetime. Jesus’ warnings about money’s power are not abstract; they are pastoral realism (Matthew 6:19–21). Beneficiary designations can be one disciplined way to align assets with convictions, especially when a donor wants a portion of their estate to strengthen gospel work beyond their lifetime.

For biblical museum ministries, beneficiary designations often align with a donor’s desire for focus. Instead of leaving a general residue gift that may be reduced by estate expenses or contested family expectations, a designated asset can express intent with precision.

Which assets commonly use beneficiary designations

Retirement accounts and why they are frequently used for charitable gifts

Traditional IRAs, 401(k)s, and similar retirement accounts are among the most common assets transferred by beneficiary designation. They can also be among the most tax-sensitive assets for heirs. For many families, leaving retirement assets to individual heirs can generate taxable income as distributions occur, while leaving some or all of those assets to a qualified charity may avoid that income tax burden.

The harder question is not whether this can be efficient, but whether it reflects the donor’s whole picture: family responsibilities, charitable commitments, and the timing of ministry needs. Estate planning counsel is essential, because tax outcomes and distribution rules vary by asset type, jurisdiction, and household situation.

Life insurance, payable on death accounts, and brokerage accounts

Life insurance proceeds typically transfer by beneficiary designation. Bank accounts may allow “payable on death” instructions, and many brokerage accounts allow “transfer on death” designations. These tools are often used when a donor wants to make sure a specific amount reaches a ministry quickly, or when they want to reduce administrative complexity for their executor.

Donor-advised funds have their own successor and beneficiary features, and foundations have governing documents that control distributions. These vehicles can be powerful, but they add layers of governance that should be reviewed carefully if the donor’s goal is a direct gift to a biblical museum ministry.

- Traditional IRA or Roth IRA beneficiary designations

- 401(k), 403(b), and other employer plan beneficiary forms

- Life insurance primary and contingent beneficiaries

- Payable on death and transfer on death registrations

- Donor-advised fund successor and charitable grant instructions

How the designation process works in practice

Step one is always the custodian’s form

Beneficiary designations are implemented through the account custodian or insurer’s process. A will cannot “override” a valid beneficiary designation on file with the institution holding the asset. This is why donor intent sometimes fails: the estate plan is updated, but the beneficiary forms are not.

What this means in practice is that donors should treat beneficiary designations as part of their core stewardship documentation. That includes keeping confirmation pages, noting the effective date, and storing them with the same seriousness as a will or trust.

Primary and contingent beneficiaries and why they protect intent

Most forms allow both primary and contingent beneficiaries. A primary beneficiary receives the asset if they survive the account holder; a contingent beneficiary receives it if the primary beneficiary cannot. For ministry gifts, contingencies matter: a named ministry could merge, dissolve, change name, or lose tax-exempt status over time.

Christians genuinely disagree about how tightly a donor should restrict a gift. Some prefer broad discretion to let leaders meet the moment; others prefer specific program restrictions to preserve purpose. Either approach can be faithful. The key is to write in a way that remains administrable if circumstances change.

Risks, tensions, and due diligence for ministry beneficiary gifts

When the ministry changes and donor intent becomes contested

Legacy gifts are exposed to time. Boards turn over. Missions statements are edited. Theological clarity can fade by accretion rather than open denial. A donor’s desire to strengthen biblical public witness can be undermined if a ministry’s doctrine, leadership practices, or transparency weakens.

That is one reason due diligence is not suspicion; it is stewardship. Most Trusted exists precisely because donors need more than marketing language. We evaluate ministries against The Most Trusted Standard, a 15-criteria framework spanning faith commitments, financial integrity, governance and leadership, and transparency and effectiveness. Where a donor is considering a significant beneficiary gift, this kind of verification helps ground the decision in evidence rather than impression.

For donors reviewing the wider landscape, it is often helpful to start with Biblical Museum Ministries and identify organizations whose doctrinal commitments and reporting practices can be examined with care.

Administrative missteps that silently defeat a generous plan

Some of the most painful failures are not theological but procedural: an outdated beneficiary form, a missing percentage allocation, a charity name that does not match the IRS record, or a designation that lacks contingency instructions. Executors cannot correct these errors easily, because the contract between the account holder and the custodian typically governs.

Donors should also consider privacy and family dynamics. A beneficiary designation is not usually made public during life, but it can become known after death. Some families interpret secrecy as distrust. Others recognize discretion as prudence. Wisdom often includes pastoral preparation: clear communication where appropriate, and clear documentation regardless.

Making a beneficiary gift that honors Scripture and strengthens public witness

Clarity about mission fit and theological commitments

Biblical museum work sits at an intersection of evangelism, education, scholarship, and cultural engagement. That intersection creates genuine tensions: how to present contested historical claims responsibly, how to treat artifacts ethically, how to avoid sensationalism, and how to speak of Scripture with reverence rather than spectacle. Donors should expect a serious ministry to name these tensions rather than dismiss them.

We recommend reviewing a ministry’s statement of faith, governance practices, and public reporting before naming it as a beneficiary. This is not mere formality. Scripture assumes that leaders are accountable (James 3:1) and that financial dealings should avoid reproach (2 Corinthians 8:20–21). A legacy gift is a form of entrusted power; it should be directed toward institutions that welcome accountability.

Coordination with advisors and documentation that can be executed

Beneficiary designations are not a substitute for legal counsel. They are a tool within an integrated plan. Donors should coordinate with an estate planning attorney and, where appropriate, a tax advisor to ensure that the designation aligns with the rest of the estate plan, including any trust provisions, specific bequests, and family support commitments.

Donors who are considering legacy options in this field often benefit from reviewing the broader practices associated with Legacy and Planned Giving for Biblical Museum Ministries, particularly where gifts may be restricted, where ministries may operate internationally, or where multiple organizations are being supported.

Some donors also find it clarifying to revisit the basic stewardship principle that generosity is not only about impact but about faithfulness. The New Testament frames giving as an act of worship shaped by integrity and discernment, not merely by sentiment (2 Corinthians 9:6–8).

FAQs for How beneficiary designations work for biblical museum ministry gifts

Do beneficiary designations override a will for ministry gifts?

In most cases, yes. A valid beneficiary designation on file with the account custodian typically controls who receives that asset, even if a will says something different. That is why beneficiary forms should be reviewed whenever an estate plan is updated, and why donors should keep written confirmation of the designation.

How can we protect a beneficiary gift if a biblical museum ministry changes over time?

There are several approaches, and the best one depends on the size of the gift and the donor’s priorities. Some donors name a broad organizational purpose, others restrict to a program area, and many include contingencies such as an alternate beneficiary. For significant gifts, legal counsel can help draft language that remains administrable if the ministry merges, renames, or no longer meets the donor’s doctrinal expectations.

A measured legacy that can be carried out

Beneficiary designations work best when they are treated as a serious stewardship document: current, clear, coordinated with the broader estate plan, and grounded in careful due diligence. For biblical museum ministry gifts, the aim is not only efficiency but faithfulness—directing resources toward institutions that can preserve donor intent, maintain integrity, and strengthen the public witness of Scripture for those who come after us.