Christian stewardship services recommend giving appreciated assets because it is one of the clearest ways to align faithful generosity with wise stewardship under today’s tax rules. For donors with long-held stock, mutual funds, or real estate, the difference between giving cash and giving an appreciated asset is often the difference between a straightforward gift and a gift that is both larger and less costly to the donor.

That recommendation is not a way to spiritualize tax minimization. Scripture treats stewardship as morally serious because it concerns both love of neighbor and accountability before God. Jesus’ parable of the talents assumes that faithful servants handle entrusted resources with prudence and purpose, not waste or negligence. What this means in practice is that Christian donors are right to ask how a gift can do the most good while keeping faith with honest reporting and lawful compliance.

Why appreciated assets often give more without asking you to spend more

The basic mechanics are simple and consequential

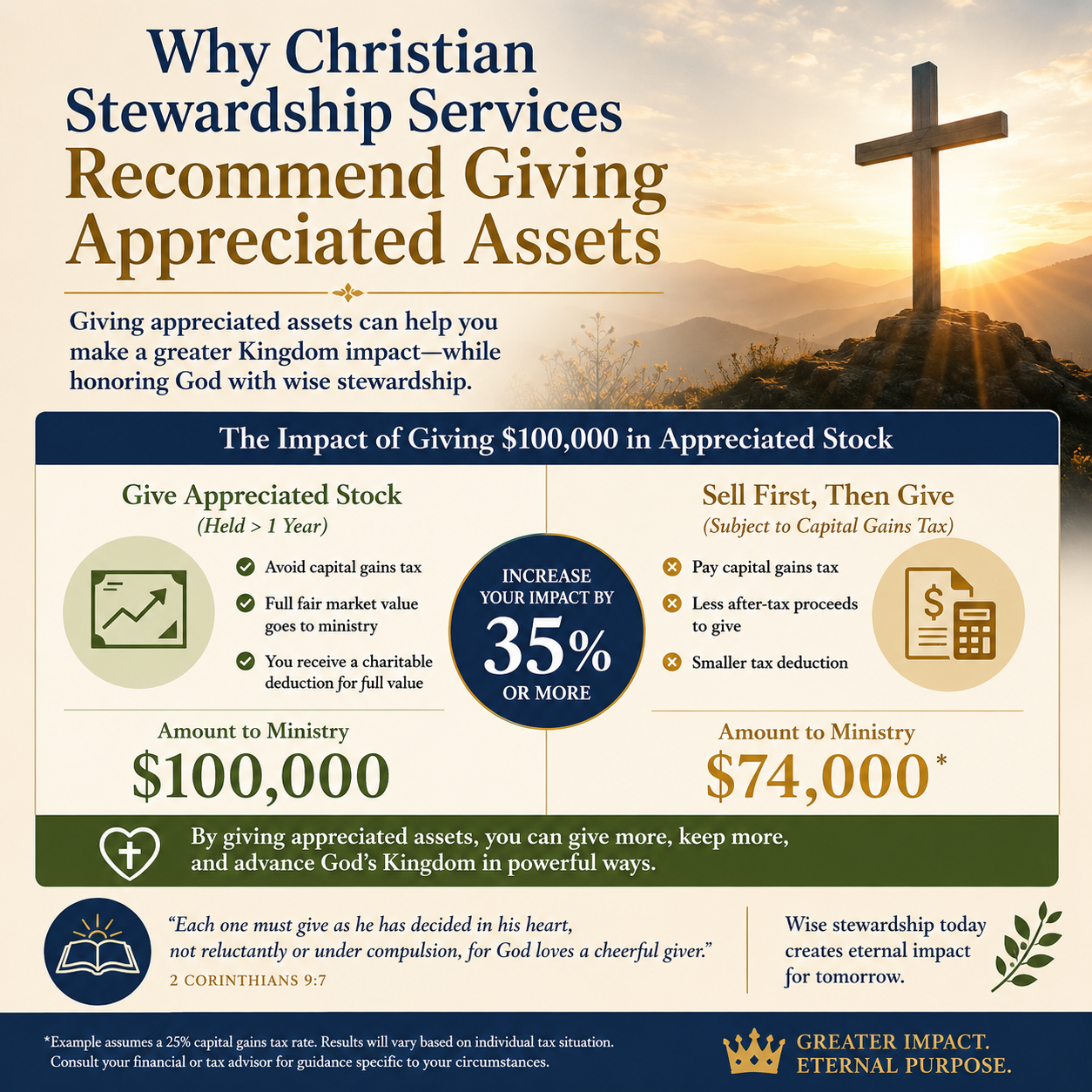

When you sell an appreciated asset, you generally realize a capital gain and owe tax. When you donate the asset directly to a qualified nonprofit, you can generally avoid capital gains tax on the appreciation, and you may be eligible to deduct the fair market value if you itemize and meet IRS requirements. The result is that the ministry receives more than it would have received if you first sold the asset and then gave the after-tax proceeds.

The IRS distinguishes between short-term and long-term gains, and it imposes different deduction limits depending on the type of property and the kind of recipient organization. Those details matter, especially for high-capacity donors, but they do not change the central logic: giving the asset itself can preserve value that would otherwise be lost to tax friction. The IRS explains these rules and limitations in Publication 526.

Stewardship is not avoidance but faithful administration

Christians genuinely disagree about how much weight to place on tax considerations in spiritual decision-making. Some fear that “tax-smart giving” reduces discipleship to technique. That concern deserves respect. Yet the alternative is not purer; it can become careless. A donor who pays avoidable tax and thereby reduces what is available for gospel work has not necessarily acted more sacrificially—sometimes they have simply acted less attentively.

Stewardship services tend to frame the choice as an ordering of goods: first, clarity about mission and beneficiaries; second, confidence in the ministry’s integrity; third, a giving method that honors both generosity and prudence. That order keeps technique in its place.

Where this approach fits within tax smart Christian giving

The itemization question and the post-2017 landscape

Appreciated-asset giving often intersects with whether you itemize deductions. Since the Tax Cuts and Jobs Act increased the standard deduction, fewer households itemize, which can reduce the immediate tax benefit of charitable deductions for many donors. The policy reality is widely documented; for example, the Tax Policy Center has tracked the shift in itemization rates and charitable deduction use after the law’s passage (Tax Policy Center).

That does not make appreciated-asset giving irrelevant. Avoiding capital gains tax can still be meaningful, and many donors with appreciated assets are already in a financial profile where itemizing remains common. For others, the strategy may be episodic rather than annual: bunching charitable giving into a single year, using a donor-advised fund, or making a larger multi-year commitment during an itemizing year.

Why stewardship services emphasize planning, not impulses

Most Christian donors have experienced the tension between spontaneous compassion and disciplined consistency. A crisis appeal arrives; a family in the church needs help; a missionary writes about an urgent shortfall. Planned giving does not oppose mercy. It protects it. When we plan, we are less likely to make gifts that feel significant in the moment but are financially fragile or strategically unfocused over time.

This is one reason stewardship professionals frequently encourage donors to hold giving assets “in reserve” rather than waiting until December to decide. Appreciated assets can be transferred on a timeline, but brokerage processing, signature requirements, and valuation questions introduce delays. Planning is not merely administrative; it is how seriousness becomes concrete.

Which appreciated assets are commonly recommended and why

Publicly traded securities are often the cleanest

For many donors, the most straightforward appreciated asset is publicly traded stock or mutual fund shares held more than one year. Transfers are typically efficient, valuation is transparent, and ministries can liquidate quickly. The simplicity matters because complexity can create donor hesitation and create unnecessary administrative burden for ministries.

Stewardship services usually encourage donors to identify “highest gain, lowest basis” lots for giving. That approach preserves cash flow while directing the most tax-inefficient holdings toward ministry. Done carefully, it can become a disciplined habit rather than an occasional tactic.

Real estate and closely held business interests can be powerful but require rigor

Real estate gifts can be significant, especially for donors whose wealth is concentrated in property. They can also be complicated. Environmental issues, title complications, debt on the property, and local market risk can create burdens for a ministry. Many nonprofits will accept real estate only through a vetted process or through an intermediary that can evaluate and sell the property responsibly.

Gifts of closely held business interests can raise additional complexity: valuation, liquidity, restrictions in operating agreements, and unrelated business income tax considerations for the receiving organization. These are not reasons to avoid such gifts categorically. They are reasons to approach them with experienced counsel, clear documentation, and a candid conversation with the receiving ministry before initiating a transfer.

Integrity matters more when gifts become more sophisticated

Donors should verify ministries with the same seriousness they apply to tax planning

As donors move from cash to appreciated assets, they are often moving from smaller discretionary gifts to more consequential commitments. That shift should raise the bar for due diligence. In our work at Most Trusted, we see a clear pattern: ministries that are well governed and financially transparent can accept non-cash gifts without turning them into a distraction or a source of reputational risk. Ministries that are informal, personality-driven, or unclear about controls often struggle even with routine administration, and complex gifts can expose those weaknesses.

Our verification work evaluates ministries against The Most Trusted Standard, a 15-criteria framework spanning faith commitments, financial integrity, governance, and transparency. Donors often assume that doctrinal soundness alone ensures operational faithfulness. Scripture does not permit that separation. The Pastoral Epistles, for example, tie spiritual leadership to observable credibility, order, and accountability. Operational integrity is not a substitute for faithfulness; it is one of its public proofs.

When you are weighing where to direct an appreciated-asset gift, it is reasonable to ask for the same basic evidence you would expect in any serious stewardship decision: audited or reviewed financial statements where appropriate, a qualified and independent board, a clear conflict-of-interest policy, and transparent reporting on program outcomes. The purpose is not suspicion; it is fidelity.

A short due diligence checklist for non-cash gifts

The questions below are not exhaustive, but they reflect the realities our team encounters when donors transition into more complex giving.

- Does the ministry have a written gift acceptance policy that addresses non-cash gifts?

- Will the ministry acknowledge the gift properly and avoid assigning a valuation it should not provide?

- Is there evidence of competent financial oversight and timely reporting?

- Does the ministry have clear governance practices, including conflicts-of-interest disclosure?

- Can the ministry explain how the gift will advance its mission without mission drift?

These questions do not replace prayer or pastoral counsel. They keep prayer from being used as a substitute for prudence.

How to proceed wisely without turning giving into a transaction

Hold together worship, wisdom, and witness

Christian giving is an act of worship before it is a financial event. That truth should govern our posture. Yet worship does not require naïveté. The more a gift reflects accumulated provision over years—appreciated stock, long-held property, a business interest—the more it calls for disciplined decision-making that honors both the Giver and the neighbor who will be served.

Many donors find it clarifying to separate three decisions that are often confused: (1) what causes and ministries deserve support, (2) what level of support is faithful given one’s responsibilities, and (3) what giving vehicle best transfers value with integrity. Appreciated assets belong mainly to the third decision. They do not tell you what to fund; they tell you how to fund what you have already judged worthy.

Connect giving strategy to mission confidence

Tax-smart methods can unintentionally create moral distance: the donor focuses on the instrument and forgets the mission. That is why we encourage donors to link strategy to verified trust. When you are confident that a ministry is credible, transparent, and well led, sophisticated giving becomes less about cleverness and more about capacity—freeing more resources for work that will withstand scrutiny and serve people well.

Donors who want a broader framework for evaluating ministries alongside giving method often begin with Christian Stewardship Services. For donors focusing specifically on technique and compliance questions connected to higher-impact generosity, Tax-Smart Giving Through Christian Stewardship Services provides the surrounding context where appreciated-asset giving usually belongs.

FAQs for Why Christian stewardship services recommend giving appreciated assets

Do we need an appraisal when donating appreciated assets?

Sometimes. Publicly traded securities generally do not require a qualified appraisal because fair market value is readily determined by market quotations. Non-cash gifts such as certain real estate or closely held business interests may require a qualified appraisal and additional IRS forms, depending on the value and property type. The IRS outlines appraisal and substantiation expectations for non-cash charitable contributions in its guidance and forms instructions (IRS Charitable Contributions substantiation requirements).

Is giving appreciated assets only for wealthy donors?

No. Appreciated-asset giving is most common among higher-capacity households because they are more likely to hold taxable brokerage accounts and long-term appreciated property, but the logic applies at many levels. A donor with a modest portfolio can still give shares instead of cash, and the avoided capital gains tax can make a meaningful difference. The more important question is not status but stewardship: whether the donor holds appreciated property, whether the donor itemizes or benefits from other planning approaches, and whether the recipient ministry can receive and process the gift with integrity.

Faithful generosity that respects both mission and means

Appreciated-asset giving is recommended so often because it is a rare intersection of simplicity and impact: it can increase what a ministry receives while lowering the donor’s tax cost, without compromising integrity. For Christian donors who want their giving to be both worshipful and wise, the better question is rarely whether taxes matter. The better question is whether our stewardship decisions—what we give, how we give, and whom we trust—bear the weight of the gospel we profess.