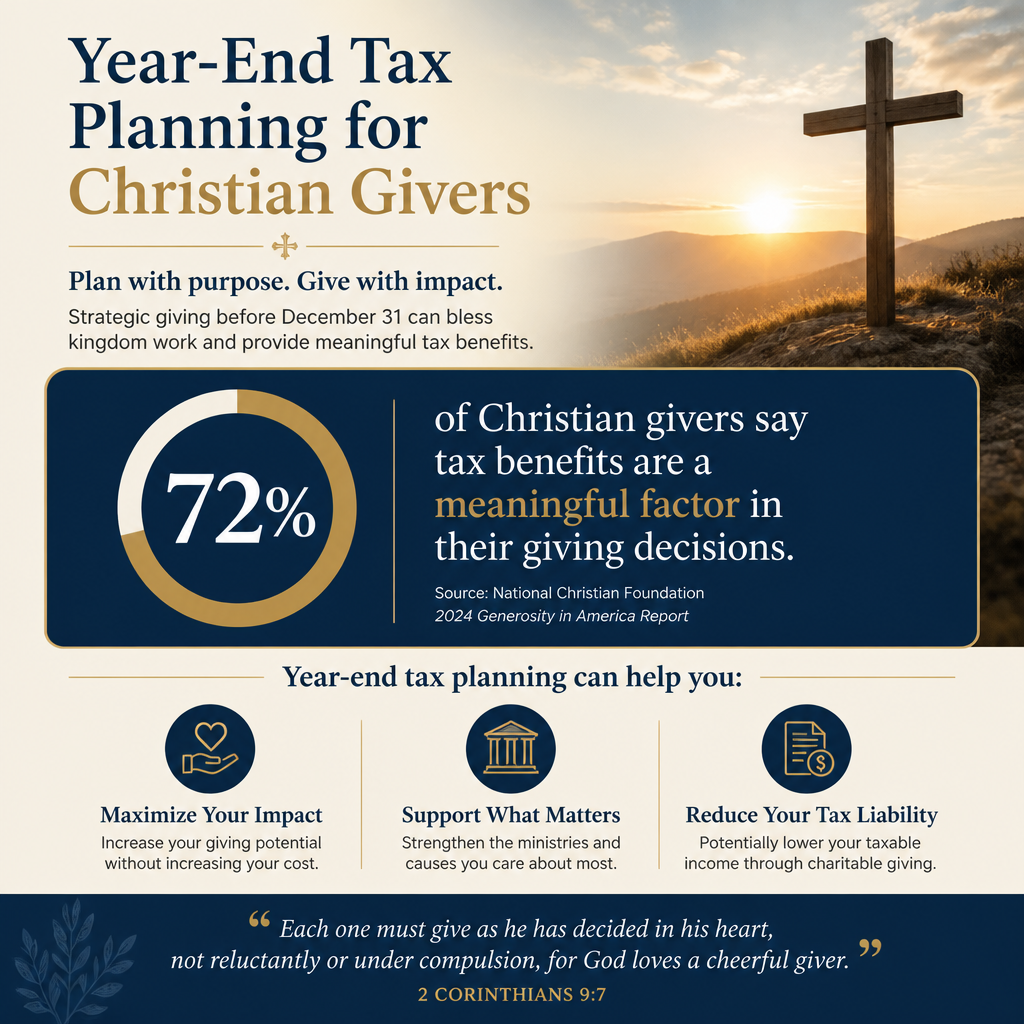

Year-end tax planning for Christian givers is not first about getting the largest deduction. It is about bringing our financial decisions into the light before God, so that our generosity reflects both love of neighbor and faithful stewardship. The tax code can either encourage disciplined giving or tempt us toward hurried, sentimental transfers in late December that we later regret.

Christian donors also face a practical tension: the causes that move our hearts are often urgent, but the organizations receiving our gifts vary widely in governance, reporting quality, and ministry effectiveness. Wise planning holds both realities together. We can pursue tax-aware generosity while also insisting on verifiable evidence that a ministry is worthy of trust.

Begin with a theological and practical definition of stewardship

Generosity is discipleship, not merely philanthropy

Scripture treats money as a spiritual matter because it reveals what we love and what we fear. Jesus’ teaching that “where your treasure is, there your heart will be also” (Matthew 6:21) is not a slogan; it is a diagnostic. Year-end planning can become a yearly examen: What have we funded, and what have we neglected? Have we given from faith or from excess?

Christians genuinely disagree about the precise relationship between tithing, freewill offerings, and New Testament liberty. Yet there is little disagreement that Christian giving is meant to be intentional, proportionate, and joyful, not impulsive or performative (2 Corinthians 9:7). Tax planning, properly ordered, supports intentionality by helping donors decide in advance what to give, to whom, and in what form.

Planning protects against last-minute giving that weakens discernment

Late-December giving often happens under time pressure, with minimal verification, and with a desire to “make the year count.” What this means in practice is that donors can unintentionally reward ministries with weak financial controls, unclear doctrine, or thin reporting, simply because they arrived first in the inbox. The stronger approach is to decide a giving strategy earlier in the year and then execute it near year-end with clarity.

For donors who want to anchor this work in a broader stewardship frame, we recommend placing tax decisions inside a fuller view of Christian Stewardship Services, where the aim is not merely compliance but faithful administration of what God has entrusted.

Understand the tax baseline before selecting a giving strategy

Itemizing versus the standard deduction shapes what is tax-relevant

For U.S. donors, whether charitable gifts will reduce taxable income often depends on whether we itemize deductions. The standard deduction is historically high, which has reduced the number of households that itemize. The Internal Revenue Service publishes the current standard deduction amounts each year; donors should confirm the year’s figures and their filing status directly through IRS.gov.

That reality does not make giving less Christian, but it does change the mechanics. Many households who give faithfully will see no incremental federal income tax benefit from additional charitable gifts if they remain below the threshold for itemizing. For some, the appropriate response is simple: keep giving, and stop treating the deduction as the primary “reason.” For others, it can justify a different cadence of giving, such as concentrating gifts into certain years.

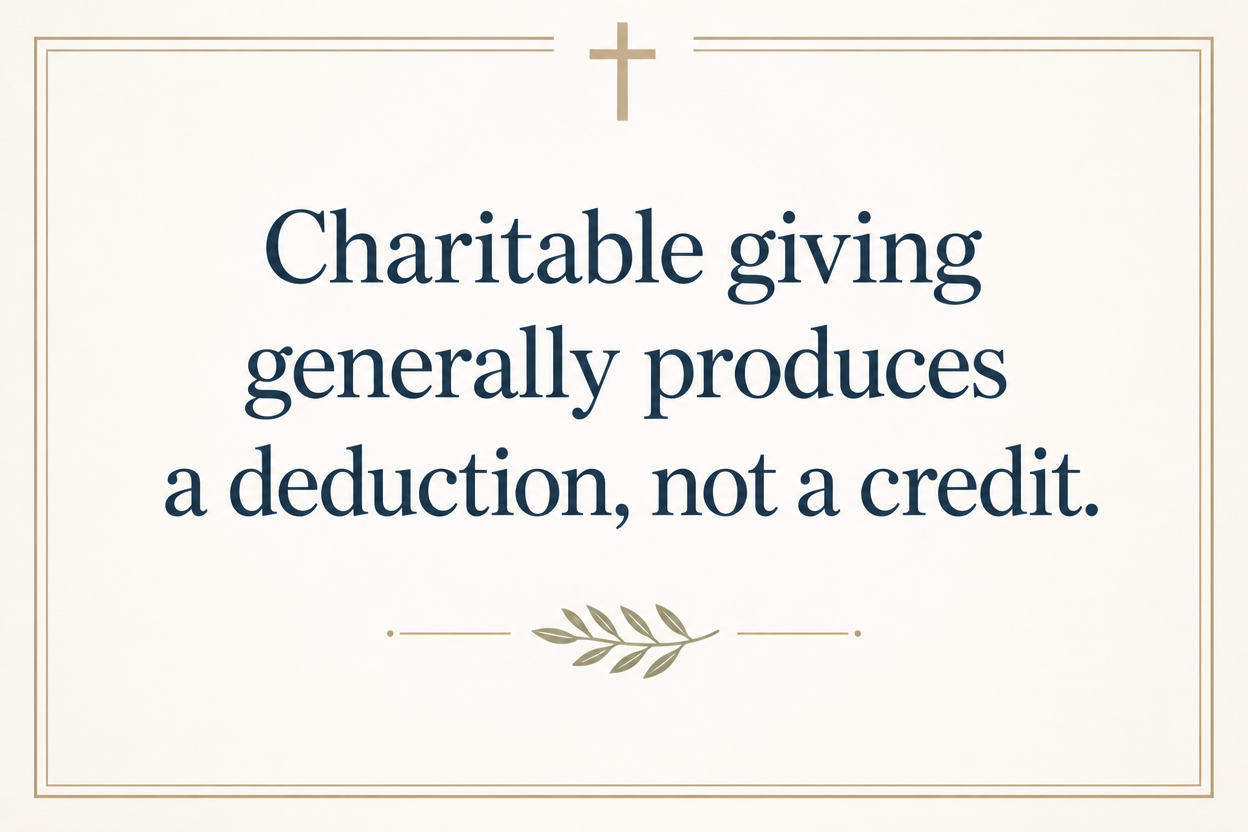

Know the difference between deduction, credit, and cash-flow impact

Charitable giving generally produces a deduction, not a credit. A deduction reduces taxable income; a credit reduces taxes owed. Sophisticated donors can still misread this, especially when charitable appeals imply a dollar-for-dollar tax “rebate.” The result can be overgiving for the wrong reason or underestimating year-end cash needs.

We recommend donors coordinate with qualified tax counsel, particularly when gifts involve appreciated assets, retirement accounts, donor-advised funds, or complex income. Good tax advice is not a substitute for Christian discernment; it is a form of prudence.

Choose gift types that align with both mission and tax wisdom

Cash, appreciated assets, and donor-advised funds each serve different ends

Cash gifts are straightforward and often essential for ministry operations. Yet for donors with appreciated securities, giving long-term appreciated assets can be materially more tax-efficient than giving cash and then selling the asset separately, because it can avoid capital gains tax while still permitting a charitable deduction when itemizing. The IRS outlines charitable contribution rules and substantiation requirements, including gifts of property, through its official guidance at IRS.gov.

Donor-advised funds can help donors “bundle” multiple years of charitable giving into a single tax year while distributing grants over time. This can be especially useful when a household’s income spikes in a particular year, or when a donor wants to commit funds for ministry without rushing to select every recipient in December. The harder question is moral rather than technical: donor-advised funds can also distance donors from the accountability of giving directly to the church and to known ministries. Used with discipline, they can strengthen generosity; used as a parking lot, they can weaken it.

Qualified charitable distributions can be decisive for some retirees

For donors who are age-eligible, a qualified charitable distribution from an IRA can satisfy required minimum distributions and reduce taxable income, which may be more valuable than an itemized deduction for those who do not itemize. Because eligibility rules and annual limits are specific, donors should confirm current requirements and execution details in IRS materials and with a tax professional; the IRS provides starting guidance at IRS.gov.

In practice, this approach can free additional resources for generosity while also reducing the “tax torpedo” effects that can push more Social Security benefits into taxable income. It is one of the clearest examples of year-end planning that is genuinely stewardship-minded, because it is both lawful and mission-directed.

- Give cash when a ministry’s near-term operations and cash flow are the priority.

- Give appreciated securities when avoiding capital gains is part of responsible planning.

- Use a donor-advised fund when you need a single-year deduction but multi-year grantmaking.

- Consider qualified charitable distributions when IRA distributions would otherwise increase taxable income.

- Document gifts carefully, including non-cash valuation and written acknowledgments.

Verify the ministry as carefully as you plan the gift

Tax compliance is not the same as ministry trustworthiness

A ministry can be legally eligible to receive charitable gifts and still be unwise to fund. The charitable sector has learned—sometimes publicly and painfully—that financial mismanagement and leadership failures can exist even where religious language is fluent and urgent needs are real. This is why year-end planning must include more than deduction mechanics.

At Most Trusted, our work is to help donors give with confidence by evaluating Christian nonprofits against The Most Trusted Standard, a 15-criteria framework covering faith commitments, financial integrity, governance and leadership, and transparency and effectiveness. Across our verification work, we observe that ministries that welcome scrutiny tend to have clearer reporting, stronger internal controls, and more stable leadership practices over time. None of these guarantees spiritual fruit, but they reduce preventable risks that harm beneficiaries and disillusion donors.

Ask questions that respect both Scripture and fiduciary reality

Christian donors are not merely consumers; we are stewards. That implies a duty of care in selecting recipients. The New Testament’s concern for integrity in handling funds is explicit—Paul took pains to administer offerings in a way that would be honorable “not only in the Lord’s sight, but also in the sight of man” (2 Corinthians 8:21). Mature donors should feel freedom to ask for audited financials, board governance information, conflict-of-interest policies, and evidence of program outcomes, especially for large gifts.

For those focusing specifically on giving strategies that reduce unnecessary tax friction while preserving discernment, the conversation belongs within Tax-Smart Giving Through Christian Stewardship Services, where method matters because trust matters.

Execute year-end giving with documentation and timing that withstand scrutiny

Substantiation is part of integrity

Many giving problems are not theological or strategic; they are administrative. The IRS requires different forms of substantiation depending on the gift type and size, including contemporaneous written acknowledgments for certain gifts and additional documentation for non-cash contributions. These rules change over time, and donors should confirm the current requirements directly through IRS.gov.

What this means in practice is that December generosity should include January discipline. Keep receipts, acknowledgment letters, and brokerage confirmations. For non-cash gifts, document fair market value and the date of transfer, and ensure the receiving organization provides the appropriate acknowledgment language.

Timing rules can be simple but unforgiving

Cash gifts are generally deductible in the year they are made; mail postmarks, online transaction timestamps, and brokerage settlement timing can matter. Year-end church gifts may be credited by the church when received, but the IRS standard can depend on when the donor relinquished control. Donors who intend to make a significant gift in the final week of the year should plan for processing delays, holiday office closures, and brokerage deadlines.

We recommend treating the calendar not as a constraint to resent, but as a prompt toward earlier discernment. When donors decide recipients and methods by early December—or earlier—they reduce the likelihood of errors, disputes, and regretted gifts.

FAQs for Year-end tax planning for Christian givers

Should Christians give differently at year-end to reduce taxes?

Christians should give intentionally year-round, but year-end can be an appropriate moment to complete planned gifts and to evaluate whether our giving matches our convictions. Tax considerations may influence the form or timing of a gift, particularly for donors who itemize deductions, hold appreciated assets, or are eligible for qualified charitable distributions. The controlling question is not “How do we lower taxes?” but “How do we give faithfully, lawfully, and with clear conscience?”

How can we tell whether a ministry is trustworthy before making a large December gift?

Start with verifiable transparency: governance oversight, clear financial reporting, and evidence that funds are used as represented. Ask for audited financial statements where appropriate, review the ministry’s board structure and conflict-of-interest practices, and look for clear explanations of program outcomes rather than only compelling stories. Donors should also consider independent verification; Most Trusted exists to evaluate ministries against The Most Trusted Standard so donors can give with greater confidence, especially when time pressure tempts superficial diligence.

A faithful year-end is measured by clarity, not urgency

Year-end planning serves Christian givers best when it disciplines our generosity rather than directing it. The aim is a form of giving that is both wise and warm: wise about tax law, documentation, and the realities of nonprofit governance; warm toward the neighbor God calls us to love. When our giving is planned, verified, and executed with integrity, the tax benefit becomes what it should be—a secondary support to a primary obedience.