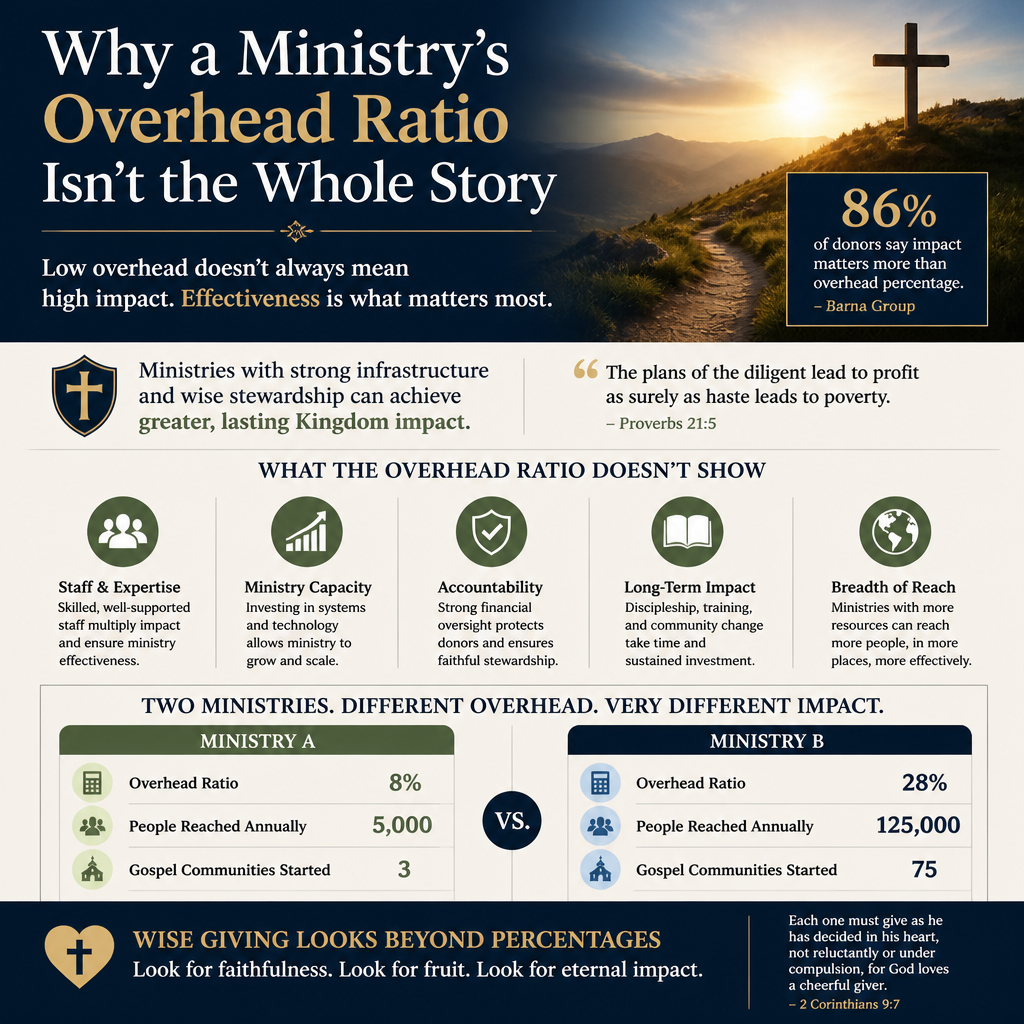

Why a ministry’s overhead ratio isn’t the whole story is not an argument for carelessness with donor funds. It is a reminder that Christian stewardship requires more than a single percentage. The overhead ratio can reveal real problems, but it can also conceal them, and it can mislead faithful donors into rewarding the wrong incentives.

Scripture does not treat money as a neutral tool. Jesus ties financial stewardship to spiritual integrity with unusual directness (Luke 16:10–11). For Christian donors, the question is not merely whether a ministry is “lean,” but whether it is honest, governed wisely, and producing fruit that matches its claims. Those are measurable realities, but they are rarely captured in an overhead line item.

What follows is a practical way to read overhead in context: when a low number is genuinely impressive, when it is a warning sign, and what evidence mature donors should seek instead. Across our verification work at Most Trusted, the ministries that withstand scrutiny are rarely those with the most polished ratios. They are those with transparent books, strong governance, and credible evidence that their work actually serves the people they claim to serve.

Overhead can be manipulated, and the incentives are not neutral

The overhead ratio is usually presented as a moral scorecard: low overhead equals faithfulness; higher overhead equals waste. The problem is that the ratio is not a moral category. It is an accounting category, and accounting categories are shaped by judgment calls that can be made well or made opportunistically.

A ministry can shift costs between “program” and “administration” through allocation methods that are technically permissible but misleading in practice. Fundraising expenses can be classified as “program education.” Executive time can be allocated heavily to “program” even when leadership is primarily raising funds or managing internal operations. None of this requires outright fraud to distort the picture donors see.

The broader nonprofit field has publicly warned donors about this dynamic for years. In 2013, Charity Navigator, GuideStar, and the BBB Wise Giving Alliance released a joint statement rejecting the idea that overhead alone is a meaningful measure of nonprofit performance, commonly referred to as “The Overhead Myth.” Charity Navigator, GuideStar, and BBB Wise Giving Alliance, “The Overhead Myth”. Their point was not that overhead is irrelevant, but that single-metric giving pressures organizations to underinvest in the very systems that make integrity and effectiveness possible.

Low overhead can be a symptom of underinvestment

Many donors have encountered ministries that feel chronically brittle: high staff turnover, inconsistent reporting, weak internal controls, and an overreliance on a charismatic founder to keep the whole operation functioning. Sometimes those weaknesses are spiritualized as “simplicity” or “lean ministry.” Sometimes they are celebrated with unusually low overhead ratios.

Yet adequate finance staffing, independent audits when appropriate, secure donor data practices, and competent program evaluation are not luxuries. They are part of loving our neighbor in organizational form. When donors pressure ministries to starve these functions, the predictable result is not holiness; it is fragility.

High overhead can represent real capacity, or real waste

There is a legitimate concern on the other side. A ministry can expand administrative layers, pay above-market compensation without justification, rent premium facilities, or persist with weak internal discipline. Those realities often do appear as “overhead,” and donors are right to ask hard questions.

The point is that overhead is an invitation to inquiry, not a verdict. Mature stewardship asks what a ministry is buying with those costs and whether the spending is governed, disclosed, and aligned with mission.

The “starvation cycle” makes ministries harder to trust, not easier

Nonprofit leaders have long described a cycle in which donors demand unrealistically low overhead, ministries comply by underreporting true costs or underinvesting in capacity, and the resulting weakness reduces impact and increases risk. A well-known articulation of this dynamic appears in Stanford Social Innovation Review’s treatment of the “Nonprofit Starvation Cycle,” which explains how the overhead fixation distorts both reporting and performance. Stanford Social Innovation Review.

Christian donors should take this seriously because the Church’s credibility is implicated. When ministries fail due to weak controls, inadequate oversight, or exaggerated claims, the public does not parse the accounting categories. They conclude that Christian charity cannot be trusted. That reputational harm is not abstract; it affects the next ministry that seeks to serve faithfully in the same community.

There is also a theological problem embedded in the starvation cycle. Scripture commends prudence, not performative austerity. Joseph’s administrative wisdom in Genesis is not presented as a regrettable overhead expense; it is the means by which God preserves life in famine (Genesis 41). Wise governance and competent administration can be instruments of mercy.

Underfunded systems increase the risk of moral failure

Financial controls are not merely technical. They are moral guardrails. Segregation of duties, documented approval processes, regular reconciliation, and independent oversight help protect a ministry’s staff from temptation and protect beneficiaries from harm. When a ministry does not invest in these basics, the risk is not only financial mismanagement; it is scandal.

Donors sometimes assume that “spiritual” organizations are less likely to need controls. Scripture assumes the opposite. The pastoral epistles require leaders to be above reproach, not only in personal character but also in public credibility (1 Timothy 3:7). Organizations must be structured so that integrity is plausible under pressure.

Underfunded evaluation can create unintentional harm

Some ministries serve vulnerable people: children, the incarcerated, refugees, survivors of exploitation, families in crisis. In these contexts, good intentions can harm when programs are poorly designed or lack safeguards. The When Helping Hurts framework, articulated by Steve Corbett and Brian Fikkert, has shaped much of the Christian conversation about dependency, dignity, and the unintended consequences of aid. When Helping Hurts.

Evaluation is part of humility. It is the discipline of asking whether the ministry’s approach is actually helping, and whether it is doing so in a way that honors the agency of the people served. That work costs money, and it will never be reflected well in a simplistic overhead contest.

What overhead does tell you, and how to read it carefully

The overhead ratio still matters. It can reveal whether a ministry is spending in alignment with its stated purpose. It can flag a fundraising model that is consuming an unhealthy share of revenue. It can expose a top-heavy structure that should be questioned. The key is reading the number alongside other evidence.

Start with consistency and trend, not a single year

A single-year overhead spike can be appropriate: a new finance hire, a one-time legal expense, an upgrade to donor database security, an audit initiated to meet a grant requirement, or the cost of building a governance structure strong enough for growth. Donors should ask whether the ministry can explain the change clearly and document it.

Patterns matter more than snapshots. An organization that oscillates wildly year-to-year may have unstable revenue or weak planning. An organization that reports consistently “perfect” ratios may be allocating costs in ways designed to impress rather than to inform.

Compare overhead to complexity of mission

A Bible translation organization, a crisis pregnancy center, a global medical mission, and a prison discipleship ministry all require different kinds of staffing, compliance, and risk management. Donors should expect overhead to vary by type of work. A ministry operating in multiple countries with child safeguarding requirements and cross-border payments will require more administration than a local ministry running a single program with volunteers.

For sophisticated donors, the question becomes: does the administrative capacity match the ministry’s operational risk? If a ministry works with children but cannot articulate safeguarding policies, training, and reporting procedures, the overhead ratio has become a distraction from what actually protects the vulnerable.

Ask what is embedded inside program expenses

Some ministries report high “program” percentages because their program is essentially grantmaking or pass-through giving. That can be legitimate, but it requires transparency. If a ministry’s program spending consists largely of funds sent to partners, donors should ask: how are partners vetted, monitored, and audited? How does the ministry prevent fraud in the field? What evidence exists that the money is used as intended?

In other cases, program spending may include significant events or media production. Again, this can be legitimate. But the accountability question remains: what outcomes are being pursued, and what evidence supports the ministry’s claims?

What mature Christian donors should examine instead of fixating on overhead

Christian donors are not merely purchasers of charitable services. We are stewards who will give an account. That accountability does not require suspicion, but it does require discernment. Overhead is one small part of a wider due diligence posture.

Financial integrity and internal controls

Donors should ask whether the ministry has basic controls that make mismanagement less likely. Practical indicators include: an independent board that reviews financials, documented policies for expense approvals, clear segregation of duties, and credible external financial review when scale and complexity warrant it.

For larger ministries, audited financial statements can provide meaningful assurance when the audit is conducted by a reputable firm and accompanied by a clean opinion. For smaller ministries, an audit may be financially impractical; in that case, donors can still look for disciplined bookkeeping, transparent reporting, and evidence that leaders welcome oversight rather than resist it.

Governance that restrains power

Many ministry failures are governance failures before they are financial failures. A board that is composed entirely of family members or close friends, a founder who cannot be questioned, or a structure with no meaningful accountability invites harm. The New Testament’s concern for qualified, accountable leadership is not theoretical (Titus 1:7–9). Governance is one way the Church embodies that concern institutionally.

Donors should ask basic questions: Is the board independent? Are conflicts of interest disclosed and managed? Does the board meet regularly and document oversight? Does the ministry have a succession plan that does not treat the organization as personal property?

Transparency that allows verification

Trustworthy ministries make it possible for donors to verify claims. They publish financial statements, explain program strategy in plain language, and name limitations honestly. They do not hide behind spiritual language to avoid legitimate questions.

Transparency is not the same as information overload. A ministry can publish many pages of marketing content and still be opaque on the matters that most affect donor trust: governance, financial reporting, safeguarding, and measurable outcomes.

Effectiveness that is appropriate to the ministry’s work

Not every ministry outcome is quantifiable, and donors should not demand a false precision that distorts discipleship into metrics. Yet ministries still make claims, and claims require evidence proportionate to their weight. A ministry claiming thousands of conversions should be able to explain what it means by “conversion,” how follow-up and church integration occur, and what accountability exists for reporting from the field.

A ministry claiming to rescue trafficking victims should be able to document safeguarding standards, referral pathways, and partnerships with qualified professionals. A ministry running short-term mission trips should be able to explain how it avoids displacing local labor, weakening local churches, or treating communities as a backdrop for donor inspiration.

How The Most Trusted Standard approaches overhead in context

At Most Trusted, we do not treat the overhead ratio as a proxy for trustworthiness. We treat it as one data point that must be interpreted alongside governance quality, financial integrity, faith commitments, transparency, and evidence of effectiveness. The Most Trusted Standard is a 15-criteria framework designed to test whether a ministry’s public claims can be substantiated and whether its structure supports long-term faithfulness.

In practice, that means we examine how a ministry’s financial reporting is produced and reviewed, whether leadership compensation and related-party transactions are handled transparently, whether the board functions independently, and whether the ministry communicates candidly about results and limitations. A ministry may have modest overhead and still fail these tests. Another may have higher overhead because it invests in compliance, safeguarding, and evaluation—and be substantially more trustworthy as a result.

This approach also honors a Christian moral intuition many donors share: we are not merely trying to minimize cost; we are trying to maximize faithfulness. Faithfulness includes prudence, truth-telling, and care for the vulnerable, not only frugality. The goal is not to excuse inefficiency. The goal is to avoid rewarding appearances over integrity.

FAQs for Why a Ministry’s Overhead Ratio Isn’t the Whole Story

Is overhead ratio ever a red flag for a ministry?

Yes. An unusually high share of spending on administration or fundraising can indicate misalignment with mission, weak discipline, or an unsustainable revenue model. The responsible response is to ask for clear explanations and supporting documents rather than assuming the ratio alone proves wrongdoing.

Is a very low overhead ratio always good?

No. Very low overhead can mean underinvestment in basic controls, safeguarding, staff development, and evaluation. It can also reflect aggressive cost allocation that makes expenses appear more “programmatic” than they truly are. Donors should look for transparency about how expenses are classified.

What documents should donors ask to see?

At minimum, donors can reasonably ask for recent financial statements and a clear description of governance and accountability practices. For larger organizations, audited financial statements and a current Form 990 (when applicable in the United States) provide useful visibility into revenue, expenses, leadership compensation, and related-party transactions.

How should Christian donors balance trust with due diligence?

Christian charity is not naive, and due diligence is not cynicism. Scripture commends generosity alongside prudence (Proverbs 21:5). A healthy posture gives freely while still asking whether a ministry’s claims are verifiable, its leaders are accountable, and its operations protect the people it serves.

Stewardship requires more than a ratio

The overhead ratio can help donors ask good questions, but it cannot answer the central one: is this ministry trustworthy? Christian donors are not called to reward the lowest administrative spending; we are called to seek faithfulness, integrity, and fruit that can bear the weight of public witness.

When donors move beyond overhead fixation and examine governance, financial controls, transparency, and credible evidence of effectiveness, our giving becomes not only more confident but more aligned with the biblical vision of stewardship. That is how generosity strengthens the Church’s witness rather than merely funding its activity.