When Christian financial service ministries send tax receipts, they are doing more than closing an administrative loop. They are making an implicit claim about what kind of gift was received, what the donor may properly deduct, and what level of accountability the ministry is prepared to provide. For Christian donors trying to give with both faith and prudence, a tax receipt is a small document carrying significant moral and legal weight.

Scripture treats money as a discipleship matter, not a side concern. Jesus’ repeated warnings about wealth and integrity assume that God’s people can handle financial obligations without cynicism or evasiveness. The tax code is not holy writ, but truthfulness is. When ministries handle receipts casually, they invite confusion at best and dishonesty at worst—often without intending either.

Why tax receipts matter in Christian financial service ministries

Receipts clarify what was given and what was received

Many Christian financial service ministries operate in categories that feel unfamiliar: benevolence funds, debt relief, microenterprise lending, donor-advised-style accounts, member support for shared needs, or fee-for-service counseling. In these models, donors can mistake any transfer of funds for a charitable contribution. A tax receipt is where a ministry either corrects that assumption or quietly reinforces it.

From a compliance standpoint, the IRS expects contemporaneous written acknowledgment for charitable contributions of $250 or more, and the acknowledgment must state whether the donor received goods or services in exchange for the gift. This is not a best practice; it is a basic requirement for substantiation. The IRS explains these requirements in its guidance on charitable contributions at IRS.gov.

Receipts also signal the ministry’s posture toward transparency

Across our verification work at Most Trusted, we observe that ministries that take financial integrity seriously treat receipting as part of their accountability culture. They send acknowledgments promptly, present them clearly, and make it easy for donors to reconcile year-end statements with actual giving. They do not rely on donor confusion to increase revenue.

Where receipting is inconsistent, donors often discover other gaps: unclear restrictions, vague explanations of how funds are allocated, or an absence of audited financial statements. Those issues extend beyond taxes into trustworthiness itself—particularly when a ministry positions its services as “Christian” and therefore implicitly worthy of confidence.

What a proper receipt should include and what it should avoid

Core elements donors should expect

A solid acknowledgment letter is not complicated, but it must be specific. Donors should be able to understand, without calling the ministry, whether the gift is deductible and what exactly was provided in return.

- The ministry’s legal name and tax status (typically a 501(c)(3) designation if applicable)

- The date of the contribution and the amount of cash given (or a description of non-cash property, without assigning value)

- A clear statement that no goods or services were provided in exchange, or a good-faith estimate of their value

- The donor’s name as the ministry has it on record, so records can be matched

- Year-end summaries that align with the donor’s actual transactions and do not double-count refunds or reversals

These features are not mere bureaucracy. They are the difference between a donor confidently stewarding resources and a donor scrambling at tax time, unsure what can be claimed. For donors who give generously across multiple ministries, clarity reduces the temptation to “round up” on deductions in ways that do not honor the truth.

Common errors that create real risk

The most frequent mistakes we see come from ministries that blend charitable giving with services that feel “ministry-like” but function as personal benefit. Examples include: sending receipts for payments that are actually fees for financial coaching; labeling membership dues as donations; or issuing acknowledgments for gifts that were earmarked to pay a specific individual’s expenses when the donor effectively selected the beneficiary.

These are not merely technicalities. Donors can lose a deduction, and ministries can invite regulatory scrutiny if they routinely receipted non-deductible payments as charitable gifts. The goal is not fear. The goal is integrity with the facts.

When a payment is a donation and when it is not

Donation versus purchase

In Christian financial service settings, the line between a gift and a purchase can blur because the “product” may be pastoral or educational rather than tangible. The IRS, however, does not treat spiritual language as a substitute for economic reality. If a donor receives a specific service primarily for their own benefit, the payment often resembles a fee more than a charitable contribution.

This matters in budgeting as well. A ministry that depends heavily on program fees should present that model plainly, rather than collecting revenue through “donations” that are functionally required payments. Donors are generally willing to pay for legitimate services. What they resist is ambiguity.

Restricted gifts, designated gifts, and the donor’s control

Donors also need to distinguish between a restricted gift and a gift they control. Restrictions are legitimate: a donor can give for a program, a geography, or a general category, while leaving the ministry with discretion inside that boundary. Problems arise when the donor’s direction becomes so specific that the ministry is effectively acting as a pass-through for a private benefit.

Christians genuinely disagree about the best models for meeting needs—direct support, pooled funds, mutual aid, and structured charitable programs each have strengths and weaknesses. But the tax treatment hinges on control and benefit. A well-governed ministry will explain, in writing, how designations are handled and whether the ministry retains full discretion consistent with charitable purpose.

Donors who want to evaluate the broader ecosystem of accountability in this space can begin with Christian Financial Service Ministries, where the category differences and common risk points become clearer.

Timing and delivery issues donors should anticipate

Year-end statements and the realities of processing

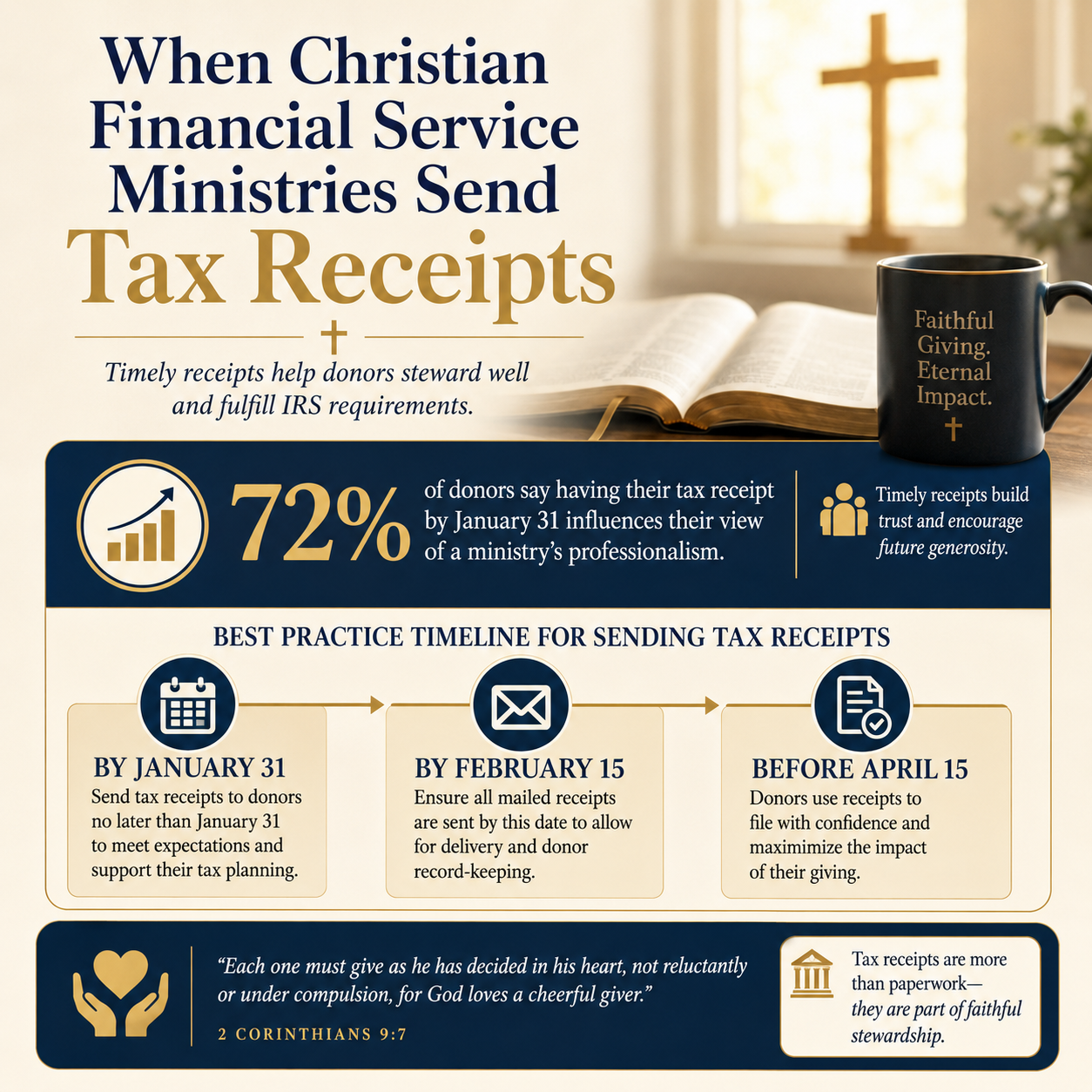

Most ministries send annual statements in January, after year-end reconciliation. Delays are not automatically suspicious; they can reflect legitimate processing constraints, holiday giving volume, or transitions in donor management systems. What matters is whether the ministry communicates clearly and whether the final statement corresponds to actual donation dates rather than the date a check was opened or a batch was processed.

For cash-basis donors, the gift date typically follows when the contribution is made—such as when a credit card is charged or a check is mailed—rather than when the ministry deposits the funds. Ministries should be careful in how they date gifts, and donors should keep their own supporting records. The IRS summarizes recordkeeping expectations for charitable contributions at IRS.gov.

Non-cash gifts require different documentation

Donating stock, vehicles, or other property can be a powerful stewardship decision, but receipting rules differ. Ministries should describe the property received without assigning a value, and donors may need qualified appraisals for certain gifts. If a ministry offers complex giving options, it should publish clear guidance and encourage donors to consult qualified tax professionals for their specific circumstances.

The theological issue beneath this is straightforward: Christians should not structure giving to create the appearance of generosity while obscuring the substance. A ministry that helps donors give wisely should also help them give truthfully.

How Most Trusted evaluates receipting as part of financial integrity

Receipting is not the whole story, but it is diagnostic

Most Trusted exists to help donors give with confidence by evaluating ministries against The Most Trusted Standard, a 15-criteria framework covering faith commitments, financial integrity, governance, and transparency. Tax receipts sit in a narrow administrative category, but they often reveal how a ministry thinks about accountability more broadly.

The ministries that meet The Most Trusted Standard tend to show the same habits in multiple places: clear policies, consistent documentation, and an instinct to explain rather than obscure. When they make mistakes, they correct them promptly and in writing. These patterns matter because donors are not merely funding outcomes; they are entrusting resources to leaders who must be faithful with what they receive.

What donors can ask without suspicion

Christian donors sometimes hesitate to ask questions because scrutiny can feel uncharitable. Scripture does not require naïveté. It commends prudence, honesty, and accountability—especially when money is involved. A thoughtful set of donor questions can strengthen both the donor and the ministry.

For donors working through the specifics of documentation, acknowledgments, and year-end reporting, Tax Receipts and Reporting for Donations to Christian Financial Service Ministries provides the context to ask the right questions without assuming bad motives.

FAQs for When Christian financial service ministries send tax receipts

When should a Christian financial service ministry send my tax receipt?

For a single contribution of $250 or more, donors should receive a contemporaneous written acknowledgment before the donor files the return for that year. Many ministries also send an annual summary in January. If a receipt is delayed, donors should confirm whether the ministry provides online access to giving history and whether the acknowledgment meets IRS substantiation requirements as described at IRS.gov.

What should we do if a receipt seems wrong or unclear?

Ask the ministry for a corrected acknowledgment in writing and keep the correspondence with the donor’s records. If the payment was actually a fee for services or provided a substantial benefit, the ministry should not represent it as a fully deductible charitable contribution. When the situation is complex—especially with designated gifts, non-cash contributions, or benefits received—donors should consult a qualified tax professional rather than relying on informal guidance.

Giving with integrity requires documentation worthy of trust

Tax receipts do not sanctify a ministry, and they do not replace discernment. They do, however, force clarity about what happened: what was given, what was received, and who controlled the use of funds. Christian financial service ministries honor their calling when their paperwork is as truthful as their mission statements, and donors honor theirs when they insist—quietly and firmly—on that same standard.