What financial documents rescue missions should share is not a cosmetic question. For Christian donors, it is a matter of stewardship, truth-telling, and love of neighbor expressed through careful giving. Scripture treats money as spiritual terrain: Jesus warns that where our treasure is, there our heart will be also, and he commends integrity that can bear the light of day.

Rescue missions operate in a morally urgent field. They provide meals, shelter, recovery support, spiritual care, and pathways to stability for people made in God’s image. That urgency can tempt donors to accept thin reporting in the name of speed, and it can tempt ministries to view financial disclosure as a distraction from “real ministry.” The better approach holds mercy and accountability together. The missions that earn durable trust tend to treat documentation as part of ministry, because it protects guests, donors, staff, and the witness of the gospel.

Financial transparency is a form of Christian integrity

Christian donors do not give to purchase outcomes the way a consumer purchases a product. We give as stewards, answerable to God for how resources are directed toward mercy and mission. That is why financial transparency is not merely a compliance exercise. It is a public commitment to walk in the truth, especially when money is involved.

In our verification work at Most Trusted, we have seen how financial clarity strengthens ministries. It reduces suspicion, lowers the relational temperature when questions arise, and gives boards the information they need to govern faithfully. It also helps donors avoid the twin errors that distort giving: either assuming every ministry is opaque, or assuming a compelling story guarantees sound financial practice.

What donors are reasonably trying to discern

Most mature donors are not seeking perfection, nor do they assume that bigger budgets imply better faithfulness. They are trying to discern whether a mission is financially disciplined, honestly represented, and governed with appropriate oversight. Those qualities require documents that can be checked, not only narratives that can be admired.

Transparency does not mean broadcasting everything

Rescue missions must protect guest privacy, security protocols, and sometimes the dignity of staff members whose lives are intertwined with the work. Donors should not expect to see sensitive personal information, nor should missions publish details that create safety risks. The goal is verifiable, decision-useful disclosure that strengthens accountability without endangering people.

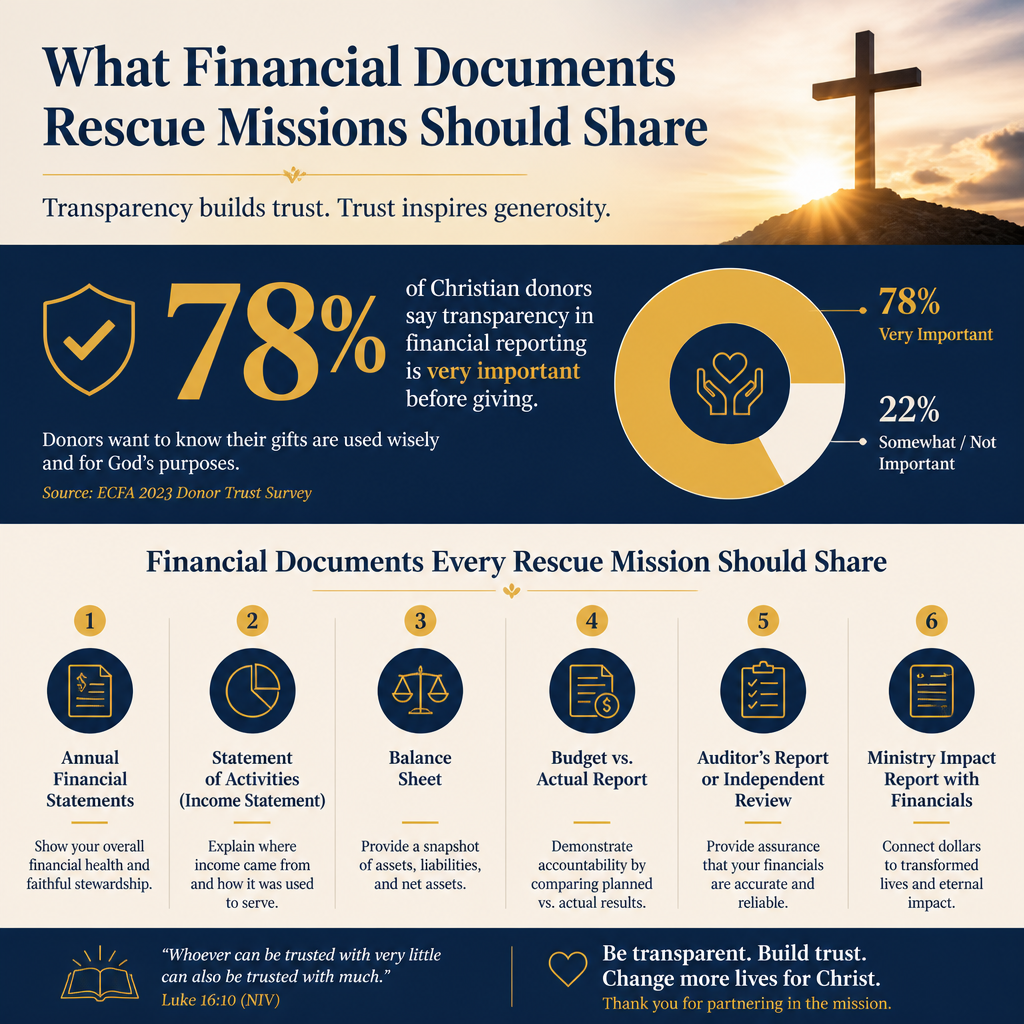

Start with core nonprofit filings and audited financials when appropriate

The baseline documents are those that establish a ministry’s public accountability and enable independent review. These are not “extra.” They are the common language of the charitable sector, and they allow donors to compare like with like across organizations.

Form 990 and related filings

For U.S. rescue missions that are required to file, the IRS Form 990 is foundational. It discloses governance practices, key compensation reporting, major program areas, and financial statements in a standardized format. Donors can access many filings through the IRS Tax Exempt Organization Search, including 990-series returns and determination letters when available. See the IRS portal at irs.gov.

Some rescue missions operate under a church or denomination and may be exempt from filing a Form 990. That exemption is lawful and sometimes appropriate, but it increases the burden on the ministry to provide alternative documentation that serves a similar accountability function. Sophisticated donors should treat “we are exempt” as an explanation, not as an endpoint.

Audited financial statements and management letters

An independent audit is not required for every ministry at every stage, but when a mission has significant revenue, complex operations, or substantial restricted funding, audited financial statements provide a level of assurance that internal reporting cannot. The audit opinion, financial statements, and notes help donors understand liquidity, debt, lease obligations, and revenue recognition practices.

For donors who want to understand what an audit does and does not guarantee, the American Institute of Certified Public Accountants provides plain explanations of audited financial statements and assurance services at aicpa.org. A mission can share the audit report and, when prudent, a summary of any material findings and corrective actions without disclosing confidential details.

Budget, reserves, and cash flow tell the operational truth

Many ministries can produce an annual report that sounds healthy while living close to insolvency behind the scenes. Rescue missions are especially vulnerable because demand can surge suddenly and because many costs are fixed: staffing, facilities, food service, insurance, and compliance. Donors who care about the stability of mercy should ask for documents that reveal operational reality.

Board-approved annual budget and midyear variance reports

A board-approved budget, paired with periodic budget-to-actual reports, shows whether leaders plan realistically and monitor performance. Donors do not need the granular line-item detail of an internal document, but a summarized version that displays major revenue streams and expense categories is often appropriate. Variance explanations matter as much as the numbers, because they show whether leadership is interpreting reality honestly.

Liquidity and reserves

Cash on hand, unrestricted net assets, and any board-designated reserves shape a mission’s ability to sustain care when giving declines. The question is not “how low can overhead go,” but “can this mission continue serving guests faithfully without lurching from crisis to crisis.” The sector has had to reckon with the damage caused by simplistic overhead fixation; Charity Navigator, Candid, and the BBB Wise Giving Alliance jointly cautioned donors against using overhead ratios as the primary indicator of performance in their widely cited “Overhead Myth” statement, archived and referenced through Charity Navigator at charitynavigator.org.

Reserve levels are contextual. A mission with a mortgage, significant facility risk, or seasonal revenue should not be evaluated by the same reserve expectations as a small outreach with minimal fixed costs. What donors should expect is transparency: a clear explanation of reserve policy, restricted versus unrestricted funds, and any material going-concern risks noted by auditors.

Document how designated gifts are protected and reported

Rescue missions regularly receive gifts for a specific purpose: a capital campaign, a new women’s shelter wing, a recovery program, or a vehicle for street outreach. Christian donors often give sacrificially to such needs, and Scripture’s warnings about dishonest weights and measures apply directly to how restricted funds are handled. The donor’s intent is not a suggestion; it is a trust.

Gift acceptance policy and restricted fund accounting

A clear gift acceptance policy sets expectations for what the ministry can responsibly receive, how it handles non-cash gifts, and when it may decline funds that create unsustainable obligations. It should also describe how restricted gifts are tracked and when restrictions can be modified, which may require donor permission or, in some cases, court action under state law.

Donors should also expect a mission to explain, in plain terms, its accounting for restricted and unrestricted funds. Audited financial statements and Form 990 schedules can support this, but many donors benefit from a short, narrative explanation paired with summary figures.

Capital projects and major campaigns

If a mission is building or renovating, it should share campaign financial updates that reconcile pledges, cash received, outstanding commitments, and project costs to date. It should also disclose whether operating funds are being used to cover capital shortfalls, or whether bridge financing has been taken on. Construction can be mission-advancing; it can also become a slow financial bleed if donors are not told the full cost.

- A campaign budget with projected costs and contingencies

- Progress-to-date reporting on funds raised and expenses incurred

- Debt disclosures, including terms and covenants in summary form

- A plan for ongoing operating costs after the project is complete

- A statement of how restricted gifts are segregated and monitored

Pair financial documents with governance and outcome disclosures

Financial documents alone cannot tell a donor whether a rescue mission is spiritually faithful, operationally sound, and effective in its stated aims. They are necessary but not sufficient. The more complete picture includes governance documents that show oversight and outcome reporting that shows whether programs are doing what the mission claims.

Governance documents that demonstrate oversight

Donors should look for evidence of an active board, meaningful conflict-of-interest practices, and clear leadership accountability. Common documents include board rosters, committee structures (especially finance and audit committees), conflict-of-interest policies, whistleblower policies, and executive compensation approval practices. These disclosures matter because concentrated authority without checks is a repeated failure point in Christian ministry.

Those who want a broader view of how faithful oversight and disclosure fit together can read more within Accountability and Transparency in Rescue Missions, where we address common governance and reporting expectations across the field.

Outcome reporting with appropriate humility

Rescue missions should report outcomes, but they should do so carefully. Human lives do not reduce to metrics, and discipleship cannot be audited like an inventory count. Still, a mission can report verifiable indicators such as nights of shelter provided, meals served, program completion counts, employment placements, or housing transitions, alongside narrative descriptions of spiritual care and community partnerships.

When missions cite community-level homelessness data, donors should expect links to authoritative sources. For example, the U.S. Department of Housing and Urban Development publishes annual Point-in-Time estimates and related homelessness reports at hud.gov. Local mission impact should not be conflated with national totals, but credible context helps donors interpret need and scope.

Across our work applying The Most Trusted Standard, we find that the healthiest disclosures do not exaggerate. They acknowledge relapse realities in recovery work, the complexity of mental illness, and the limits of any single program. Truthful reporting is not a marketing risk; it is a moral stance.

For donors who want to situate a specific mission within the wider landscape of shelter, outreach, and recovery ministries, Rescue Missions and Homeless Outreach provides the broader context where financial integrity, governance, and effectiveness intersect.

FAQs for What financial documents rescue missions should share

What if a rescue mission says it does not file a Form 990?

Some rescue missions are structured as churches or integrated auxiliaries and may be exempt from Form 990 filing requirements. In that case, donors should reasonably ask for substitute disclosures that provide comparable transparency: recent audited or reviewed financial statements, a board-approved budget with summarized year-to-date reporting, and clear explanations of restricted funds, executive oversight, and related-party transactions. Exemption from filing does not remove the stewardship obligation to be accountable.

Is an audit required for a rescue mission to be trustworthy?

An audit is not the only marker of trustworthiness, and smaller ministries may not have the scale to justify the cost. Still, as budgets grow and operations become more complex, an independent audit becomes a prudent safeguard. Where an audit is not present, donors can look for compensating controls: a strong board finance function, timely financial reporting, clear policies, and consistent public disclosure of key statements. The standard is not “audit or nothing,” but verifiable evidence proportionate to the ministry’s size and risk.

What mature transparency communicates to Christian donors

Rescue missions should share documents that allow donors to test reality: standardized filings where applicable, audited statements when appropriate, board-approved budgets and variance reporting, and clear documentation of how restricted gifts are protected. These disclosures do not replace faith; they honor it. They signal that a ministry intends to serve guests with stability, to tell the truth about money, and to welcome accountability as part of its Christian witness.