Christian medical ministry audits matter because they sit at the intersection of stewardship, credibility, and the care of real patients. Donors are not simply underwriting a budget line; they are entrusting resources that a ministry will convert into clinical care, community health, and compassionate presence that honors Christ.

Yet “audit” is often used loosely in Christian fundraising. Some ministries mean an independent financial statement audit performed under professional standards. Others mean an internal review, a compliance check, or a program evaluation. For Christian donors who want to give with confidence, the first task is to understand what kind of assurance an audit can and cannot provide.

1. What an audit is and what it is not

Audits provide assurance about financial statements

A financial statement audit is an independent examination of an organization’s financial statements, typically performed under U.S. Generally Accepted Auditing Standards. The auditor’s opinion is about whether the financial statements are fairly presented in all material respects, not whether every dollar was spent exactly as a donor would prefer. Materiality matters: auditors focus on what could reasonably influence a reader’s decision, not on every small error.

For donors, this is still meaningful. An audited set of financials indicates that the ministry is willing to submit to external scrutiny and that its reporting has been tested. It does not mean fraud is impossible; audits are designed to provide reasonable assurance, not absolute assurance. The public accounting profession is explicit about this limit, including the risk that collusion or management override can defeat controls in ways that are difficult to detect in an audit. See the AICPA’s overview of the audit process and its reasonable assurance framework.

Not every review labeled audit is an audit

Some ministries describe a “program audit” of medical teams, a “pharmacy audit” for controlled substances, or an “internal audit” of billing practices. Those can be responsible practices, but they are not equivalent to an independent financial statement audit unless conducted by an external CPA firm under recognized standards. Sophisticated donors should ask which standards were used, who performed the work, and what report was issued.

In Christian medical ministries, terms can also blur because the work spans clinical practice, missions logistics, and charity administration. A clinical quality review is important, but it answers a different question than whether the financial statements are reliable.

2. Why audits are especially consequential in Christian medical ministry

The work carries higher operational and ethical complexity

Medical ministry is not only spiritually weighty; it is operationally demanding. Ministries manage pharmaceuticals, sensitive patient data, volunteer clinicians, international partners, and cross-border supply chains. Each domain creates risk: diversion of medicines, substandard care, improper referral arrangements, or failures in safeguarding and consent. A financial audit does not directly certify clinical quality, but strong financial reporting and internal controls are often correlated with a culture that treats accountability seriously.

The Church’s commitment to mercy is not sentimental. In Matthew 25, Jesus binds care for the sick to fidelity to him. That claim should sharpen, not soften, our expectations for integrity. Donors should not accept vague assurances when ministries are handling patient lives and donor funds at the same time.

Donors face a real information imbalance

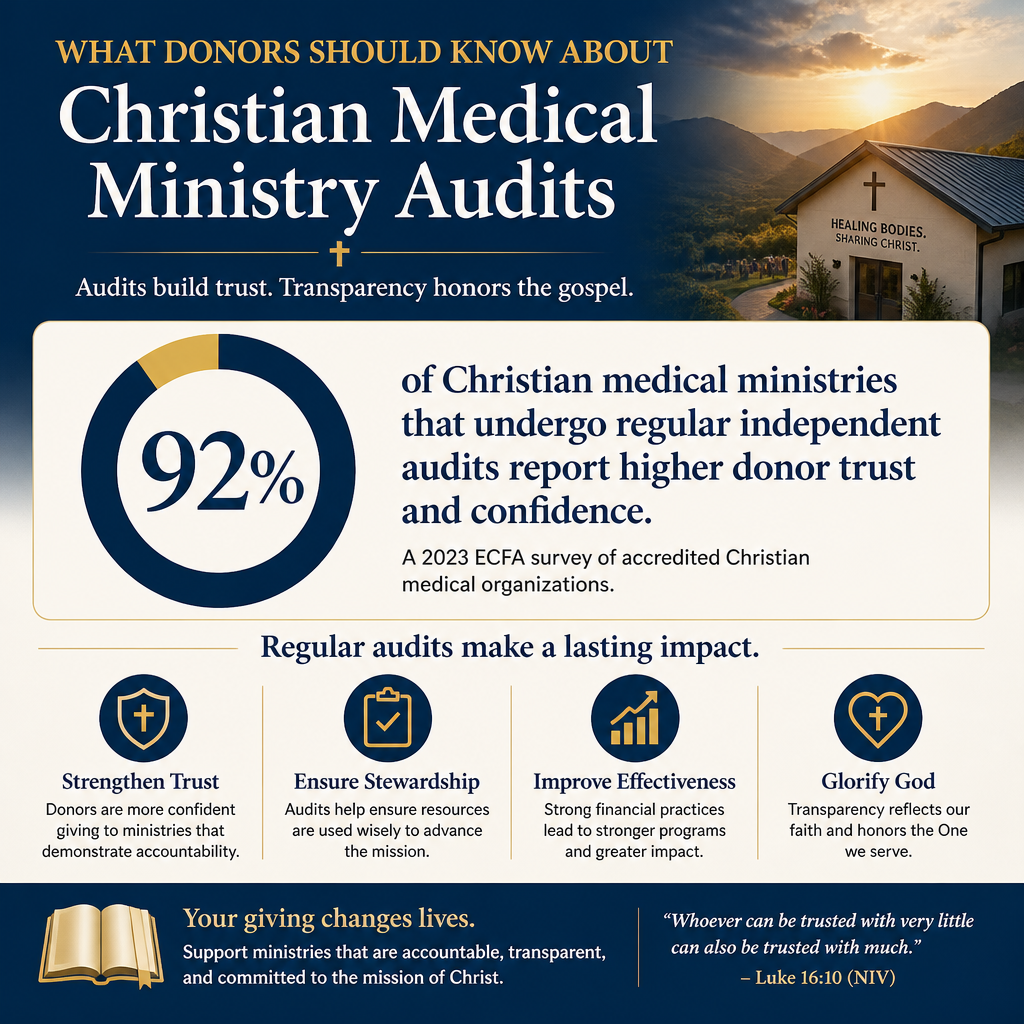

Most donors cannot visit field sites, examine procurement contracts, or evaluate whether a community health program is clinically sound. Ministries know that. The temptation is to substitute moving stories for verifiable evidence. Audits are one counterweight: they create a structured, external check on a ministry’s financial representations, which is often the only standardized documentation a donor can compare across organizations.

This is also where independent verification can serve donors. At Most Trusted, we evaluate ministries against The Most Trusted Standard, a 15-criteria framework that examines faith commitments, financial integrity, governance, and transparency. Audits are not the whole story, but they are one of the clearest signals that a ministry is willing to be measured.

3. What donors should ask for when a ministry says it is audited

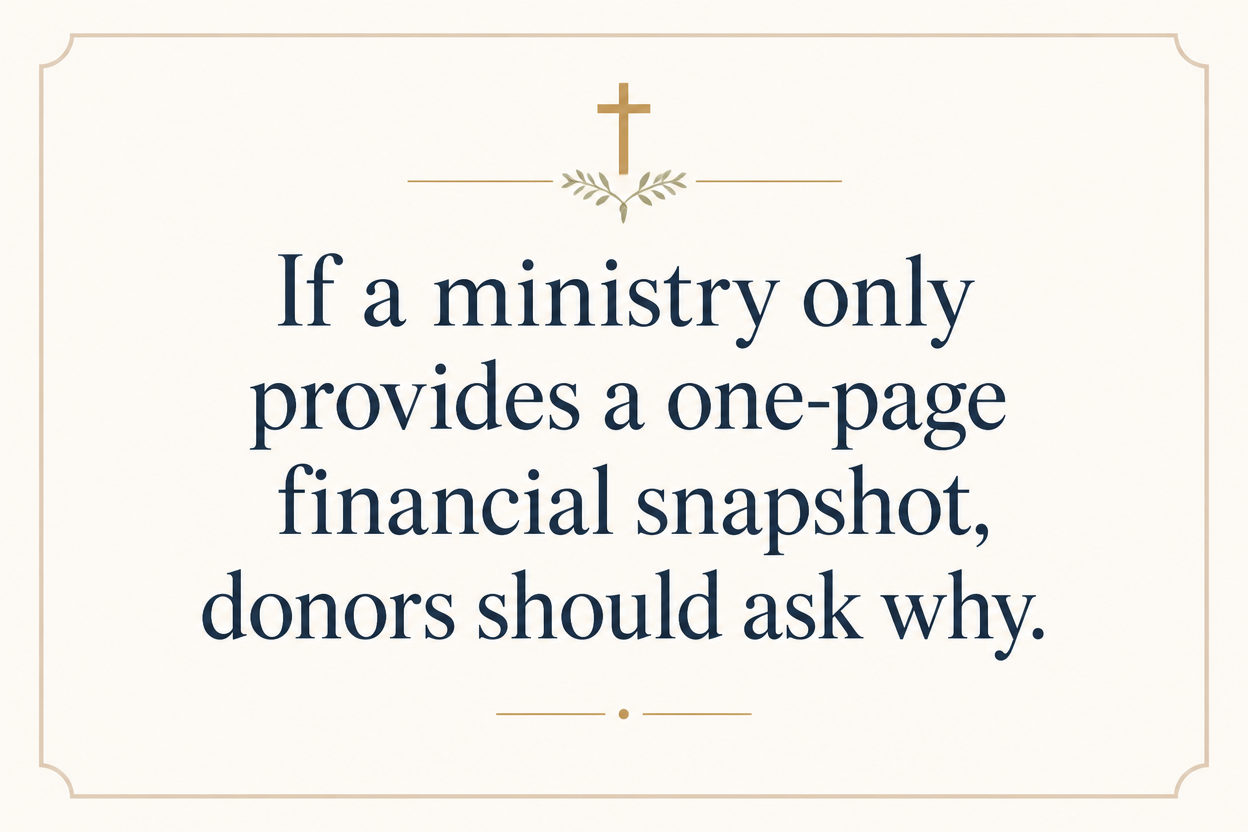

Request the actual audited financial statements

A ministry that has been audited should be able to provide the audited financial statements, including the auditor’s opinion letter, the statements themselves, and the notes. The notes matter; they explain key accounting judgments, related-party transactions, lease commitments, restricted funds, and uncertainties that a summary cannot capture.

If a ministry only provides a one-page financial snapshot, donors should ask why. For U.S. nonprofits, donors can often cross-check baseline information through the IRS Form 990, which the IRS requires for many tax-exempt organizations. The IRS explains nonprofit filing expectations and public disclosure at irs.gov/charities-non-profits.

Clarify scope, standards, and timeframe

Audits are tied to a fiscal year. A ministry may have been audited five years ago and not since. Or it may have a clean opinion but weak timeliness, releasing audited statements long after the year ends. Timeliness is not a cosmetic issue; delayed reporting can signal internal bottlenecks or governance weaknesses that donors should not ignore.

Donors can ask a small set of clarifying questions without drifting into suspicion. A prudent ministry will welcome clarity because it protects them from misunderstanding and builds trust.

- Which fiscal year was audited, and when were the audited statements released?

- Was the engagement an audit, a review, or a compilation, and what standards applied?

- What was the auditor’s opinion: unmodified, qualified, adverse, or disclaimer?

- Were there significant deficiencies or material weaknesses reported to governance?

- Were there major restatements or changes in accounting policy year over year?

Pay attention to governance’s relationship to the auditor

In well-governed nonprofits, the board or an audit committee oversees the audit relationship, not management alone. Donors rarely see the full behind-the-scenes governance process, but ministries can disclose basic practices: who approves the auditor selection, whether auditor rotation is considered, and whether the board reviews the results in detail.

This is one reason we encourage donors to view audits as part of a broader accountability ecosystem. A clean audit opinion alongside a weak board, opaque related-party disclosures, or repeated leadership conflicts does not provide the confidence donors are seeking.

4. Audit signals donors often misread

A clean opinion does not answer every donor question

Christian donors often want to know whether giving “directly helps patients” and whether “administration is kept low.” A financial audit does not certify that overhead is morally suspect or that low administration is inherently virtuous. The nonprofit field has increasingly resisted simplistic overhead ratios because they can punish investments in compliance, staff training, cybersecurity, safeguarding, and evaluation.

Prominent charity evaluators have explicitly warned against treating overhead as the primary measure of quality. Charity Navigator summarizes this concern and the broader debate around overhead in its educational materials at charitynavigator.org.

A ministry can be audit-ready and still be programmatically weak

Financial reporting can be strong while medical practice, partner oversight, or outcome measurement is thin. In medical ministry, donors should ask for evidence of clinical protocols, credential verification for volunteers, safeguarding training, and partner accountability, especially in cross-cultural contexts where power imbalances are pronounced.

Christians genuinely disagree about how much outcome measurement is appropriate for mercy ministries. Some fear that metrics can treat patients as numbers. Others argue that refusing measurement can hide negligence. The wiser approach is to expect proportionality: the more a ministry claims measurable impact, the more it should be prepared to show credible evidence, without flattening compassion into spreadsheets.

Absence of an audit is not always disqualifying, but it is informative

Smaller ministries may not be able to afford a full audit every year. That reality is not automatically a sign of irresponsibility. But donors should understand what replaces it: strong bookkeeping, independent board oversight, transparent reporting, and clear controls around cash handling and restricted funds. If none of those are present, the lack of an audit becomes less a budget issue and more a governance issue.

Where donors are making larger gifts, funding medical assets, or supporting international operations with complex supply chains, requiring an audit becomes more reasonable. Stewardship is not uniform; it scales with the size and risk profile of the giving.

5. How audits fit into a fuller picture of trust

Audits belong alongside faithfulness, transparency, and effectiveness

For Christian donors, trust is not merely technical. It includes fidelity to the gospel, integrity in leadership, and truthful communication. Audits help with one slice of that picture: whether financial statements can be relied upon. They do not test theology, pastoral posture, or whether stories are presented with dignity and consent.

That is why donors benefit from looking at a ministry through more than one lens. Most Trusted exists to help donors do that work carefully. Under The Most Trusted Standard, we look for coherent faith commitments, credible governance, disciplined financial practices, and transparent reporting that respects donors as moral agents, not merely as revenue sources.

Use audits to ask better questions, not to outsource discernment

Many donors want a single document that settles the question: “Is this ministry safe to support?” Audits are valuable, but they do not remove the need for discernment. They should prompt more precise questions about related-party transactions, restricted fund handling, concentration of authority, and whether financial reporting aligns with how the ministry describes its work publicly.

For donors focused on Christian medical work, it is also wise to situate the audit conversation within the broader landscape of accountability in Christian Medical Ministries. Different models—clinics, mobile teams, hospital partnerships, medical ships, and community health programs—have different risk profiles that change what “good accountability” looks like.

Donors concerned about receipting, substantiation, and compliance expectations should also take the time to understand Tax Receipts and Compliance for Christian Medical Ministry Giving. An audit can support confidence, but it does not replace clear gift documentation, correct legal structuring, and honest communication about deductibility.

FAQs for What donors should know about Christian medical ministry audits

Does an audit prove that a Christian medical ministry is using donations exactly as promised?

No. An independent financial statement audit provides reasonable assurance that the financial statements are fairly presented in all material respects. It does not guarantee that every restricted gift was tracked perfectly, that every program claim is accurate, or that every operational risk has been controlled. Donors should read the notes, ask how restricted funds are handled, and look for additional transparency about program delivery and partner oversight.

Should we refuse to give if a medical ministry does not have an audit?

Not automatically. The right expectation depends on size, complexity, and risk. For smaller ministries, a full audit may be financially burdensome, but the absence of an audit should be offset by other concrete practices: transparent financial reporting, independent board oversight, documented internal controls, and clear policies for handling cash, medicines, and restricted gifts. For larger gifts or higher-risk operations, requiring audited statements is a prudent expression of stewardship.

Stewardship that honors the sick and respects the truth

Audits are not a substitute for Christian discernment, but they are a meaningful form of accountability in a field where donors carry real responsibility. When ministries welcome independent scrutiny, report clearly, and govern themselves with integrity, donors can give with greater freedom—confident that mercy is being carried with truthfulness, and that compassion is not being purchased at the expense of credibility.