Tax receipts and stewardship for orphan care donors are not administrative details; they are part of Christian obedience. The same Scripture that commands care for the fatherless also insists on honest weights and measures, and the church has long understood financial integrity as a moral matter, not merely a compliance matter. When donors give to orphan care, they are not purchasing outcomes. They are entrusting resources to an organization that must handle those resources with transparency, restraint, and reverence.

Orphan care also carries distinctive risks that make paperwork and governance more, not less, important. The movement has had to reckon with the harm that institutionalization can do to children, the perverse incentives created when beds must be filled to satisfy funding, and the temptation to tell stories that move money but flatten truth. Stewardship begins before a gift is made: we honor God when we ask hard questions about how a ministry accounts for gifts, communicates need, and protects the children and families it serves.

Tax receipts are a stewardship signal, not a spiritual scorecard

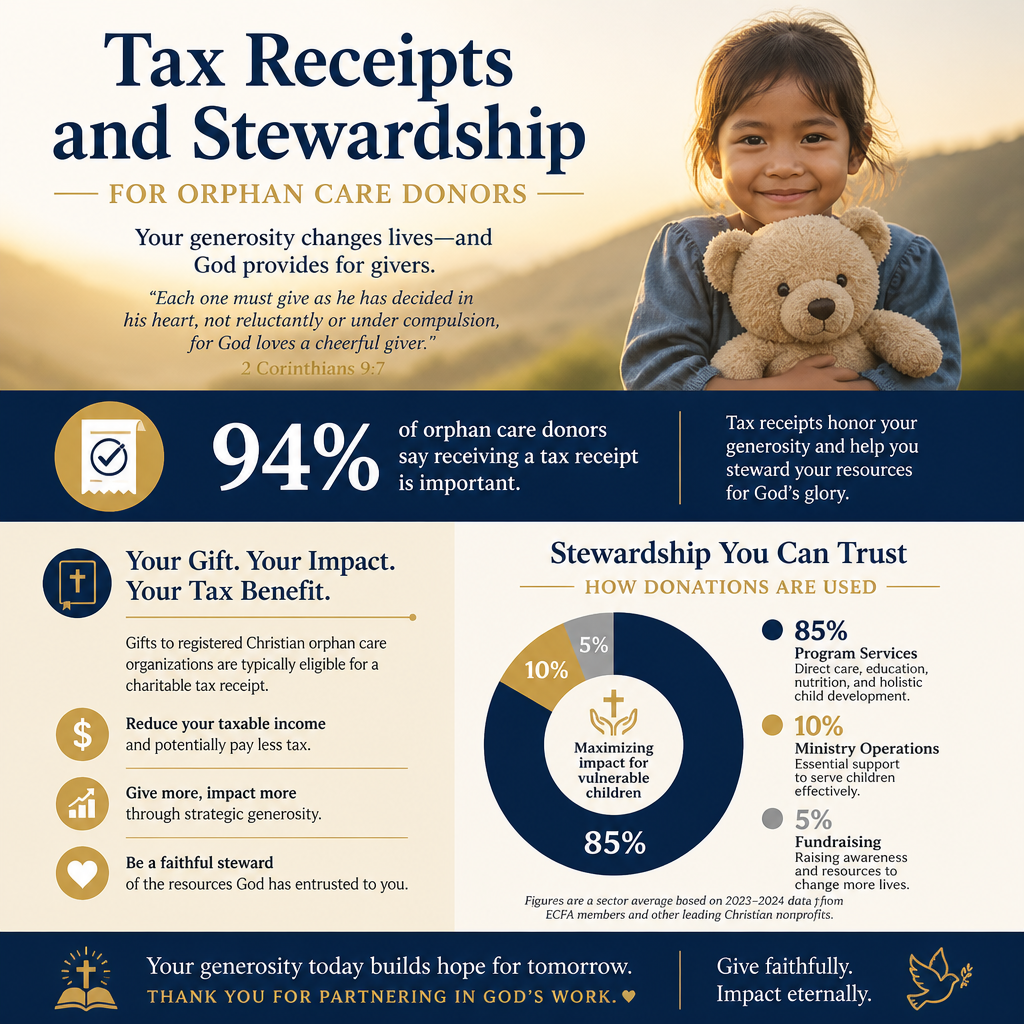

A tax receipt is not the reason Christians give, but it is often the first verifiable document a donor receives. For many donors, it becomes the practical test of whether a ministry’s back office is ordered toward integrity or toward improvisation. That difference matters because orphan care ministries routinely manage restricted funds, sponsor support, international transfers, and personal data. A ministry that treats receipting lightly will usually treat other controls lightly as well.

What a proper receipt should include

In the United States, the IRS expects donors to have a contemporaneous written acknowledgment for contributions of $250 or more, and that acknowledgment must include specific elements (such as whether goods or services were provided and a good-faith estimate of their value). The standard is not ambiguous, and the consequences land on the donor at filing time. The IRS outlines these requirements in its guidance for charitable contributions at IRS.gov.

Receipts also signal whether the ministry understands the difference between an internal record and a donor-facing acknowledgment. Serious ministries generally issue receipts promptly, correct errors without defensiveness, and retain records in ways that match the nature of their work. Orphan care often involves recurring support relationships, and those relationships require consistent statements that donors can reconcile against their own records.

When a receipt does not make a gift deductible

Tax deductibility is not a synonym for generosity, and a receipt is not a guarantee. Some gifts are not deductible even when a ministry is acting in good faith, including certain quid pro quo arrangements or payments that function as tuition or personal benefit. Non-cash gifts carry additional substantiation rules and, in some cases, appraisal requirements. IRS Publication 526 remains the baseline reference point for what is deductible and what documentation is required at IRS.gov.

For orphan care donors, the most common friction point is not intent but classification: sponsorship relationships can blur lines in donors’ minds. If a ministry is clear in its receipting language and program description, it reduces the risk that donors will treat a gift as a personal transaction rather than a charitable contribution made to the organization’s discretion.

Restricted gifts are powerful tools, and they can damage a ministry when misused

Christian donors often restrict gifts out of earnest desire: a child’s sponsorship, a transition home, a family preservation initiative, or a specific country program. Restrictions can protect mission focus and prevent drift. They can also create a brittle financial structure that forces leaders to chase designated dollars while core operations quietly starve. Mature stewardship acknowledges that both realities are true.

How restrictions should be defined and honored

A restriction is a donor-imposed limitation on how a gift may be used. In practice, clarity is everything. A restriction that is too narrow can trap funds in a program that cannot responsibly absorb them; a restriction that is too vague becomes functionally meaningless. Strong ministries document restrictions in writing, train staff to code gifts correctly, and report on restricted fund balances with the same seriousness they apply to child safeguarding policies.

Accounting standards require nonprofits to classify net assets with donor restrictions separately and to disclose relevant information in financial statements. While many donors will never read a full audit, the presence of audited statements and coherent notes is one of the clearest external indicators that restrictions are being tracked and honored. The Financial Accounting Standards Board provides authoritative standards at fasb.org.

Why “designated for a child” language requires careful handling

Sponsorship is often described as support “for a child,” and in many models it is administered as part of a broader program that benefits multiple children and families. Ethical practice requires that ministries explain this plainly: the donor is giving to the organization to carry out its mission; the donor is not assuming parental control or purchasing a defined set of services. When donors believe they are funding an individual child in a tightly traceable way, disappointment is predictable, and trust erodes when realities are disclosed later.

The harder question is how a ministry behaves when a sponsored child leaves a program, reunifies, or relocates. Mature orphan care increasingly prioritizes family-based care and reintegration when safe and appropriate. Restrictions that implicitly reward institutionalization can unintentionally resist that progress. Donors who care about the fatherless should want ministries to do what is best for the child, even when it changes the story attached to a monthly gift.

When a ministry cannot follow a restriction

Restrictions sometimes become impossible to honor: a government closes a program, a partner relationship ends, or a safeguarding concern requires abrupt changes. At that moment, integrity is tested. The ministry must either obtain donor consent to redirect funds or return them, depending on the circumstances and the governing documents. Quietly repurposing restricted money may solve a short-term problem, but it damages the moral foundation of the work.

Across our verification work at Most Trusted, the ministries that meet The Most Trusted Standard tend to treat restrictions as fiduciary commitments rather than as marketing promises. They also communicate constraints early, before a donor gives, because informed consent is part of honoring a donor’s conscience.

Donor information is a stewardship responsibility, not a fundraising asset

Orphan care ministries often ask for donor information that feels intrusive: legal names, addresses, employer details for matching gifts, and in some cases identifying information connected to international wire requirements. Donors may also share prayer requests, family updates, and notes intended to be passed to children or caregivers. That collection creates an ethical duty: the ministry becomes a custodian of sensitive information.

Why ministries request identifying details

Some data requests are simply necessary. A receipt must connect to a donor identity for tax reporting. Matching gifts often require employer verification. Payment processors require certain fields to reduce fraud. Larger ministries may also need to comply with anti-money laundering practices or banking requirements when funds move across borders. Donors should not assume malice when a form requests more than an email address, but they should expect a clear explanation and a restrained approach.

Where donors should be firm is on unnecessary collection and unclear retention. A ministry should be able to describe what it collects, why it collects it, how long it retains it, and how it secures it. In the orphan care context, this concern extends beyond donor privacy to child protection: communications and images involving minors demand heightened caution and controlled access.

Transparency about fundraising practices

Sophisticated donors know that fundraising and mission are not separable; the question is whether fundraising practices respect truth and dignity. Ministries should be able to state whether they rent or sell donor lists, how they handle opt-outs, and whether they use third-party marketing platforms that share data. When answers are evasive, prudence is warranted.

Responsible stewardship also requires that donors refuse the temptation to treat children’s stories as consumable content. Christians genuinely disagree about the boundaries of storytelling in ministry communications, but there is broad agreement that children must not be exposed to harm in the name of raising funds. A ministry’s privacy posture is therefore not peripheral; it is part of its safeguarding culture.

Complex gifts require humility, documentation, and aligned expectations

Many orphan care donors are now considering gifts beyond a credit card donation: appreciated stock, donor-advised funds, qualified charitable distributions, and estate gifts. These can be wise and generous, but they raise the stakes. The ministry must process the gift accurately, issue appropriate acknowledgments, and avoid providing tax advice it is not qualified to give. Donors must also avoid using complexity as a way to distance themselves from accountability.

Gifts of stock and other non-cash assets

Giving appreciated securities can increase impact while reducing capital gains exposure, but the documentation differs from cash giving. Donors typically need a receipt acknowledging the gift without assigning a value, since valuation is generally the donor’s responsibility. If the ministry’s instructions are confusing or its brokerage process is inconsistent, donors can face delays and errors that are difficult to unwind later. The IRS guidance for non-cash contributions and substantiation is accessible through IRS.gov.

For orphan care in particular, donors should ask how the ministry treats non-cash gifts operationally. Some organizations liquidate immediately; others retain certain assets under board-approved policies. Either approach can be responsible if governed and disclosed, but neither should be improvised.

Planned giving and the moral clarity of bequests

Planned giving often reflects a donor’s settled convictions: that the care of vulnerable children and families is not a seasonal concern but a lifetime commitment. Bequests, beneficiary designations, and charitable trusts can also introduce misaligned expectations if a donor assumes the gift will fund a very specific program indefinitely. Ministries change, contexts change, and needs change. The most durable planned gifts are those restricted to a mission field broadly enough to remain faithful without becoming unworkable.

Donors should also consider governance continuity. A bequest is an act of long-term trust in a board’s future decisions, not only a vote of confidence in current leadership. That is one reason verification matters. Most Trusted evaluates ministries against The Most Trusted Standard, examining faith commitments, financial integrity, governance practices, and transparency so donors can make longer-horizon decisions with fewer blind spots.

What donors should reasonably expect from financial reporting

Not every faithful orphan care ministry will be large enough to commission a full independent audit, and donors should not confuse size with virtue. Still, the baseline expectations are clear: consistent receipting, understandable annual reporting, accessible leadership and board information, and a willingness to answer informed questions without irritation. When a ministry resists ordinary accountability practices, donors should interpret that resistance as a meaningful data point.

For donors who want to place their giving inside a broader view of safeguards, family-based care models, and long-term outcomes, our work on Orphan Care Ministries addresses the wider context in which financial stewardship sits. The same commitments that protect a donor’s tax documentation also protect children from being turned into fundraising instruments.

Stewardship that honors God protects both children and trust

Christian donors do not give to satisfy the IRS, but neither do we glorify God by treating financial truth casually. Tax receipts, restricted gift practices, donor privacy, and complex gift processing are all tests of whether a ministry is ordered toward integrity. In orphan care, where emotions run high and stories carry real power, those tests become safeguards.

The aim is not suspicion; it is disciplined love. When donors insist on clear receipting and principled stewardship, we strengthen the conditions under which orphan care can mature toward what children most need: stable families, honest institutions, and mercy governed by truth.