Evaluating financial transparency in Bible translation ministries is not a secondary concern for Christian donors; it is a stewardship question with moral weight. Scripture treats money as a revealer of the heart, and the church has learned through centuries that spiritual language can be used to conceal weak controls, conflicted decision-making, or avoidable waste.

Financial transparency does not guarantee faithfulness, and a ministry can publish glossy reports while obscuring material risks. Yet a ministry that refuses ordinary accountability places an avoidable burden on donors’ consciences. “It is required of stewards that they be found faithful” (1 Corinthians 4:2) is not only a personal exhortation; it is also a governance principle that should be visible in public records, board practice, and accessible reporting.

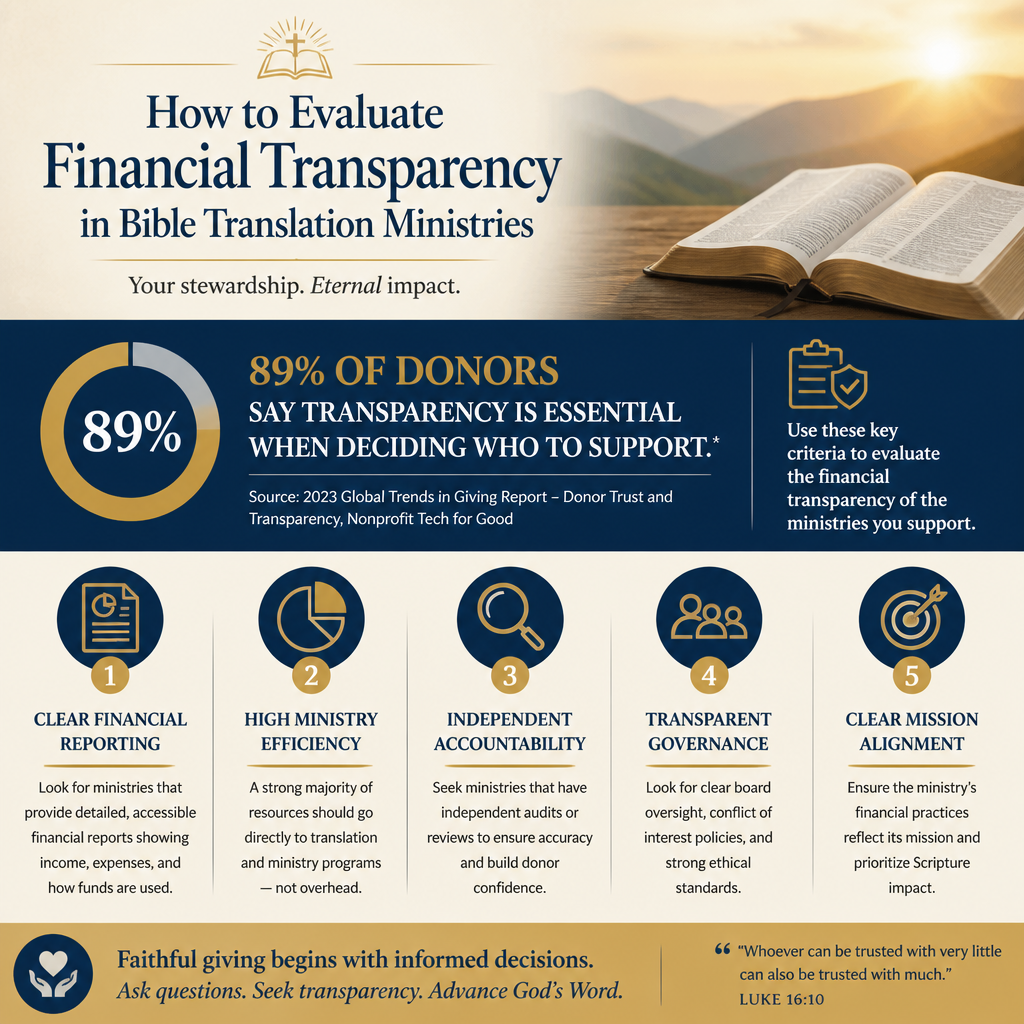

Start with what transparency can and cannot prove

Christian donors often want a simple indicator: a percentage, a rating, a single document. Financial transparency rarely works that way, especially in Bible translation where security concerns, cross-border remittance, and multi-year project timelines complicate public reporting. A mature evaluation begins by distinguishing between secrecy that protects people and secrecy that protects an institution.

Security concerns are real but they are not a blank check

Some translation work occurs in places where public disclosure can put local partners at risk. Donors should expect a ministry to explain, in plain terms, what it withholds and why, and to offer alternative forms of verification: audited financials shared privately, aggregated reporting by region, or third-party oversight. “Walk as children of light” (Ephesians 5:8) does not require reckless disclosure, but it does require a posture of truthfulness rather than defensiveness.

Transparency is a pattern across documents, not a single artifact

Many donors begin with the IRS Form 990 because it is standardized. That instinct is sound: the Form 990 is one of the few comparable windows into governance, related-party transactions, executive compensation, and revenue mix. The IRS itself frames the Form 990 as a public disclosure tool for tax-exempt organizations, with legal obligations around accuracy and public availability IRS.

Verify the basics first: audited financials, accessible filings, and clear policies

Before analyzing nuanced efficiency questions, donors should confirm whether the ministry meets baseline transparency norms that responsible boards treat as non-negotiable. Where these basics are absent, deeper claims about impact cannot be responsibly weighed.

Audits matter because internal sincerity is not an internal control

An independent financial statement audit is not a spiritual badge; it is a disciplined process that tests whether an organization’s financial statements are fairly presented under accepted standards. Many smaller ministries cannot justify an audit every year, but larger Bible translation ministries handling significant restricted gifts typically can, and should. When an audit is available, donors should look for the audit opinion, whether the auditor reported material weaknesses, and whether the ministry explains how it addressed findings.

Policies reveal whether transparency is embedded or improvised

Responsible ministries publish, at minimum, a conflict of interest policy, a whistleblower policy, and a document retention policy. These are not bureaucratic formalities; they are safeguards for truth-telling and for protecting staff who raise concerns. Donors should also look for a clear gift acceptance policy, especially when ministries receive complex non-cash gifts or donor-advised fund grants.

- Audited financial statements available on the website or upon request

- Current IRS filings and a consistent practice of public disclosure

- Conflict of interest policy and board disclosure practice

- Whistleblower reporting channel that does not route back to the accused leader

- Clear restrictions language for designated gifts and how they are honored

Across our verification work at Most Trusted, the ministries that meet The Most Trusted Standard tend to treat these items as ordinary stewardship, not as donor appeasement. That distinction affects how candidly leaders answer questions, how boards document decisions, and how quickly corrections are made when errors occur.

Read the money with translation realities in mind

Bible translation is not a single expense line called “translation.” It is a portfolio of activities: linguistic research, community testing, Scripture engagement, training local translators, literacy work, distribution, and often technology. Donors should read budgets and reports in light of that reality rather than forcing ministries into misleading categories.

Beware simplistic overhead arguments

Christian donors have been trained to treat a low “overhead ratio” as a moral virtue. The nonprofit sector has pushed back on that assumption for good reason. Charity Navigator, Candid, and the BBB Wise Giving Alliance jointly warned against the “overhead myth,” arguing that underinvesting in administration and fundraising can undermine effectiveness and accountability Charity Navigator. For Bible translation ministries, underinvestment in finance teams, security protocols, and partner due diligence is not frugality; it can be a risk to people and to Scripture projects.

Restricted gifts require visible discipline

Translation projects are often funded through restricted gifts: “for Language X,” “for the New Testament,” “for training local translators.” A transparent ministry explains how it tracks restricted funds, what happens when a project is overfunded or delayed, and how it communicates changes. Donors should watch for vague language such as “funds may be used where needed most” attached to heavily marketed designations. Sometimes that flexibility is necessary; it becomes problematic when it is unclear, undisclosed, or inconsistent with donor intent.

What this means in practice is that donors should ask for a simple reconciliation: how much was raised for a category and how much was spent, over a multi-year horizon. Mature ministries can provide this without treating the question as distrust.

Follow governance signals that predict financial honesty

Financial transparency is rarely separable from governance quality. Weak boards approve weak disclosures. Strong boards insist on clarity because they understand that mission faithfulness and financial integrity are intertwined.

Board independence and related-party transactions

Donors should review whether a board is meaningfully independent of the founder or CEO, whether it includes financial expertise, and whether it documents decisions. The Form 990 can reveal whether officers or key employees have family relationships with each other, and it prompts disclosure about business transactions with interested persons. These are not automatically disqualifying facts, but they raise the burden of proof for oversight and disclosure.

Executive compensation should be explainable without defensiveness

Compensation is a perennial flashpoint: some donors assume any high salary is morally suspect, while others ignore the issue entirely. Scripture speaks strongly to greed and self-dealing, and it also recognizes that “the laborer deserves his wages” (1 Timothy 5:18). The question is whether compensation is set through a documented, independent process using comparable data, and whether the ministry is candid about that process. A transparent organization can describe how pay is determined and how it aligns with the organization’s size and complexity.

For donors seeking a broader framework for prudent discernment across ministries, we encourage engagement with How to Give Wisely to Bible Translation Ministries, where these governance signals are weighed alongside theological and programmatic considerations.

Ask for effectiveness reporting that matches financial claims

Financial transparency is ultimately in service of mission truthfulness. Bible translation ministries should be able to connect money to outputs and outcomes in ways that neither trivialize spiritual fruit nor hide behind it.

Demand clarity on what is counted and what is implied

Translation ministries often report progress in ways that can confuse donors: “languages started,” “translation programs supported,” “people reached,” “Scripture portions distributed.” Some of these are meaningful; some can be inflated if definitions are loose. A responsible report defines terms, distinguishes between direct work and funded partners, and avoids implying that distribution equals comprehension or discipleship.

Time horizons are long and that should be disclosed, not marketed away

Translation is slow, iterative work. Donors should be wary of reporting that promises speed without acknowledging community checking, consultant review, or Scripture engagement work that enables use. Transparent ministries explain delays, political disruptions, staffing changes, and quality-control decisions. They also show how they evaluate partnerships, especially when funds are passed through to local organizations.

Across our work applying The Most Trusted Standard, we have found that the healthiest ministries publish enough detail to invite meaningful questions: what was accomplished this year, what did it cost, what remains, and what would cause the plan to change. That posture reflects confidence in the light rather than skill in persuasion.

For donors wanting a wider view of the field, including how different Bible translation models structure partnerships and accountability, see Bible Translation Ministries.

FAQs for How to evaluate financial transparency in Bible translation ministries

Should a Bible translation ministry publish audited financials on its website?

For ministries of substantial size, publishing audited financial statements is a strong indicator of transparency and board seriousness. Some organizations working in high-risk contexts may choose to share audits upon request rather than posting them publicly, but they should still provide independent verification and a credible explanation of what is withheld and why. A refusal to provide audited statements in any form, when the ministry has the scale to obtain an audit, is a meaningful warning sign.

Is a low overhead ratio a reliable way to judge financial integrity?

No. Overhead ratios can be manipulated and can punish necessary investments in finance systems, safeguarding, partner due diligence, and staff development. Sector leaders have cautioned donors against treating overhead as a proxy for impact, including the joint statement from Charity Navigator, Candid, and the BBB Wise Giving Alliance on the “overhead myth” Charity Navigator. The better question is whether spending decisions are explained, governed well, and connected to credible progress and outcomes.

A faithful donor posture is neither suspicion nor naivete

Christian donors are not called to cynicism, but we are called to wisdom. Financial transparency in Bible translation ministries should look like truthful disclosure, disciplined governance, and reporting that can withstand ordinary scrutiny without spiritualizing away legitimate questions. Where a ministry welcomes that scrutiny, donors can give with greater freedom, trusting that integrity and mission are being pursued together.