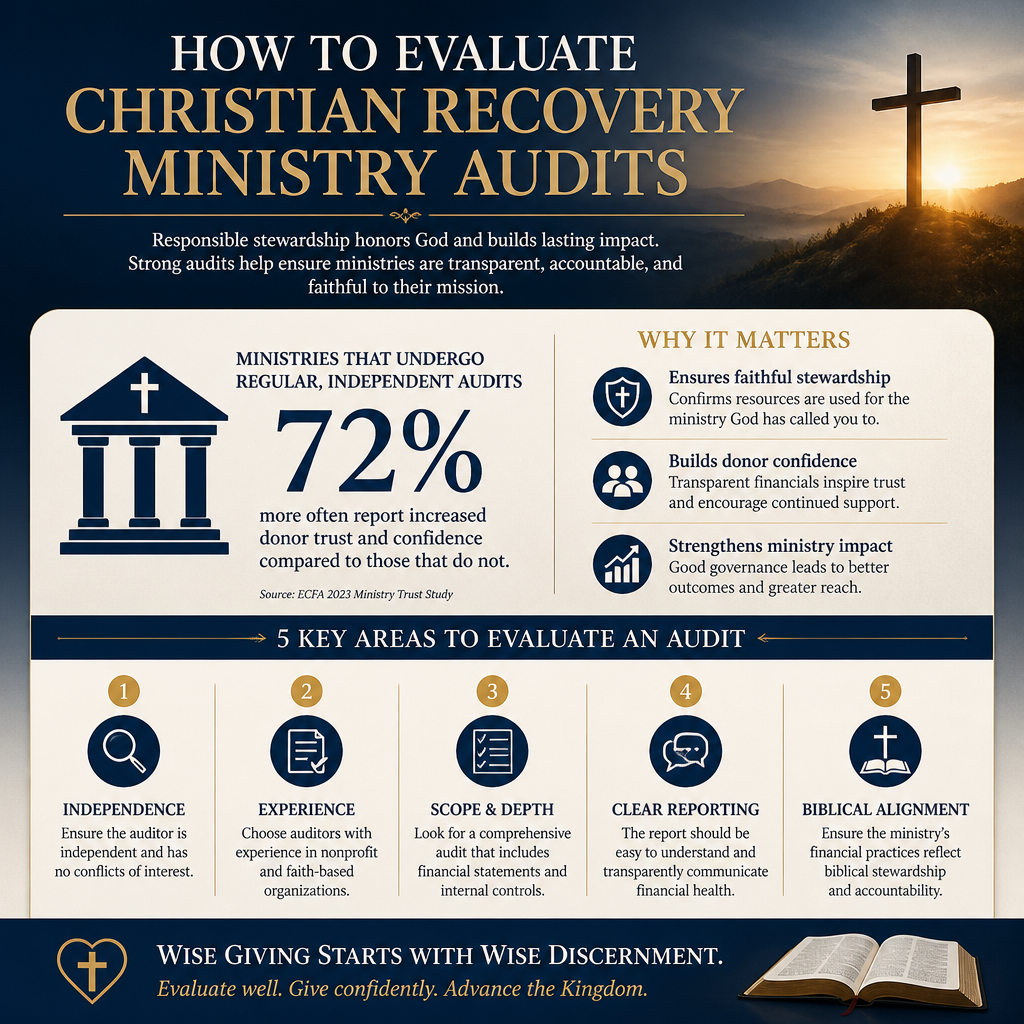

Evaluating Christian recovery ministry audits is one of the most practical ways donors can honor both compassion and truth. Addiction recovery work carries real spiritual stakes, deep human suffering, and high operational complexity; audits are not a luxury but a basic discipline of stewardship and credibility.

Many donors want assurance that a ministry is not only sincere, but also sound: faithful in doctrine, careful with money, accountable in leadership, and honest about outcomes. Audits can help establish that assurance, but only when donors understand what an audit can and cannot tell them, and when ministries are willing to be examined in the light.

Start with clarity about what an audit is and is not

Financial statement audits answer a narrow question

A financial statement audit is an independent CPA firm’s opinion on whether an organization’s financial statements are presented fairly, in all material respects, in accordance with an accounting framework such as U.S. GAAP. It is not a certification that a ministry is well-run, doctrinally faithful, or effective in discipleship. It does not prove that every dollar was spent wisely; it provides reasonable assurance that the reported numbers are not materially misstated.

That distinction matters in recovery ministry because donors often want an “impact audit” when what exists is a financial audit. Both are valuable, but they are not interchangeable. A ministry may have clean financial statements and still have weak program controls, unhealthy leadership dynamics, or unclear treatment practices.

Other reviews matter and donors often confuse them

Some ministries use a compilation or review instead of an audit. Those engagements are less rigorous than an audit and are not designed to provide the same level of assurance. Similarly, an annual Form 990 is not an audit; it is a tax filing. Donors should read these documents as different tools, each with its own limitations.

The goal is not to demand a single perfect document. The goal is to see whether a ministry welcomes scrutiny appropriate to its size and risk profile, and whether its leadership treats accountability as part of Christian obedience rather than an external imposition.

Read the auditor’s report like a steward, not a spectator

Opinion language signals the starting point

When donors receive audited statements, the first page to read is the independent auditor’s report. An “unmodified” opinion (sometimes called a “clean” opinion) is generally what donors expect for stable organizations with ordinary financial complexity. A “qualified,” “adverse,” or “disclaimer” opinion does not automatically mean fraud, but it does mean donors should slow down and ask direct questions about why the auditor could not provide standard assurance.

Christian donors are often reluctant to press for explanations because they do not want to appear cynical. Scripture does not commend naïveté. “Whoever walks in integrity walks securely, but he who makes his ways crooked will be found out” (Proverbs 10:9). Integrity welcomes clarity.

Material weaknesses and significant deficiencies are not technical trivia

Audits frequently include communication about internal control issues. A “material weakness” indicates a reasonable possibility that a material misstatement of the financial statements will not be prevented or detected in time. A “significant deficiency” is less severe but still meaningful. In recovery ministry contexts, weak controls can create conditions where restricted gifts are misapplied, client-related expenses are miscoded, or leadership overrides process under pressure.

Donors should not panic at every control issue; smaller organizations often mature over time. But donors should insist on a credible remediation plan, a timeline, and evidence that the board is engaged. An audit that identifies a problem is doing its job. A board that ignores the problem is not.

Recovery ministries have unique risk areas donors should test

Client care and safety require more than financial compliance

Many recovery ministries operate residential programs, counseling, peer support, or reentry services. These environments raise serious safeguarding questions: staff screening, incident reporting, medication management (when applicable), boundaries, and supervision. A standard financial audit does not verify these controls. Donors should therefore ask whether the ministry undergoes additional oversight appropriate to the services offered—clinical supervision structures, external licensing where required, and documented safeguarding policies.

This is not a secular distraction from the gospel. Christian recovery work is a form of neighbor-love that must be ordered by holiness and protection of the vulnerable. When ministries claim to be spiritually restorative, they must also be operationally trustworthy.

Restricted giving and designated funds are common pressure points

Recovery ministries frequently receive designated gifts for scholarships, housing assistance, program expansion, or capital projects. These funds increase complexity. Donors should look for evidence that the ministry tracks restricted gifts accurately and reports on them transparently. The audit can help confirm whether restricted net assets are stated properly, but donors can also ask for narrative reporting that connects restricted funds to actual expenditures and outcomes.

Across our verification work at Most Trusted, ministries that meet The Most Trusted Standard tend to treat donor restrictions as a trust to be honored, not a flexibility to be negotiated. That posture usually shows up not only in the numbers, but in the ministry’s written communications and board oversight.

Effectiveness and spiritual fruit require disciplined transparency

Outcomes measurement in recovery is contested but not optional

Christian donors rightly care about spiritual transformation, not merely behavior modification. At the same time, recovery ministries should be able to provide credible, bounded claims about what they do and what participants experience. The field has had to reckon with how difficult it is to measure sustained sobriety, stable housing, employment, family reconciliation, and church reintegration over time. There are methodological challenges: attrition, self-report bias, and the ethics of follow-up with people in fragile situations.

Those challenges are not a reason to abandon measurement. They are a reason to measure with humility, clarity, and restraint. Donors should be wary of ministries that advertise extraordinary success rates without defining terms, time horizons, or data sources. Donors should also be wary of ministries that refuse to track anything measurable on the grounds that “only God can measure fruit.” God measures the heart; donors still must steward resources responsibly.

Financial efficiency is not the same as effectiveness

Some donors treat overhead ratios as the primary indicator of trustworthiness. That approach has been widely criticized by nonprofit evaluators because it can incentivize underinvestment in governance, finance, and evaluation. A widely cited articulation of this concern is the “Overhead Myth” statement supported by leading charity evaluation and oversight organizations, including Charity Navigator and BBB Wise Giving Alliance Charity Navigator. Donors should ask not “How low is overhead?” but “Are administrative and fundraising costs appropriate, explained, and governed?”

In practice, audits help donors see whether reporting is consistent and whether financial statements reflect a disciplined organization. But donors still need a second lens: whether the ministry tells the truth about what it can reasonably claim, and whether it corrects course when programs do not produce the results hoped for.

Use audits as one component of a broader verification posture

Board governance is where accountability either holds or collapses

In Christian ministries, donors often focus on the founder’s charisma or the program’s emotional resonance. Audits, however, point donors toward governance: who sets policy, who approves budgets, who reviews executive compensation, and who addresses conflicts of interest. A ministry can have passionate staff and still drift into patterns of unaccountable decision-making that eventually harm participants and donors alike.

Donors should ask whether the board meets regularly, maintains minutes, has independent members, and takes responsibility for financial oversight. The audit committee function may be formal or informal depending on size, but someone other than staff should own the relationship with the auditors. When the same person both spends the money and controls the reporting, the conditions for misuse are present even if misuse has not occurred.

What we recommend donors request from ministries

For most recovery ministries, a donor’s goal should be simple: confirm that the ministry is transparent, governed, and candid about both results and limitations. When evaluating audited materials and related disclosures, we recommend requesting:

- The most recent audited financial statements and the management letter if available

- A clear explanation of any auditor findings and a written remediation plan

- Board policies on conflicts of interest, compensation setting, and whistleblower protection

- A program description that distinguishes services offered from outcomes claimed

- A summary of outcome tracking methods, definitions, and time horizons

Donors who want to go deeper into the broader landscape of vetted considerations in this field can review Christian Addiction Recovery Ministries as a reference point for common models, risks, and verification questions.

Most Trusted exists to reduce the burden on donors who do not have the time or specialized expertise to perform this diligence alone. Our evaluations apply The Most Trusted Standard across faith commitments, financial integrity, governance and leadership, and transparency and effectiveness, because a ministry’s trustworthiness is rarely confined to a single document.

FAQs for How to evaluate Christian recovery ministry audits

Should every Christian recovery ministry have a full financial audit?

Not always. The appropriate level of assurance depends on size, complexity, regulatory requirements, and the risk profile of the programs offered. A small, simple ministry may begin with reviewed statements and mature toward a full audit as revenue and complexity grow. What donors should consistently expect is proportional transparency: clear financial reporting, board oversight, and a willingness to answer direct questions without evasion.

What is the most concerning audit red flag for a recovery ministry?

A nonstandard auditor opinion or repeated, unresolved internal control findings should trigger careful follow-up, especially when paired with weak governance signals such as a founder-controlled board or lack of documented policies. The issue is not perfection; it is whether leadership demonstrates repentance-shaped accountability—naming problems truthfully, correcting them promptly, and submitting to oversight appropriate to the trust being received.

Recovering trust requires more than good intentions

Christian recovery ministry often serves people who have been betrayed by institutions and wounded by sin, including their own. Donors should not add to that harm by funding work that cannot withstand scrutiny. Audits are one crucial instrument of accountability, but they function best when donors read them carefully, ask disciplined questions, and expect governance that treats the ministry’s resources and participants as sacred trusts.

For donors who want to evaluate how ministries measure outcomes and communicate effectiveness with integrity, How Christian Addiction Recovery Ministries Measure Impact provides additional context for what responsible transparency can look like in a field where simplistic claims rarely serve the truth.