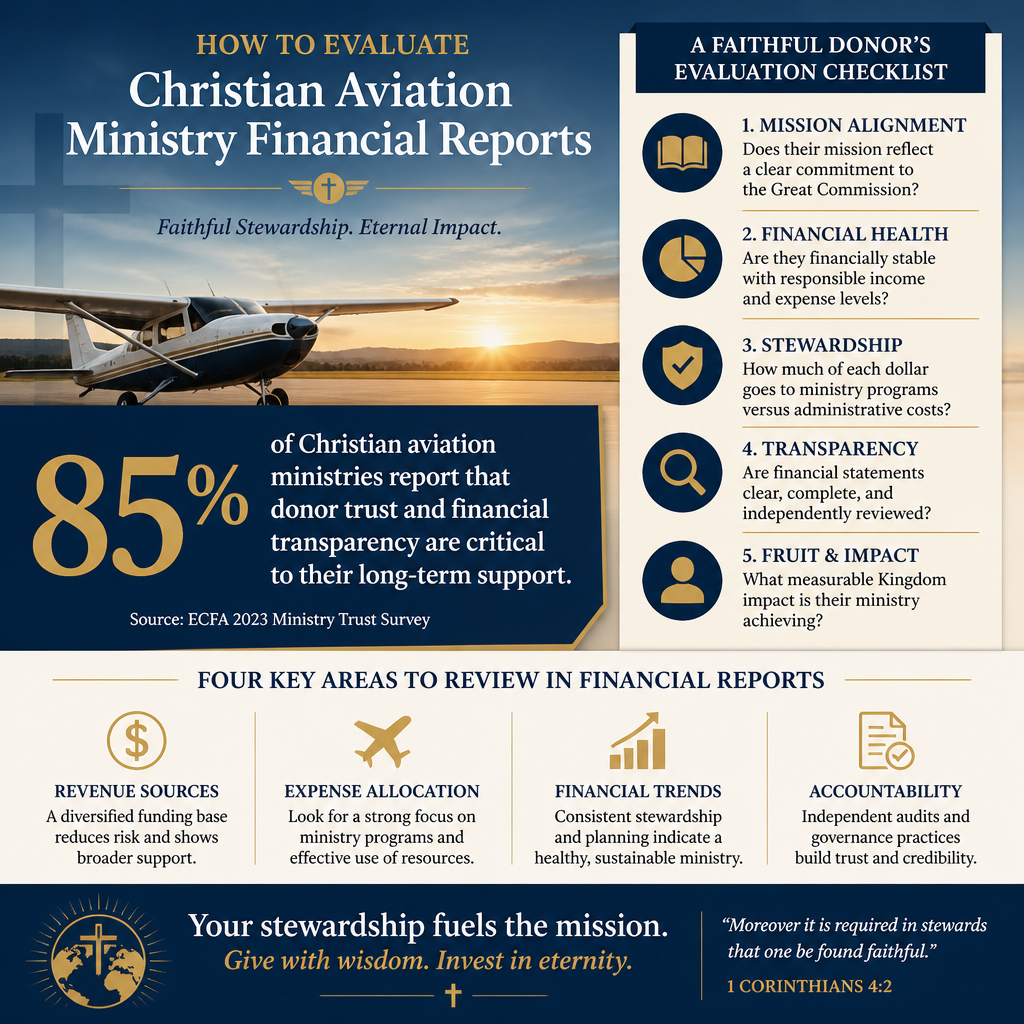

Knowing how to evaluate Christian aviation ministry financial reports is not a secondary concern for serious donors. Aviation amplifies both impact and risk: a single aircraft can open access to isolated communities, and a single weak control can expose donors, staff, and beneficiaries to preventable harm.

Scripture treats money as a spiritual matter before it is an administrative one. Jesus’ repeated teaching on wealth and stewardship is not mainly about techniques; it is about faithfulness, honesty, and the fear of God. For donors, a ministry’s financial reporting is one of the few public windows into whether leadership governs with that kind of reverent accountability.

Start with what the financials can and cannot prove

Financial reports are evidence, not the whole story

A ministry’s Form 990, audited financial statements, and annual report can show whether numbers reconcile, whether the organization follows accounting standards, and whether there are signs of instability or self-dealing. They cannot, on their own, prove spiritual health, doctrinal fidelity, or the quality of discipleship in remote airstrips and village clinics. Mature evaluation holds both truths at once: financial documents are necessary for diligence, but insufficient for final judgment.

Across our verification work at Most Trusted, the ministries that meet The Most Trusted Standard tend to treat financial reporting as part of their Christian witness. They do not present transparency as a marketing posture. They present it as a discipline of integrity in the presence of God and neighbors.

Begin with the right documents and the right time horizon

For U.S. nonprofits, the Form 990 is often the most accessible baseline document. The IRS makes clear that tax-exempt organizations must make their Form 990 available for public inspection, which is one reason it remains a cornerstone for donor due diligence (IRS). When audited financial statements are available, they usually provide stronger assurance because they include notes, accounting policies, and an external auditor’s opinion.

Aviation ministries are also capital-intensive and weather cyclical. A single year can be distorted by a major maintenance event, aircraft acquisition, or a restricted grant. Donors should read at least three years of results when possible, and interpret anomalies cautiously rather than assuming misconduct or excellence from one number.

Read the Form 990 with aviation realities in mind

Revenue quality matters more than revenue size

The first question is not “How large is the budget?” but “How dependable and properly classified is the income?” Aviation ministries often receive a mix of individual gifts, church support, foundation grants, and occasionally program-related revenue. A healthy pattern is a diversified base that does not depend on one donor, one brokered gift stream, or one unusually favorable contract.

On the Form 990, compare total revenue to cash flow patterns described in narrative sections. Watch for ministries that report rising revenue while also reporting chronic liquidity strain, delayed payables, or repeated emergency appeals. Financial statements can be clean and still reveal an institution living too close to the edge for an aviation operation that must plan maintenance, pilot currency, and insurance well ahead of time.

Expense categories require careful interpretation in aviation

Donors often default to the program-versus-administration framing. The field has had to reckon with how that framing can mislead. Leaders across charity evaluation have publicly argued that focusing narrowly on overhead can punish ministries that invest in strong systems, which protect people and outcomes; Charity Navigator summarizes this shift in its discussion of the “overhead myth” and why overhead ratios alone are inadequate (Charity Navigator).

In aviation, a “low overhead” story can be especially dangerous if it means thin maintenance reserves, underinvestment in compliance, or weak financial controls. The harder question is whether spending aligns with mission and risk. A ministry that transports pastors, medical teams, and Scripture resources across difficult terrain may appropriately spend heavily on aircraft operations and safety systems that never appear “programmatic” to an uninformed reader.

Evaluate balance sheet strength and the discipline of reserves

Liquidity, not just surplus, keeps aircraft in the air

A balance sheet is where donor optimism meets operational reality. Pay particular attention to cash and cash equivalents, current liabilities, and net assets with and without donor restrictions. A ministry can show positive net assets while still lacking the liquid resources required for predictable maintenance cycles, insurance costs, and fuel price volatility.

When a ministry cannot absorb routine shocks, it is more vulnerable to unplanned risk-taking: deferring maintenance, pushing staff beyond safe limits, or expanding routes without adequate operational capacity. Those are not merely managerial missteps; they are stewardship failures with moral weight.

Restricted funds and designated gifts should be explained plainly

Aviation donors often designate gifts for aircraft purchases, hangars, training, or a particular country program. That is reasonable. It also creates complexity. Ministries should disclose, in straightforward language, how restricted contributions are tracked, when restrictions are released, and whether designated giving is creating strain on core operations.

A common tension is that donors love capital gifts, while the ministry must fund ongoing costs: pilots’ training hours, maintenance reserves, avionics updates, and compliance administration. A trustworthy ministry does not conceal that tension. It explains it and invites donors into informed partnership.

- Ask whether aircraft acquisitions come with an operating plan that includes maintenance and insurance, not only purchase price.

- Look for board-approved reserve practices appropriate for high-risk, high-cost operations.

- Confirm that restricted funds are not propping up general cash flow in ways that create future crises.

- Watch for chronic negative operating cash flow even when the income statement looks positive.

- Prefer clear, consistent classification of expenses year over year, with explanations for major changes.

Test governance signals that show up in the numbers

Related-party transactions and compensation deserve sober scrutiny

Donors should examine whether the Form 990 discloses loans to or from officers, business transactions with insiders, or unusual vendor relationships. In aviation, vendors may include maintenance shops, fuel providers, charter services, or aircraft brokers. Some related-party involvement can be legitimate, especially in smaller markets. The issue is whether it is disclosed, independently reviewed, and demonstrably fair.

Compensation should be evaluated with the same seriousness. A competent aviation CEO or operations leader may require specialized expertise, and underpaying critical roles can be a false economy. The question is whether compensation is set through a documented process, approved by independent board members, and consistent with comparable roles.

Audit quality and internal controls are not optional for aviation

An audit does not guarantee the absence of fraud, but it does raise the standard of accountability. If audited statements are available, read the auditor’s opinion and note any material weaknesses or significant deficiencies in internal controls. When a ministry is not audited, donors should ask what alternative accountability measures are in place and whether the ministry intends to pursue an audit as it scales.

For donors interested in broader patterns of accountability in this field, see Accountability and Transparency in Christian Aviation Ministries. The strongest organizations treat governance, controls, and transparency as integrated disciplines rather than isolated compliance tasks.

Connect financial reporting to effectiveness and Christian witness

Financial integrity should support verifiable ministry outcomes

Financial reporting is a means, not an end. Aviation ministry claims should be tested with the same care as financial claims: route metrics, safety practices, partner accountability, and evidence of local church strengthening. Christians genuinely disagree about what counts as “effectiveness” in mission work—especially when spiritual fruit cannot be reduced to a dashboard. Still, a ministry should be able to show how flights connect to real pastoral access, medical care delivery, Bible translation support, disaster response, or other clearly defined outcomes.

Where the reporting is thin, donors should ask whether the limitation is principled or convenient. Some security contexts require discretion. But discretion is not a permission slip for vagueness. Mature ministries provide meaningful, non-sensitive reporting: aggregate route data, broad outcome categories, audited summaries, and credible third-party partnerships.

Use a consistent framework rather than isolated red flags

Most donors have seen both extremes: ministries praised for low overhead that later collapse under weak controls, and ministries with strong systems that are unfairly criticized for investing in compliance and administration. What this means in practice is that donors benefit from an evaluative framework that keeps multiple criteria in view at once.

Most Trusted exists to serve that need for disciplined, faith-informed verification. We evaluate Christian nonprofits against The Most Trusted Standard, a 15-criteria framework that examines faith commitments, financial integrity, governance, and transparency with effectiveness. When donors want to understand the broader field, Christian Aviation Ministries provides context for why aviation work carries distinct operational demands and why diligence must be proportionate to the stakes.

FAQs for How to evaluate Christian aviation ministry financial reports

Should donors prioritize ministries with the lowest overhead ratio?

No. An overhead ratio can be a signal, but it is not a verdict. Aviation ministries require systems that protect safety and prevent financial misuse: maintenance planning, insurance oversight, compliance administration, and strong internal controls. A ministry that reports unusually low administrative costs may be underinvesting in precisely the structures that keep people safe and keep donor intent honored. Donors should look for consistency, clarity, and governance evidence rather than a single “low overhead” score.

What if an aviation ministry will not share audited financial statements?

Refusal is different from inability, and donors should ask which it is. Smaller ministries may not yet have the budget for a full audit, but they should still be willing to share Form 990s, internally prepared financial statements, board-approved budgets, and clear policies for handling restricted gifts. If a ministry has the scale to operate aircraft and employ specialized staff but consistently declines reasonable financial transparency, donors have grounds to pause and request stronger accountability before giving.

Financial diligence is part of faithful partnership

Christian aviation is a work of access, presence, and endurance. It can bring the means of grace and mercy to places the church cannot easily reach. That same reality requires donors to practice a form of love that includes scrutiny: reading the numbers, asking hard questions, and rewarding ministries that treat transparency as part of their discipleship. The goal is not suspicion. The goal is faithful partnership grounded in truth.