How often Christian counseling ministries should undergo audits is not a procedural question; it is a stewardship question. When a ministry receives gifts offered to God, donors have a reasonable expectation that leadership can demonstrate financial integrity with evidence, not assurances.

Counseling ministries carry a particular trust. They often handle restricted gifts, scholarship funds, and sensitive client-related expenditures. They also operate in a field where compassion can make donors reluctant to ask hard questions. Scripture commends generosity, and it also condemns weights and measures that cannot be trusted. “Unequal weights and unequal measures are both alike an abomination to the LORD” (Proverbs 20:10). In practice, credible audits are one of the clearest “equal measures” available in modern nonprofit life.

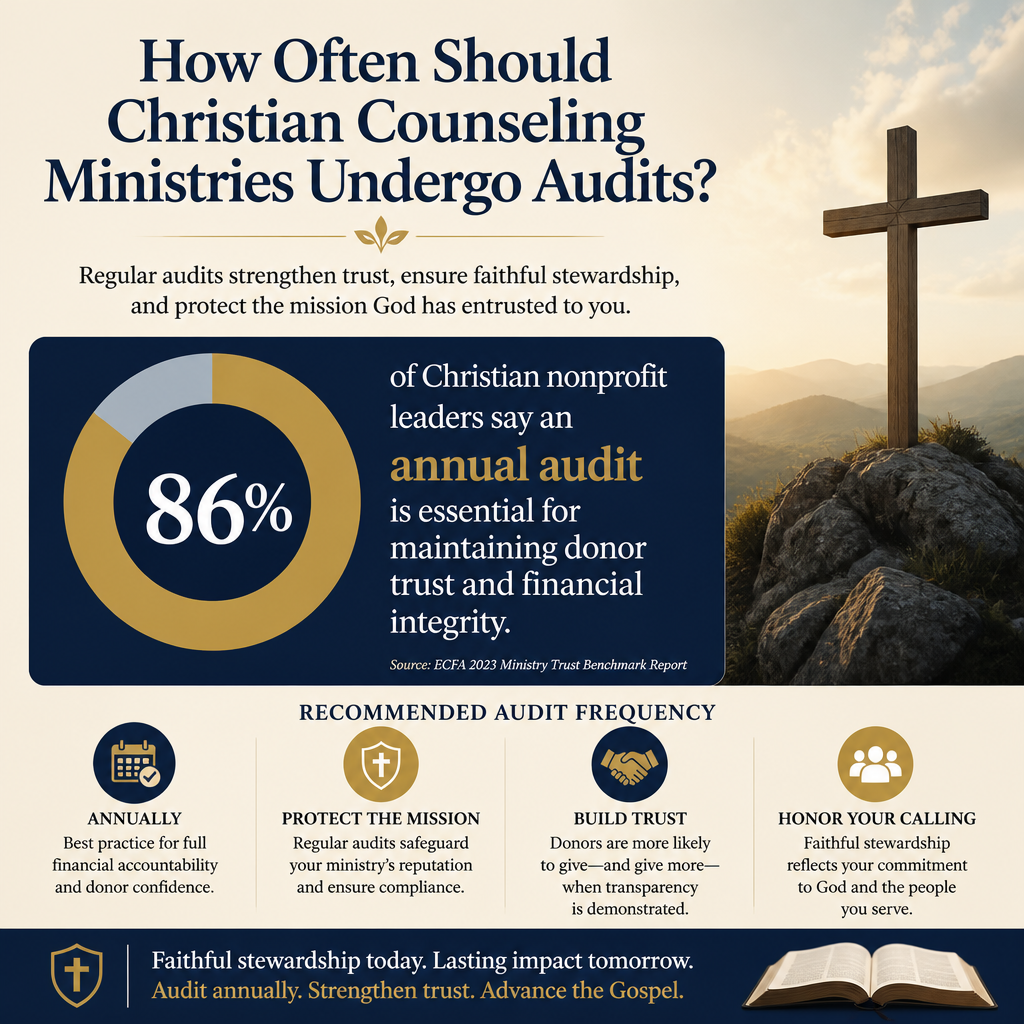

Annual independent financial audits are the baseline for mature ministries

Why annual matters for counseling ministries

For most established Christian counseling ministries, an independent financial statement audit every year should be treated as the baseline expectation, not a luxury. Annual cadence matters because cash flow, payroll, program subsidies, and restricted giving move continuously; delayed scrutiny tends to convert real-time correction into retrospective regret. When audit intervals stretch, board members and donors lose the ability to distinguish a temporary strain from a structural weakness.

Annual audits also discipline internal operations. Ministries that know an auditor will test revenue recognition, restricted fund treatment, and expense allocation tend to keep documentation clean throughout the year. That is not cynicism; it is accountability. In our verification work at Most Trusted, the ministries that meet The Most Trusted Standard typically treat audit readiness as a standing posture, not an annual scramble.

Audit versus review versus compilation

Not every external financial service is an audit. An audit provides the highest level of assurance and includes testing and confirmation procedures. A review offers limited assurance and relies more heavily on management representations. A compilation generally provides no assurance. Donors do not need to become accountants, but they should recognize that ministries may describe a review as though it were an audit. Clear terminology is part of transparency.

Right-sizing audit frequency depends on risk, scale, and funding complexity

When more than annual may be prudent

Some counseling ministries should go beyond an annual audit because their risk profile is higher. That is often true when a ministry manages multiple locations, operates residential programs, maintains significant receivables, or administers scholarship funds with heavy restrictions. It can also be prudent when rapid growth outpaces financial systems, or when there has been leadership transition in the finance function.

“More than annual” usually does not mean two full audits in a year. It may mean an annual audit plus interim testing, a separate agreed-upon procedures engagement around restricted funds, or a targeted internal control assessment. What this means in practice is that the board should identify where the ministry is most exposed and request independent testing in that area, not simply buy more general assurance than it can interpret or act on.

When less than annual can still be faithful stewardship

Some smaller ministries genuinely cannot carry the cost of a full annual audit without diverting resources away from frontline care. Christians genuinely disagree about where the line should be drawn between administrative rigor and program spending, and simplistic formulas do not serve the church. Even so, “we cannot afford an audit” should never become “therefore no external scrutiny.” A young ministry might begin with annual reviews, a strong board-level finance committee, and a clear plan to move to audits as revenue grows.

Donors should pay attention to whether leadership can name the plan, the timeline, and the triggers for moving up the assurance ladder. The absence of a plan often signals that leadership does not feel accountable to external standards. The presence of a plan signals prudence under constraint.

Donors should ask for more than an audit opinion

The audit opinion is not the only signal

A clean audit opinion is meaningful, but it is not exhaustive. Auditors give an opinion on whether financial statements are fairly presented in accordance with an accounting framework, not whether the ministry is making wise strategic choices or whether every internal control is strong. Donors should look for the surrounding documents that show governance seriousness: audited financial statements, notes, and—when applicable—a management letter that identifies control weaknesses and recommended improvements.

Where donors sometimes misread audits is assuming that “audited” means “safe.” Fraud can occur in audited organizations. Financial stress can accumulate without affecting the opinion. What the audit does provide is disciplined transparency and a credible check on whether the ministry’s financial reporting is reliable.

What to request and what to notice

For donors evaluating a Christian counseling ministry, we recommend asking for the most recent audited financial statements and confirming that they are posted or readily provided. If the ministry receives federal funds over the threshold, the Single Audit regime may apply and should be easy to document through the Federal Audit Clearinghouse. The requirement is triggered when an entity expends $750,000 or more in federal awards in a fiscal year, a threshold established in 2 CFR Part 200, Subpart F (eCFR: 2 CFR Part 200 Subpart F).

A short list of donor-level diligence questions can surface whether the audit is functioning as genuine accountability:

- Is the audit performed by an independent CPA firm, and is the firm named?

- Are the financial statements and notes available without resistance?

- Does the board have a finance or audit committee that meets regularly?

- Were there material weaknesses or significant deficiencies, and were they addressed?

- Are restricted gifts clearly separated and tracked?

When a ministry responds defensively to ordinary requests, that posture itself becomes information. Transparency is not a branding choice; it is a moral stance toward donors and beneficiaries.

Audit cadence should be integrated with governance and ministry realities

Counseling ministries face distinctive confidentiality pressures

Christian counseling ministries work with sensitive stories and real trauma. The field has had to reckon with the ethical demands of confidentiality, informed consent, and appropriate boundaries. Financial audits should never put client privacy at risk, but the existence of confidential data is not a reason to avoid independent scrutiny. It is a reason to ensure the ministry uses appropriate controls: segregation of duties, limited access to systems, and careful documentation practices that protect identity while still supporting financial accountability.

Donors should distinguish between client confidentiality and financial opacity. Ministries can safeguard counseling records while still producing clear financial reporting, credible audits, and board oversight. In fact, the disciplines tend to support each other: a ministry that takes confidentiality seriously often has the operational maturity to take financial controls seriously as well.

The board must own the audit relationship

The harder question is not whether an audit occurs, but who owns it. Best practice is for the board, or a board committee, to hire the auditor, receive findings, and ensure follow-through. When the audit is treated as a staff-only task, it often becomes a compliance event rather than a governance tool. Donors should feel free to ask whether the auditor meets with the board in executive session. That is not suspicion; it is normal fiduciary care.

Those giving into counseling ministries are often giving because they believe in restoration—marriages strengthened, addictions addressed, trauma held with skill and prayer. But restoration in Scripture is never opposed to truth-telling. A governance culture that welcomes honest assessment is better aligned with the moral shape of Christian ministry than one that equates scrutiny with distrust.

How The Most Trusted Standard frames audits for donor confidence

Audits sit within a larger accountability ecosystem

Financial audits matter, but donors do not give to financial statements. They give to ministry. The wise donor therefore places audits within a broader set of verifiable signals: faith commitments, governance quality, financial integrity, transparency, and evidence of effectiveness. That integrated approach is why Most Trusted evaluates ministries against The Most Trusted Standard, a 15-criteria framework that looks beyond a single document to the pattern of an organization’s life.

Across our work, the healthiest counseling ministries treat audits as one element of honesty before God and neighbor. They publish their audited statements, explain major changes plainly, and invite questions. They do not hide behind complexity, nor do they reduce stewardship to overhead ratios. The sector has widely recognized that simplistic overhead benchmarks can mislead donors and punish necessary investments in systems; Charity Navigator, BBB Wise Giving Alliance, and GuideStar articulated this in “The Overhead Myth” letter (Charity Navigator: The Overhead Myth).

Where donors can go deeper in this category

Donors focused on counseling ministries often want a coherent set of expectations: what documentation to ask for, what governance practices to expect, and what questions are fair without being cynical. Within Christian Counseling Ministries, we track the patterns that distinguish ministries that can sustain trust over time from those that depend on personality and goodwill. Within How to Give Wisely to Christian Counseling Ministries, we address the practical donor questions that arise when compassion meets accountability.

What this means for audit frequency is straightforward: donors should expect a rhythm of independent verification that matches the ministry’s complexity, and they should expect leadership to treat that rhythm as normal discipleship in stewardship, not as an external imposition.

FAQs for How often Christian counseling ministries should undergo audits

Should a Christian counseling ministry post its audit publicly?

Where feasible, yes. Public posting of audited financial statements is one of the simplest demonstrations that a ministry is not asking donors to operate on trust alone. If a ministry has legitimate constraints—for example, a security context or a complex affiliation—it should still provide the audit promptly upon request and explain the constraint plainly rather than using it as a blanket reason for opacity.

What if a ministry says an audit is too expensive?

Cost is a real constraint, especially for smaller ministries, but it should produce a credible plan rather than a permanent exemption. Donors can ask what level of external assurance the ministry currently uses, what internal controls are in place, and what revenue or complexity threshold will trigger moving to an annual audit. A ministry that treats the question as fair and answers with specificity is usually demonstrating the posture donors are hoping to find.

Audit frequency is a stewardship practice, not a box to check

Christian counseling ministries should generally undergo independent financial audits annually once they have reached meaningful scale, with additional targeted scrutiny when complexity and risk warrant it. The point is not to satisfy donor anxiety; it is to honor the moral weight of handling consecrated resources. Donors who ask for credible audits are not being adversarial. They are aligning their giving with the scriptural insistence that God’s work be conducted “in the light,” with measures that can be tested and found true.