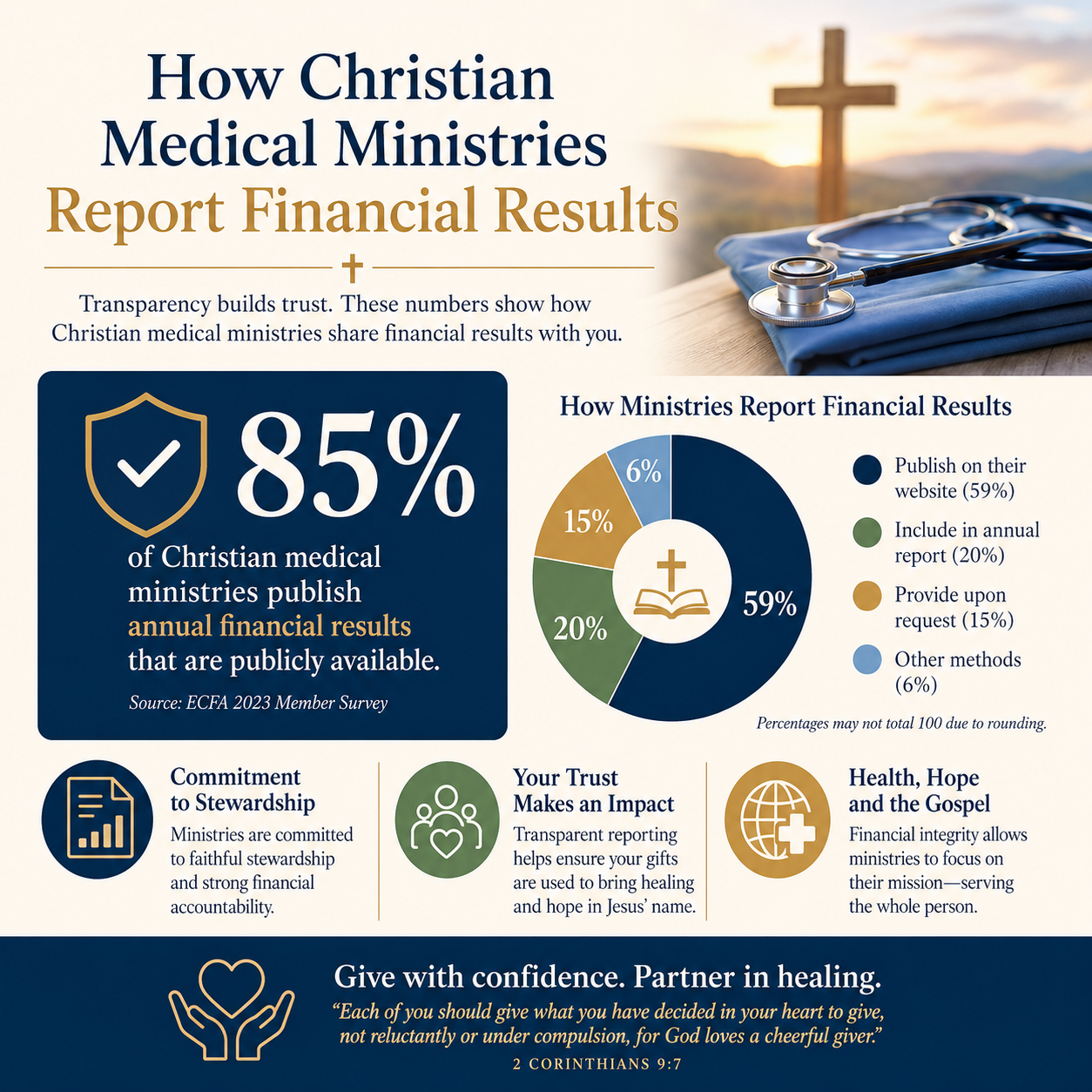

How Christian medical ministries report financial results is not a technical question for accountants alone. For Christian donors, it is one of the most practical tests of stewardship: whether a ministry’s public claims about healing, compassion, and integrity are matched by verifiable financial truth.

Scripture treats money as a discipleship issue, not a side concern. Jesus’ teaching in Luke 16 binds spiritual trustworthiness to financial faithfulness: “Whoever can be trusted with very little can also be trusted with much.” When donors fund medical work—often in contexts of vulnerability, trauma, and weak institutions—financial reporting becomes part of the ministry’s moral witness.

What donors should expect from a Christian medical ministry financial report

A serious financial report should help a donor answer a small set of hard questions: What came in? Where did it go? What is owed? What is reserved? What was accomplished? And what risks could jeopardize the work or compromise patient care?

For U.S.-based ministries, the most standard baseline is a set of audited financial statements prepared under Generally Accepted Accounting Principles, paired with an annual report that connects dollars to outcomes. Not every faithful ministry can afford an audit every year, especially smaller organizations, but a ministry’s size and complexity should raise expectations, not lower them.

Audited financial statements and the Form 990 are not interchangeable

Donors sometimes treat the IRS Form 990 as the “financial report.” It is a valuable disclosure document, but it is not a substitute for audited statements, and it can be misunderstood by readers who do not work with nonprofit accounting. Ministries should make both accessible when applicable, and they should explain major line items in plain language without minimizing complexity.

Some Christian medical ministries are churches or integrated auxiliaries and may not file a Form 990. That legal reality is not automatically a mark against them, but it does heighten the importance of voluntary transparency: audited statements, clear governance disclosures, and accessible explanations of how funds are handled.

Transparency should be structured, not improvised

Healthy reporting is consistent year to year. A donor should be able to trace continuity: accounting policies, revenue recognition, how restricted gifts are treated, and how major program categories are defined. When a ministry changes categories or renames expenses without explanation, the donor loses comparability, and trust erodes.

The core financial statements and what they do and do not prove

Most donors have seen a “statement of income and expenses” and assumed it tells the whole story. It does not. Medical work carries distinctive financial dynamics—inventory, clinical staffing, liability, and regulatory exposure—that require a full set of statements to interpret responsibly.

Statement of financial position shows resilience and risk

The balance sheet answers whether the ministry can endure volatility. Cash reserves, receivables, payables, debt, and net assets are not merely accounting categories. They are signals of how a ministry will respond when supply costs spike, a disaster doubles patient volume, or a major grant is delayed.

Donors sometimes punish ministries for holding reserves, assuming every dollar should be spent immediately. Yet nonprofit research and professional standards generally recognize reserves as prudent risk management. The question is not whether reserves exist, but whether reserves are governed, explained, and proportional to the ministry’s obligations.

Statement of activities must be read with restrictions in mind

Medical ministries often receive restricted gifts: funds designated for a clinic build-out, a specific country program, a mobile medical unit, or medication purchases. A ministry can show a surplus while still facing cash constraints if much of its revenue is restricted. Conversely, it can show a deficit while funding capital projects with restricted gifts. Financial reports should clearly distinguish restricted and unrestricted net assets and explain material movements.

Statement of cash flows is where sustainability becomes visible

Cash flow is where many ministries quietly struggle. A ministry may report strong revenue but suffer delayed reimbursements, slow pledge fulfillment, or rapidly rising costs in pharmaceuticals and logistics. A mature report helps donors understand whether program expansion is supported by recurring cash generation or by temporary funding spikes.

Program expenses and the overhead debate in medical ministry

Christian donors often ask, “How much goes to the mission?” It is a fair question. It is also a question that can be mishandled, especially in medical ministry where administrative infrastructure is often a precondition for safe, compliant care.

Overhead ratios are a weak proxy for integrity

Expense allocation categories—program, management and general, fundraising—are governed by accounting standards, but they still require judgment. A clinic’s medical director may train local staff (program), ensure compliance and safety protocols (management), and speak at donor events (fundraising). Ministries should disclose allocation methodologies and avoid presenting simplistic ratios as moral proof.

The sector has publicly rejected the idea that low overhead is synonymous with effectiveness. In 2013, Charity Navigator, GuideStar, and BBB Wise Giving Alliance issued an open letter warning donors against judging nonprofits primarily by overhead ratios and urging attention to results, transparency, and governance Charity Navigator.

What donors should ask instead of hunting for the lowest percentage

Across our verification work at Most Trusted, the ministries that meet The Most Trusted Standard tend to treat cost reporting as an act of truth-telling, not a marketing exercise. They can explain why certain costs exist and why those costs protect patients and honor donors.

- How are shared costs allocated, and who approves the methodology?

- What compliance and safeguarding systems are funded, and what incidents have those systems prevented?

- How does the ministry control medical supply chain risk, theft, and spoilage?

- What is the ministry’s reserve policy, and what scenarios is it designed to cover?

- How does leadership evaluate program effectiveness beyond activity counts?

Outcome reporting that matches medical realities and Christian ethics

Financial results are necessary but not sufficient. Christian medical ministry is not only a transfer of goods and services; it is an expression of mercy shaped by truth, dignity, and wise action. Reporting should respect the medical complexity of patient care and the Christian insistence that people are not metrics.

Outputs are easy to count and easy to misuse

Numbers like “patients served” or “surgeries performed” can be meaningful, and donors understandably want them. But output counts can conceal failures in quality, follow-up, or local capacity-building. A mobile clinic that reports high volume but lacks continuity of care may unintentionally burden local systems or leave chronic conditions unmanaged.

Responsible ministries pair output counts with at least some indicators of quality and continuity: referral completion rates, adherence to clinical protocols, medication availability, patient education, and local partner capacity. Where privacy laws and security concerns constrain public disclosure, a ministry can still describe its measurement approach and governance safeguards.

Medical ministry must be careful with storytelling

Christian donors respond to testimony because the gospel is, in part, proclaimed through witness. Yet medical storytelling can drift into exploitation if it trades on graphic detail, identifiable images, or unverified “miracle” claims. A ministry’s reporting should show restraint, consent practices, and patient dignity.

In the wider field of development and relief, the When Helping Hurts framework articulated by Steve Corbett and Brian Fikkert has influenced Christian thinking about unintended harm and the importance of dignity, participation, and long-term flourishing When Helping Hurts. Medical ministries operate under similar moral constraints: compassion must be competent, and competence must be accountable.

Governance and controls that make financial results trustworthy

The hardest financial failures in Christian ministry are often governance failures before they become accounting failures. A glossy annual report can coexist with weak internal controls, concentrated power, and unclear accountability—conditions that can deteriorate quickly under the pressure of growth or crisis.

Board oversight and related-party disclosures matter more than polish

Donors should expect clear disclosure of board composition, independence, meeting frequency, conflict-of-interest policies, and any related-party transactions. In medical settings, relationships with suppliers, clinics, and overseas partners can create genuine conflicts. Transparency does not eliminate temptation, but it does reduce concealment.

Many donors begin their orientation through broader context on Christian Medical Ministries, then evaluate a specific organization’s governance and reporting practices against credible standards. What donors are ultimately seeking is not perfection, but trustworthy patterns: clarity, consistency, and accountability.

Internal controls are a ministry of protection

Strong internal controls are not a sign of distrust; they are a form of care. Segregation of duties, approval thresholds, inventory controls for pharmaceuticals, documented procurement processes, and independent review all reduce the likelihood that a ministry’s people will be placed in compromising situations.

For donors who want to go deeper on how ministry dollars are handled in practice, How Christian Medical Ministries Use Donations provides additional context on typical cost structures, cross-cultural partnership models, and the risks that responsible reporting should address.

FAQs for How Christian medical ministries report financial results

Should a Christian medical ministry always have an independent audit?

An independent audit is a strong marker of financial maturity, especially as a ministry grows in revenue, geographic complexity, and regulatory exposure. Smaller ministries may not yet have the resources for annual audits, but they should still provide credible financial statements, transparent policies, and some form of independent oversight. The key donor question is whether the ministry’s reporting and controls match the scale of the funds entrusted to it.

Is it a red flag if a ministry spends more on administration than donors expect?

Not necessarily. In medical work, administration often includes compliance, credentialing, safeguarding, supply chain controls, quality assurance, and financial systems that protect both patients and donors. A better approach is to ask what those costs fund, how they are governed, and whether the ministry can demonstrate competence and outcomes without manipulating expense categories to appear lean.

Financial reporting is part of a ministry’s public discipleship

Christian donors give to medical ministry because the sick matter to God, and because mercy is not optional for Christ’s people. But mercy must be joined to truth. When Christian medical ministries report financial results with clarity, independent verification where appropriate, and sober attention to outcomes and risk, they do more than satisfy curiosity. They honor the Lord who sees, protect the vulnerable they serve, and give donors a basis for confident stewardship.