How Christian Donor-Advised Funds work is a practical question with spiritual weight. For many donors, the donor-advised fund is not merely a tax tool; it becomes a recurring decision point about stewardship, timing, trust, and conscience.

A DAF can strengthen disciplined generosity, especially for believers who want to give thoughtfully across years rather than impulsively in moments of crisis. It can also create new temptations: indefinite delay, overconfidence in financial engineering, or a subtle shift from cheerful giving to perpetual planning. Christian donors do well to understand the mechanics clearly, because the mechanics shape the heart.

What a Christian donor-advised fund is and what it is not

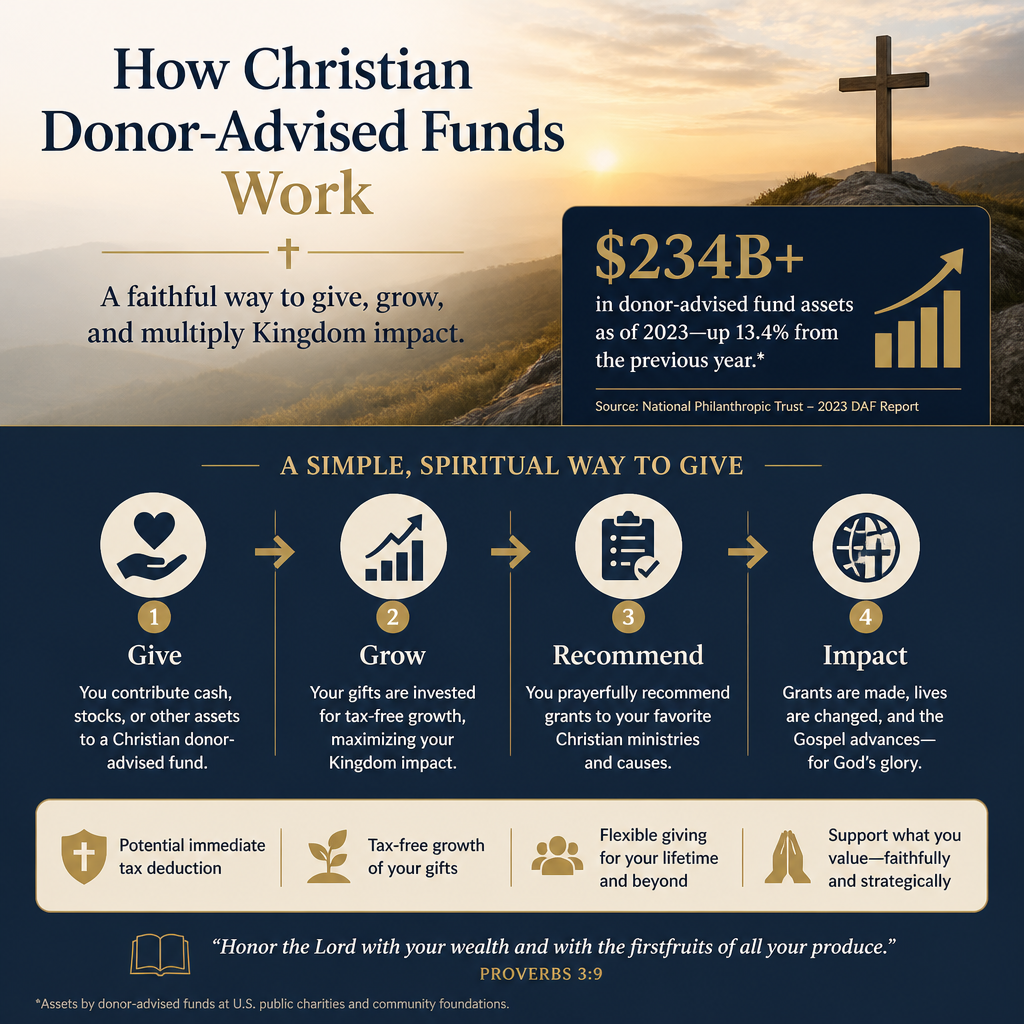

A donor-advised fund is a charitable account administered by a sponsoring organization. You make an irrevocable charitable contribution to the sponsor, receive a charitable deduction subject to IRS rules, and then recommend grants over time to IRS-qualified public charities. The sponsor has legal control of the assets; you retain advisory privileges that the sponsor generally follows if the grant request is eligible and properly documented.

The distinct claim of a Christian donor-advised fund is not that it changes the legal structure, but that it adds mission-specific guardrails. Those guardrails can include faith-aligned grant policies, biblically informed counsel, and investment options that avoid direct support of certain industries. For donors concerned with theological coherence, this can matter as much as administrative convenience.

Irrevocable gift, ongoing influence

The “irrevocable” nature of the contribution is the first point many donors miss. Once assets are contributed, they are no longer yours; they belong to the sponsoring charity. Your ongoing role is advisory. That distinction is not a technicality. It is part of the moral clarity of giving: “Where your treasure is, there your heart will be also” (Matthew 6:21). A DAF formalizes the moment when treasure changes hands, even if grants are made later.

DAFs are not private foundations

DAFs and private foundations both allow structured grantmaking, but they operate under different rules and expectations. Private foundations carry extensive compliance responsibilities, separate tax filings, and self-dealing restrictions; they also typically require greater donor administration. DAFs were built to reduce friction for donors who want the benefits of organized giving without running a standalone entity.

DAFs do not solve the “trust problem” by themselves

Christian donors often come to DAFs after some disillusionment—unclear reporting, celebrity leadership failures, financial opacity, or simply the fatigue of evaluating ministries while managing family and business responsibilities. A DAF can centralize recordkeeping and help with due diligence, but it cannot replace discernment. The sponsoring organization becomes a critical intermediary, and the ministries receiving grants still require evaluation.

How the flow of money works from donation to grant

The operational path of a DAF is straightforward, but each step introduces decisions that shape outcomes. Donations are received, receipted, and placed in the donor’s advised fund. Assets may be held in cash or invested. The donor later recommends grants to specific charities, and the sponsor performs eligibility checks before sending funds.

Contributing cash or appreciated assets

Many donors begin with cash contributions because they are simple. Over time, donors with appreciated assets often contribute securities or other non-cash assets because the tax treatment can be more favorable than selling first and donating the proceeds. This is an area where wise counsel matters; complex assets can involve valuation questions, liquidity delays, and sponsor policies that differ materially from one provider to another.

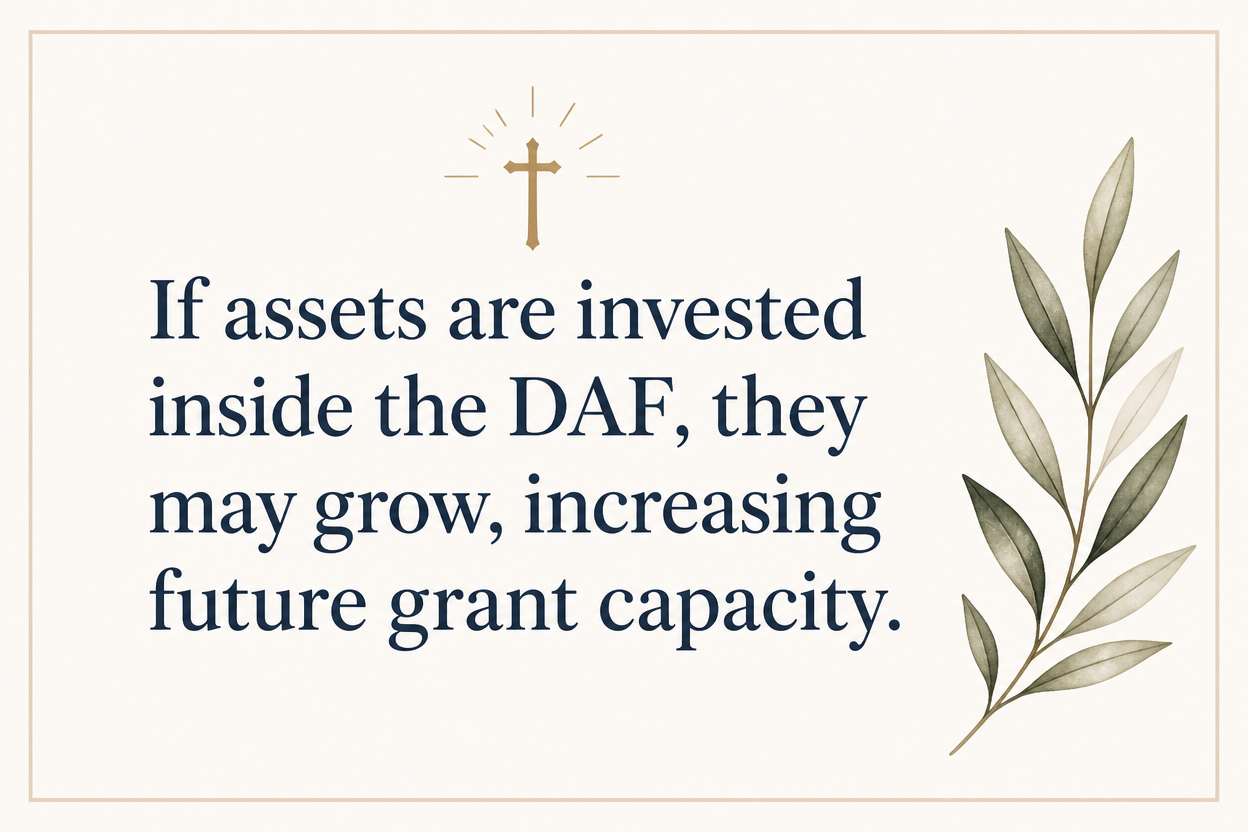

Investments, growth, and the moral question of delay

If assets are invested inside the DAF, they may grow, increasing future grant capacity. That can be good stewardship when it serves real ministry needs over time—supporting long-term commitments, planned giving strategies, or multi-year initiatives. Yet Christians genuinely disagree about how long charitable assets should remain ungranted. Some view extended warehousing of funds as inconsistent with the New Testament’s urgency about meeting needs; others emphasize prudence and sustainability.

What this means in practice is that donors should treat “investment inside the DAF” as a means, not an end. The question is not merely whether the account grew; the question is whether the account served faithful obedience. “Each one must give as he has decided in his heart, not reluctantly or under compulsion, for God loves a cheerful giver” (2 Corinthians 9:7). Cheerfulness can coexist with planning, but it rarely coexists with indefinite postponement.

Recommending grants and confirming eligibility

When you recommend a grant, the sponsor typically confirms that the recipient is a qualified public charity and that the grant does not provide impermissible benefits to the donor (such as tickets, memberships with benefits, or payments that satisfy a legally enforceable pledge in ways the sponsor prohibits). Christian DAFs may also apply faith-based screening, such as requiring alignment with orthodox Christian beliefs or excluding grants to organizations engaged in activities contrary to their mission.

This is one reason Christian donors often prefer a Christian sponsor: the sponsor’s grant policies effectively become part of the donor’s moral perimeter. If a donor expects the sponsor to act as a guardrail, the donor should review the sponsor’s statement of faith, grant guidelines, and exception process before contributing.

Where Christian donors experience friction and how to think faithfully about it

DAFs promise simplicity, but mature donors quickly discover pressure points: fees, restrictions, the complexity of ministry vetting, and contested questions such as tithing through a DAF. Those tensions are not signs that the model is broken. They are reminders that modern financial tools always form us in some direction, and Christians should name that formation rather than ignore it.

Tithing, church giving, and conscience

Some Christian DAF sponsors allow grants to local churches; others do not. Some donors also wonder whether contributing to a DAF “counts” as tithing. Scripture’s teaching on firstfruits, proportionate giving, and generosity is clear, but Christians apply those principles differently across covenantal frameworks and church traditions.

Our counsel is to treat the local church as a primary stewardship responsibility and to avoid letting the DAF become a mechanism for delay or detachment. If a DAF is used to support the church, donors should still preserve the spiritual discipline of regular, proportionate giving and the relational accountability of membership. The question is not only deductibility; it is discipleship.

Fees and the true cost of administration

DAFs charge administrative fees, and the underlying investment options typically carry their own expenses. The moral question is not whether fees exist—administration costs money—but whether fees are disclosed, reasonable, and justified by service quality. Fee schedules also shape behavior: high minimums and layered fees can push smaller donors away; very low fees can coincide with minimal service and minimal accountability.

Donors should read fee schedules as carefully as they read ministry budgets. The “Overhead Myth” conversation in the broader nonprofit sector has clarified that overhead ratios alone do not measure effectiveness, but disclosure and governance still matter. The open letter signed by GuideStar, Charity Navigator, and BBB Wise Giving Alliance remains a useful reference point for thinking about this responsibly: GuideStar.

Ministry evaluation remains the central challenge

A DAF can make giving easier; it does not make giving wise. The hardest work for serious Christian donors is assessing whether a ministry is doctrinally sound, financially trustworthy, governed well, and genuinely effective in its stated mission. That work is especially difficult because Christian ministry outcomes are not always quantifiable, and because religious language can be used to obscure weak accountability.

This is where Most Trusted’s work intersects naturally with DAF use. Across our verification work, we evaluate ministries against The Most Trusted Standard, a 15-criteria framework that examines faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. Donors who use a DAF often find that rigorous third-party verification helps them move from generalized goodwill to defensible confidence, especially when making larger or repeated grants.

Choosing a DAF and building a grantmaking practice that holds up over time

DAFs reward clarity. Donors who articulate purpose, boundaries, and a rhythm of giving tend to use the tool in ways that produce both spiritual and practical fruit. Donors who treat the DAF as a holding tank tend to accumulate complexity and lose momentum.

Selection criteria that matter for Christian donors

Christian donors should ask direct questions in four categories. First, mission and theology: what is the sponsor’s doctrinal basis, and how does it affect grant eligibility? Second, governance and accountability: who oversees the sponsor, what audits occur, and how are conflicts handled? Third, grant policies: can you support churches, missionaries, and international work, and what documentation is required? Fourth, service and transparency: what reporting will you receive, how quickly are grants processed, and how clearly are fees disclosed?

It is also wise to assess how the sponsor handles complex cases: designated gifts, scholarship-like assistance, disaster relief, and grants to organizations with mixed activities. Mature donors should not assume that “Christian” automatically means consistent policies. It simply means the sponsor has chosen a Christian frame; the donor still must evaluate how that frame is administered.

When it is prudent to open a DAF

DAFs are commonly opened in years of unusual income or major asset events: a business sale, large bonus, equity vesting, or the sale of highly appreciated securities. The donor can separate the timing of the charitable deduction from the timing of ministry distributions. That flexibility can be legitimate stewardship, but it should not become an excuse to postpone generosity. If the donor’s intent is to give, a DAF can help execute that intent with order and documentation.

For donors with steady giving patterns and no appreciated assets, a DAF may still be appropriate if it simplifies recordkeeping, helps structure family philanthropy, or supports a focused grantmaking strategy. But the tool should earn its place; simplicity is not free, and not every donor needs another financial account.

Practices that protect joy and accountability

Three practices tend to keep DAF giving spiritually healthy. First, set a grantmaking cadence—monthly, quarterly, or annually—so funds do not languish. Second, establish a ministry evaluation process proportionate to the size and risk of the grant. Third, keep gratitude and prayer close to the act of giving, so the DAF does not reduce generosity to a spreadsheet exercise.

Many families also use a DAF to disciple the next generation: involving adult children in reviewing ministries, discussing theological alignment, and learning to read financial statements without cynicism. That formation is slow, but it is one of the quiet strengths of the model when used intentionally.

A tool that can serve obedience or subtly replace it

Christian donor-advised funds work best when they are treated as an instrument of faithful stewardship rather than a substitute for it. The legal structure can bring order, tax efficiency, and administrative relief, but it cannot confer discernment, courage, or love of neighbor. Those are spiritual realities, not financial features.

For donors weighing whether a DAF belongs in their stewardship practice, it is worth returning to first principles: God owns all things; we are entrusted stewards; and generosity is meant to be both wise and active. For further context on the broader landscape, see Christian Donor-Advised Funds.