Giving strategies using Christian donor-advised funds often begin with a deceptively simple question: how does a Christian give with both conviction and clarity when needs are urgent, opportunities are uneven, and tax rules are complex. A donor-advised fund can serve holy ends or merely efficient ones. The difference is not the account itself, but the spiritual and practical discipline brought to it.

A DAF separates the timing of a donor’s charitable contribution from the timing of the grants. That separation is powerful. It can also become morally weighty. Scripture treats money as a revealer of loyalty and love, not as a neutral tool; Jesus’ warnings about treasure and trust are not addressed only to the greedy, but to disciples who may sincerely want to serve God (Matthew 6:19–24). What follows are strategies we see mature donors use when they want a DAF to support genuine stewardship rather than simply provide flexibility.

Begin with theological stewardship, not tax efficiency

DAFs are frequently introduced through the language of deduction management. That is not wrong, but it is incomplete. Christian giving is an act of worship and justice before it is an act of financial planning. A DAF is best understood as a stewardship instrument: it helps a donor hold resources with open hands, direct them with wisdom, and release them with consistency.

Define the account’s purpose and moral boundaries

Across our verification work at Most Trusted, we observe that donors who are clearest about their purpose tend to make fewer reactive gifts and fewer gifts driven by urgency alone. A simple written statement often helps: what causes and communities is this DAF meant to serve, what kinds of ministries will be prioritized, and what kinds of requests will be declined even when emotionally compelling.

This is not about narrowing compassion. It is about refusing the subtle drift that can occur when a DAF becomes a “holding tank” that keeps generosity perpetually postponed. The New Testament’s emphasis on readiness—“as we have opportunity, let us do good” (Galatians 6:10)—pushes against indefinite deferral. Discipline is part of devotion.

Hold the church and the poor in view at the same time

Christians genuinely disagree about how to sequence giving: some prioritize the local church first as the ordinary locus of mission; others distribute giving more broadly across global and specialized ministries. The DAF can serve either approach, but it should not become a rationale to reduce support for a healthy local church. If a church depends on predictable giving for staffing, mercy funds, and long-term discipleship, then using a DAF only for occasional grants can unintentionally introduce instability.

At the same time, a DAF can strengthen mercy ministry by allowing a donor to respond to real needs without destabilizing household finances. Wisdom literature commends planning without trusting in plans. What this means in practice is that a DAF can be used to create a “margin” for generosity—so that aid to the poor is not always an emergency and never a performance.

Use a verification lens early, not after disappointment

The question is not whether Christian nonprofits sometimes fail; they do, and the harm to trust can be severe. The question is whether donors will treat ministry credibility as an assumption or as a claim to be evaluated. Most Trusted exists to help donors give with confidence by evaluating ministries against The Most Trusted Standard, a 15-criteria framework spanning faith commitments, financial integrity, governance practices, and transparency and effectiveness. When donors apply that kind of lens before making recurring commitments, they tend to experience fewer reversals and fewer “quiet withdrawals” from generosity after a scandal.

For readers seeking a broader orientation to account design and ministry evaluation, see our work on Christian Donor-Advised Funds.

Fund the DAF with assets that match your calling and constraints

DAF strategy becomes concrete when a donor decides what to contribute. The asset choice affects taxes, liquidity, the timing of grants, and the donor’s ability to remain faithful under pressure. Some of the most effective strategies are simply disciplined ways of giving what is already present in a household’s financial life.

Consider giving appreciated assets rather than only cash

For donors with taxable brokerage accounts, contributing appreciated securities can be one of the clearest examples of wise stewardship. Done properly, it can align the donor’s desire to give with an honest recognition that taxes are not a virtue in themselves, but a cost to be managed responsibly. The IRS explains that when a donor gives long-term appreciated property to a qualified charity, the donor may generally deduct the fair market value and avoid capital gains tax on the appreciation, subject to limitations and substantiation rules. See the IRS guidance at irs.gov.

The harder question is not whether this is legal; it is whether it is spiritually fitting. For many donors, the discipline of giving appreciated assets counters a tendency to give only from surplus cash flow. It is a way of offering something that has grown over time, rather than something that happens to be liquid today.

Use bunching when it serves generosity rather than gaming

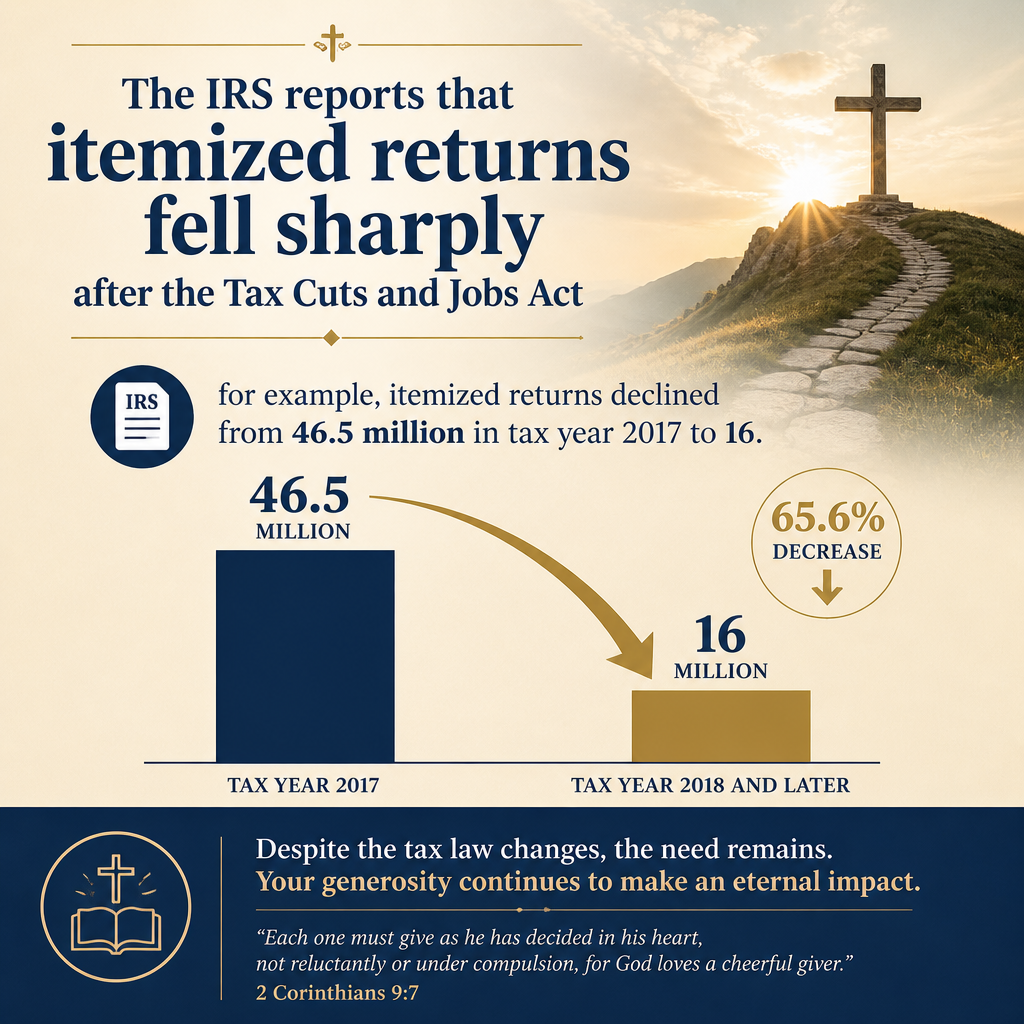

Some donors contribute multiple years of intended giving into a DAF in one tax year, then recommend grants over several years. This “bunching” approach can make sense in the post-2017 environment where fewer households itemize deductions. The IRS reports that itemized returns fell sharply after the Tax Cuts and Jobs Act; for example, itemized returns declined from 46.5 million in tax year 2017 to 16.7 million in tax year 2018. See the IRS Statistics of Income data at irs.gov.

The moral risk is treating bunching as the point rather than the instrument. If bunching accelerates giving into a DAF but grants slow down, the effect is to improve a tax outcome while delaying impact. Mature practice sets a grant cadence at the same time the bunching contribution is made, so the strategy does not quietly become an excuse for postponement.

Plan for illiquid gifts and complex assets with sobriety

Some DAF sponsors accept gifts such as private business interests, certain real estate, or restricted partnership interests. Others do not. Even when accepted, the timeline from contribution to liquidation can be unpredictable, and the donor’s deduction rules may differ from publicly traded securities. The relevant point is not maximal complexity; it is alignment. If an asset is illiquid and the donor expects to fund urgent ministry needs, the mismatch can create frustration and rushed granting later.

When a donor expects to give complex assets, it is prudent to coordinate early with qualified counsel and with the DAF sponsor’s policies. The aim is not sophistication for its own sake, but a form of honesty: counting the cost before making commitments.

Establish a grant rhythm that respects urgency, accountability, and formation

DAFs can tempt donors into two opposite errors: granting impulsively under emotional pressure, or granting rarely because the “right time” never arrives. A faithful strategy creates a deliberate rhythm—regular enough to form generosity, structured enough to respect accountability, and flexible enough to respond to crises.

Choose a baseline cadence and protect it

Many donors do well with a simple pattern: a monthly baseline for core commitments, plus quarterly or semiannual reviews for additional grants. This mirrors how many ministries actually operate—budgets are steady, while special projects are episodic. It also reduces the likelihood that giving becomes a sporadic reaction rather than a stable vocation.

For donors who want their DAF to support both local and global work, the cadence can be divided: baseline support to a church or long-term partners, with the review cycle reserved for opportunities and emergencies. The moral discipline here is predictability. Faithfulness is often less dramatic than donors expect, but more consequential over decades.

Discern when to grant immediately and when to wait

Not every need should be funded instantly. Some requests require due diligence: governance questions, financial controls, theological alignment, or a track record of measurable work. But waiting is not inherently virtuous either. In a disaster or acute crisis, delay can be its own form of harm, particularly for ministries providing food, shelter, medical care, or evacuation support.

The wiser approach is to decide in advance what triggers rapid response. For example: “When a verified ministry partner faces a sudden crisis, we will grant within 48 hours.” For less familiar ministries, a waiting rule can apply: “We will not fund first-time requests until basic documentation is reviewed.” This turns discernment into a practice rather than a mood.

Give in ways that reduce the overhead obsession

Some donors default to overhead ratios as a shortcut for trust. The charitable sector has repeatedly argued that this can mislead donors and harm nonprofits by incentivizing underinvestment in systems and staff. Charity Navigator, Candid (GuideStar), and the BBB Wise Giving Alliance published a joint letter urging donors to move beyond overhead as the primary measure of nonprofit performance. See the letter posted by Charity Navigator at charitynavigator.org.

This does not mean abandoning scrutiny. It means asking better questions: Are leaders accountable? Are financial statements transparent? Is the ministry candid about results and limits? Are there independent board practices? DAF strategy is at its best when it funds effectiveness and integrity, not merely frugality.

Handle anonymity, church support, and restricted giving with integrity

A DAF is not only a financial instrument; it is also a social instrument. It affects how donors are seen, how relationships with ministries are managed, and how influence is exercised. These are spiritual matters. The DAF can either protect humility and trust, or it can enable control and distance.

Use anonymity to protect humility, not to avoid accountability

Anonymous giving has a clear biblical resonance in Jesus’ warning against public display (Matthew 6:1–4). A DAF can make anonymity relatively easy. That can be a gift to both donor and recipient, particularly when public recognition would distort motives or create unhealthy dependence on a single family.

The tension is that anonymity can also make accountability harder for the donor. If a ministry never knows who is giving, it cannot ask clarifying questions or provide tailored reporting. Some donors address this by remaining anonymous publicly while establishing a private point of contact through the DAF sponsor, or by choosing partial anonymity (name disclosed, amount withheld). The aim is humility without opacity.

Support local churches without turning grants into preferences

Supporting a local church through a DAF can be appropriate, but it should be done with a clear understanding of the church’s policies and the DAF sponsor’s rules. Churches often have designated funds, capital campaigns, and benevolence accounts; donors should avoid creating restrictions that require special handling or that function as personal directives rather than gifts.

A prudent strategy is to ask the church directly how to give in a way that strengthens its mission and reduces administrative burden. If the intent is to support a pastor or missionary personally, donors should confirm whether the gift is permissible and whether it should be made through established channels to avoid tax and governance complications. Integrity in giving is not merely compliance; it is love expressed with order.

Resist restricted giving when it becomes control

Restrictions can be legitimate. Donors may want to support a specific program, a translation project, a crisis response, or a church plant. Yet restrictions can also become a subtle form of power that burdens ministries and undermines their judgment. Experienced leaders regularly report that narrowly restricted gifts can create underfunded core operations and distort priorities.

The more strategic approach is to reserve restrictions for cases where a donor has high confidence in the ministry’s capacity and reporting, and to prefer broader designations that still honor the donor’s intent. When a donor trusts a ministry’s governance and transparency, unrestricted or lightly restricted giving often produces more durable impact.

DAF strategy is a spiritual discipline with measurable consequences

Christian donors often want both spiritual faithfulness and practical confidence. A DAF can serve that desire when it is governed by a clear purpose, funded thoughtfully, granted with disciplined rhythm, and practiced with humility in relationships. The account’s flexibility is not a substitute for discernment; it is an invitation to deeper discernment.

Most Trusted’s work consistently reinforces a basic pattern: when donors combine theological seriousness with verifiable evaluation, giving becomes steadier, less reactive, and more aligned with the long obedience of discipleship. The point is not to perfect a technique, but to order resources toward love of God and neighbor with integrity that can withstand scrutiny.