How to give stock to discipleship ministries is, at its best, a question about stewardship and formation at the same time. The mechanics matter because they determine whether more of what God has entrusted to a donor can be directed toward ministry rather than taxes. The discernment matters because discipleship work is often difficult to measure, easy to market, and vulnerable to shortcuts that produce activity without spiritual depth.

Scripture does not treat wealth as morally neutral. Jesus’ warnings about money are sustained and direct, and the early church’s patterns of generosity are inseparable from the church’s life together. For donors with appreciated securities, giving stock can be one of the clearest ways to align financial prudence with a sincere desire to “excel in this act of grace also” (2 Corinthians 8:7).

Why stock can be one of the most faithful ways to fund discipleship

Appreciated assets often carry hidden tax friction

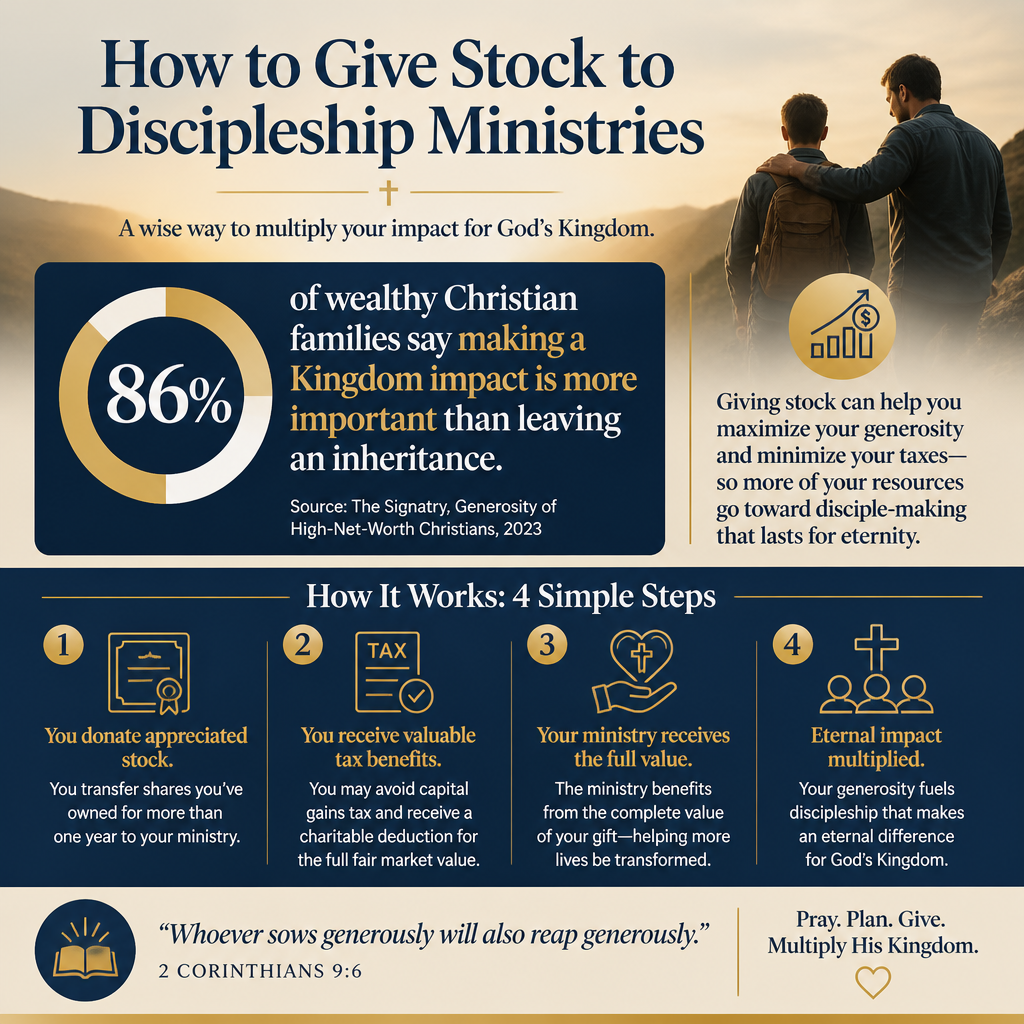

When donors sell appreciated stock to give cash, the capital gain can reduce what ultimately reaches a ministry. A straightforward alternative is to give long-term appreciated securities directly to a qualified charity, typically allowing the donor to avoid capital gains tax while claiming a charitable deduction (subject to IRS rules and individual circumstances). The IRS explains these general principles in its charitable contribution guidance and publications (IRS Charitable Contributions).

What this means in practice is that stock gifts can increase ministry funding without increasing a donor’s out-of-pocket cost. For discipleship ministries, where budgets are frequently constrained and program costs are real (curriculum development, trained staff, pastoral coaching, safeguarding, data systems), marginal dollars often translate directly into real capacity.

Discipleship is long-term work that benefits from stable, planned generosity

Many discipleship outcomes unfold over years: Scripture fluency, habits of prayer, resilience in suffering, faithfulness in vocation, and durable commitment to the local church. Donors who fund that kind of work often find that disciplined, repeatable giving patterns matter more than occasional spikes of generosity. Stock giving can support that stability, particularly when donors set a practice of gifting a portion of annual appreciated positions or using a donor-advised fund to smooth year-to-year volatility.

Christians genuinely disagree about the best models for discipleship at scale—para-church versus local church embedded, digital-first versus relationally intensive, cohort models versus apprenticeship. But the shared premise is that formation is rarely efficient. Giving stock well is partly about accepting that reality and funding ministries whose designs reflect it.

Decide whether you are giving stock directly, through a DAF, or through a foundation

Direct stock gifts can be simple when the ministry is prepared

Some discipleship ministries have brokerage accounts and clear instructions for stock transfers. In those cases, a donor’s broker can deliver shares directly. Done well, this is straightforward. Done poorly, it can create administrative confusion, delays, and misapplied gifts—especially around year-end.

Across our verification work at Most Trusted, we observe that administrative readiness is not a superficial concern. Ministries that handle stock gifts well usually have clear gift acceptance policies, documented internal controls, and timely donor receipting practices—habits that also tend to correlate with wider financial integrity and transparency.

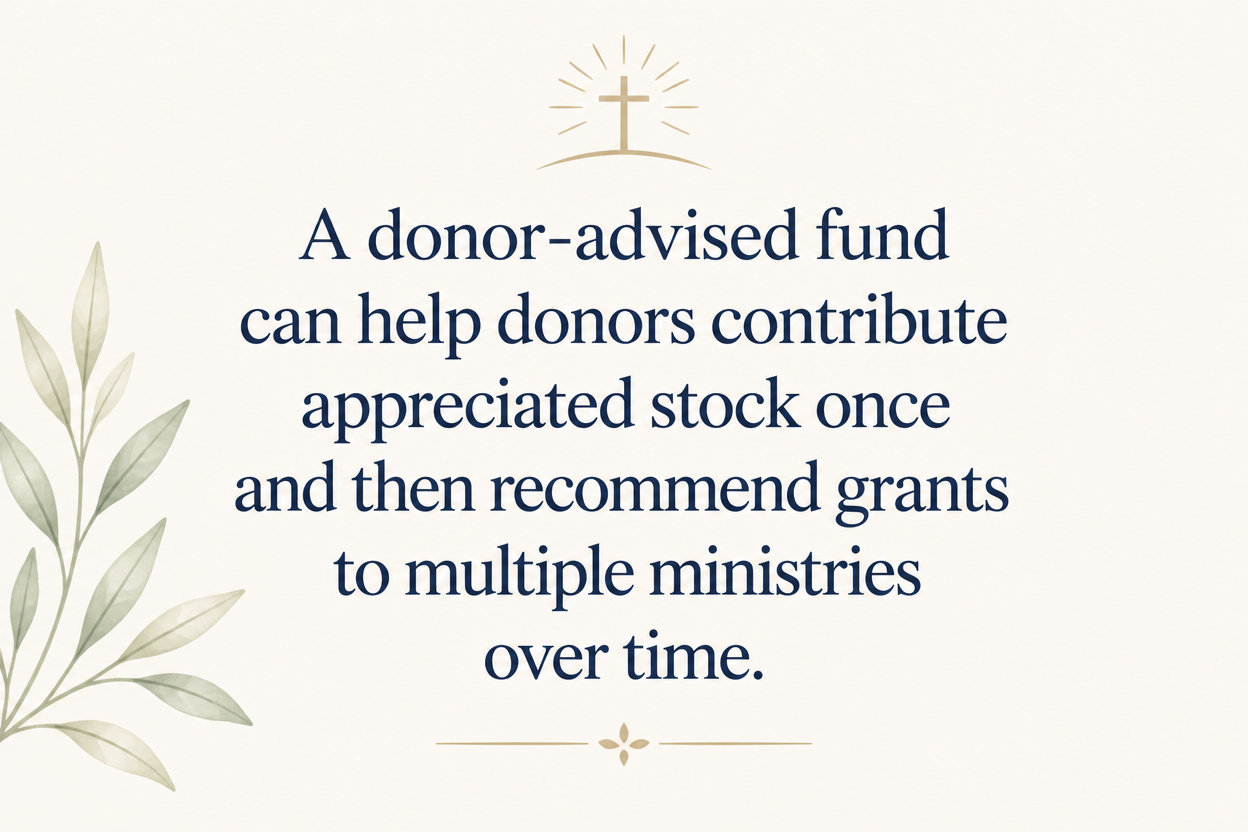

Donor-advised funds and foundations can add flexibility and governance

A donor-advised fund can help donors contribute appreciated stock once and then recommend grants to multiple ministries over time. For some donors, that separation between the investment decision and the grant decision fosters steadier giving and more thoughtful evaluation. Fidelity Charitable provides a plain overview of how donating stock to a donor-advised fund generally works (Fidelity Charitable).

Private foundations introduce additional compliance and administrative responsibilities, but they also offer a structured vehicle for families practicing intergenerational stewardship. The harder question is not which vehicle is “best,” but whether the chosen vehicle supports clarity of purpose, integrity of process, and real generosity toward the church’s mission.

Confirm the ministry can receive stock and that the gift will be used as intended

Ask for the stock transfer instructions and the gift acceptance posture

Before initiating a transfer, donors should ask the ministry for written delivery instructions, the designated contact for brokerage transfers, and the process for acknowledging the gift. Most ministries will sell the shares upon receipt, but some may hold them. That decision should be governed by policy, not by improvisation.

Donors should also ask whether the ministry has any restrictions on the types of securities it can accept. Thinly traded securities, restricted stock, complex privately held shares, and certain alternative assets often require specialized handling. A ministry that accepts such gifts without a clear policy may expose itself to undue risk.

Restricted gifts can honor donor intent but also strain operations

Many donors want to designate gifts for scholarships, curriculum translation, rural pastor training, or church planting residencies. Restrictions can be a faithful way to align resources with calling. They can also unintentionally create fragmentation: staff time spent chasing many small restricted pools, or programs sustained by restricted funds while core infrastructure goes unfunded.

We recommend donors treat restrictions as a covenant rather than a preference. If a donor is not willing to fund the full costs of a designated program—including administration, supervision, safeguarding, and evaluation—the restriction may be unwise. Discipleship ministries, particularly those serving youth, must fund training and safety practices without apology.

Handle the tax and compliance details with the seriousness they deserve

Receipts, valuation, and timing are not minor details

For publicly traded securities, the charity’s receipt should describe the shares and date received, not assign a value. The donor generally determines fair market value under IRS rules and keeps supporting documentation. The IRS addresses substantiation expectations and related requirements in its guidance and publications (IRS Publications).

Timing can be spiritually mundane and practically decisive. Market movement between the initiation of a transfer and the charity’s receipt can change value. Donors who care about year-end giving should begin early enough to avoid brokerage bottlenecks and holiday closures. Ministries that serve donors well will say this plainly and provide a realistic cutoff date for receipt.

Large gifts, complex assets, and appraisal thresholds

Some non-cash gifts require qualified appraisals and additional forms. Donors and ministries should not treat those requirements as nuisances. Proper substantiation protects the donor and reinforces a culture of integrity. For donors making large or complex gifts, a competent CPA or tax attorney is often part of faithful stewardship, not an optional add-on.

Christians sometimes worry that careful tax planning signals divided motives. Scripture does warn against serving money. Yet prudence is not greed; it can be a means of directing more resources to Gospel work. The moral question is not whether donors minimize avoidable taxes within the law. It is whether donors love God and neighbor more than comfort, and whether giving actually increases generosity.

Apply ministry due diligence that fits the nature of discipleship work

Discipleship is measurable, but not always in the way donors want

Some outcomes should be visible: volunteer retention, leader training completion, doctrinal clarity in curriculum, safeguarding compliance, and evidence of local church partnership. Other outcomes are harder: humility, perseverance, repentance, unity, and love of Scripture. Serious ministries resist both extremes—either claiming unverifiable transformation at scale or refusing all measurement in the name of “mystery.”

For donors wanting a wider view of how discipleship ministries vary and what responsible programs look like, we publish sector context and evaluation considerations within Discipleship Ministries.

Use a disciplined set of checks before transferring shares

A stock gift is often larger than an annual check because it draws from accumulated appreciation. That makes pre-gift due diligence proportionately important. A single page of glossy outcomes is rarely sufficient. Donors should ask for primary documents and look for governance and financial signals consistent with long-term trustworthiness. The ministries that meet The Most Trusted Standard tend to treat transparency as a posture: clear financial reporting, accountable leadership, and honest communication about limits.

- Confirm the ministry’s IRS status and legal name match the receiving account.

- Review the most recent audited financials or, if not audited, the latest financial statements and governance disclosures.

- Understand how the ministry defines discipleship and how programs reflect that theology in practice.

- Ask how leaders are trained, supervised, and held accountable, especially in ministry to minors.

- Clarify how the ministry partners with local churches rather than competing for authority and loyalty.

Donors who want a focused view of practical giving decisions—including non-cash gifts—can also consult our coverage under How to Give to Discipleship Ministries.

FAQs for How to give stock to discipleship ministries

Should we give stock directly to the ministry or through a donor-advised fund?

Either can be faithful and effective. Direct stock gifts can be efficient when a ministry has clear transfer instructions and strong receipting practices. A donor-advised fund can add flexibility, help organize giving across multiple ministries, and allow a donor to contribute appreciated stock in a strong market year while distributing grants over time. The better choice is usually the one that supports consistent generosity and careful evaluation, not the one that feels most novel.

What should we ask a discipleship ministry before transferring appreciated shares?

Ask for written transfer instructions, the ministry’s process for acknowledging stock gifts, and whether it sells shares immediately upon receipt. Request current financial reporting and clear explanations of how the ministry defines and evaluates discipleship outcomes. If the gift will be restricted, confirm in writing how the funds will be used and whether the ministry can responsibly carry the administrative burden of that restriction.

Giving stock with confidence

Giving appreciated stock to discipleship ministries can be one of the most practical expressions of Christian stewardship: a legally sound way to reduce tax friction and increase what reaches ministry. The same gift, however, can fund shallow programming if discernment is replaced by sentiment. When donors combine careful mechanics with serious ministry evaluation—grounded in Scripture, attentive to governance, and honest about trade-offs—stock giving becomes not only a financial decision, but a commitment to the patient work of forming disciples who endure.