How Christian donors value non-cash charitable gifts is ultimately a question of stewardship, not merely tax strategy. The church has long understood that generosity includes more than cash, because Scripture presents wealth as a trust to be managed before God, not simply a balance to be spent.

Non-cash giving can be a mature expression of Christian discipleship: releasing appreciated assets, sharing productive property, or funding long-term ministry work without forcing a ministry into short-term fundraising urgency. It can also be a source of confusion and moral hazard when donors, ministries, or advisors treat valuation as a technical loophole rather than a matter of truthfulness and love of neighbor. Christian donors tend to value non-cash gifts well when they can connect the gift to real ministry outcomes, verify integrity, and keep their consciences clear.

Non-cash gifts as stewardship and worship

Scripture frames assets as entrusted, not possessed

Christian giving begins with the doctrine of creation and the confession that all we hold is received. “The earth is the Lord’s and the fullness thereof” (Psalm 24:1). That theological claim has practical force: it relativizes ownership and makes it possible to give away assets that feel “part of us,” such as land held for decades, a closely held business interest, or shares accumulated through disciplined saving.

Non-cash gifts often surface precisely when a donor’s financial life has matured beyond weekly cash-flow giving. Appreciated assets can represent years of patience, risk, and provision. The decision to transfer them to a ministry is frequently experienced as a deeper relinquishment than writing a check, because it involves surrendering future potential and the sense of security attached to it.

Christian donors value integrity over cleverness

The harder question is not whether non-cash gifts are “smart,” but whether they are truthful and rightly ordered. Jesus’ warning that “one’s life does not consist in the abundance of his possessions” (Luke 12:15) presses against a subtle temptation: to treat giving as another way to maximize personal advantage. Tax considerations are legitimate within the law, but they are not morally neutral if they become the primary motive.

For that reason, mature Christian donors tend to value non-cash gifts through two lenses at once: the spiritual lens of worship and the prudential lens of wise administration. When those lenses align, non-cash giving becomes a clean, credible channel for generosity rather than a complicated maneuver that leaves unresolved questions.

Why donors give non-cash assets and what they are trying to protect

Alignment of resources with calling

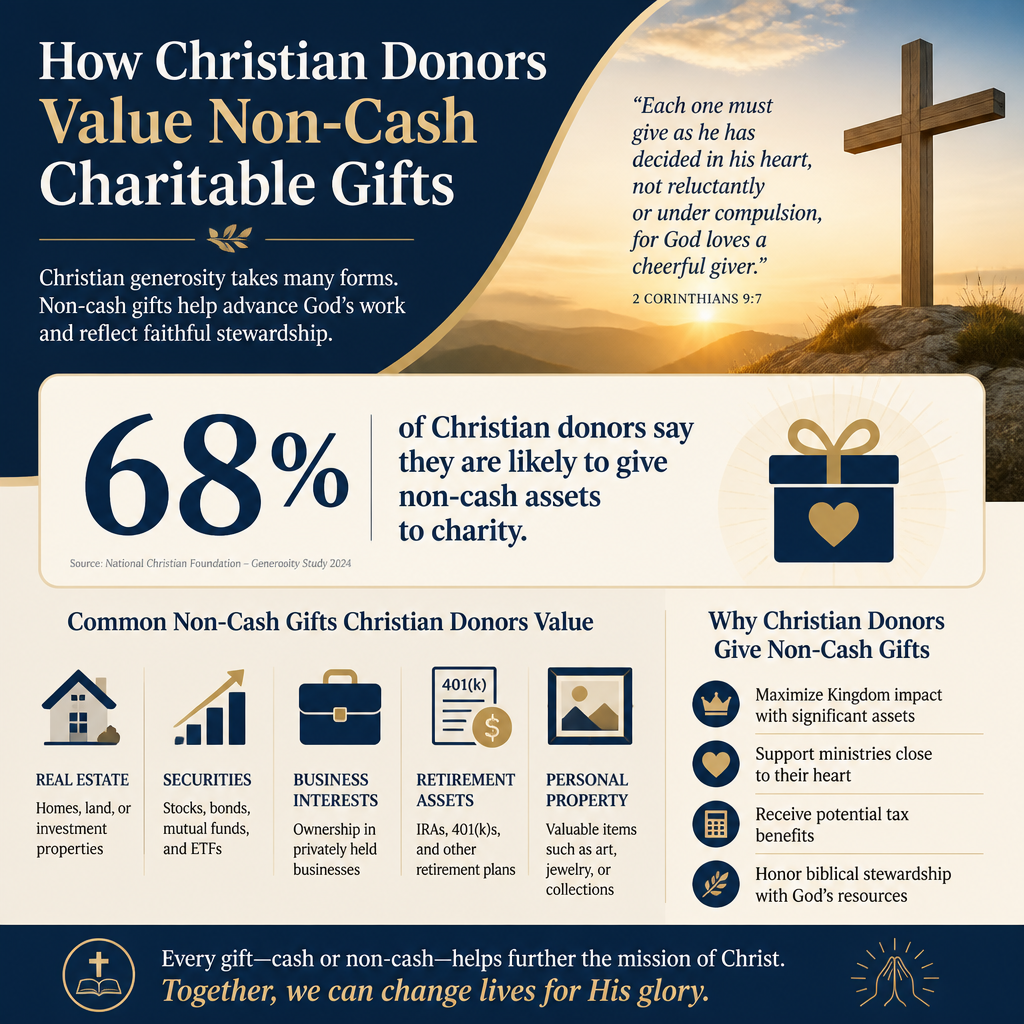

Most donors who consider non-cash gifts are trying to accomplish at least one of three outcomes: give more than they could give from cash on hand, avoid unnecessary erosion of the gift through taxes, or deploy assets in ways that match the time horizon of ministry work. Those are not selfish aims. They are often an attempt to be faithful with the “talents” entrusted to them (Matthew 25:14–30).

In practice, this is why gifts of appreciated securities are common. Selling appreciated stock can trigger capital gains tax; donating shares directly may allow the donor to give the full fair market value while potentially avoiding capital gains on the appreciation, subject to IRS rules and donor-specific circumstances. The IRS outlines the general treatment of charitable contributions and substantiation in IRS guidance.

Protection of conscience and reputation

Christian donors also value non-cash gifts because they are attempting to protect something less visible: moral clarity. Complex gifts can create downstream risk if the ministry cannot manage them, if the valuation is disputed, or if the gift becomes publicly controversial. Few donors want their generosity to create suspicion about the ministry’s governance or their own intent.

Across our verification work at Most Trusted, we find that donors ask better questions when they recognize that non-cash gifts are not simply “assets” but responsibilities. Donors are not only transferring value; they are transferring complexity. The most faithful giving anticipates that transfer and refuses to burden ministries with avoidable risk.

How non-cash gifts are valued and why valuation ethics matter

The practical valuation question

“Value” in non-cash giving has at least three layers. First, there is market value as recognized by accepted valuation methods. Second, there is net realized value to the ministry after liquidation costs, carrying costs, and timing. Third, there is missional value: whether the asset advances ministry work without distorting priorities.

Donors sometimes assume that the headline appraised value is what the ministry “receives.” That can be untrue, especially with real estate, tangible personal property, or unusual assets. The ministry may face brokerage fees, environmental assessments, title issues, storage costs, insurance, or restrictions that reduce what can be realized. A donor who values truthfulness will want the ministry to be able to say, with a clear conscience, what was received and how it was handled.

Appraisals, substantiation, and the donor’s moral duty

Valuation ethics are not a secondary concern; they are part of Christian honesty. The IRS generally requires qualified appraisals for certain non-cash contributions above specified thresholds, and it imposes documentation expectations on donors and organizations. The relevant requirements are described in IRS materials and forms such as Form 8283; donors should consult current rules directly through the IRS and competent advisors.

Christians genuinely disagree about how much weight to place on tax benefits in motivating a gift, but there is broad agreement about truthfulness. Inflated valuations, poorly supported appraisals, or vague descriptions of contributed property can become a form of misrepresentation, even when no one intends fraud. A donor shaped by Scripture will care about avoiding both wrongdoing and the appearance of wrongdoing, not to protect a brand, but to honor the God of truth.

What ministries need from donors when receiving non-cash gifts

Capacity, policy, and governance

Not every Christian nonprofit should accept every kind of non-cash gift. A ministry that receives a property it cannot insure, maintain, or liquidate may be diverted from its calling. Wise boards adopt gift acceptance policies, define who can approve complex gifts, and ensure the organization can evaluate restrictions and risks before accepting them.

We recommend that donors treat a ministry’s readiness as a core part of “value.” The best non-cash gift is not the one with the largest appraised number; it is the one that a ministry can steward transparently, in a timely way, under competent governance. When donors want a clearer view of how ministries approach these questions across governance, financial integrity, faith commitments, and public transparency, the broader context of Christian Stewardship Services can be a useful starting point.

The donor’s role in preventing friction and confusion

Non-cash gifts often fail not because of bad intent but because of mismatched expectations. Donors can prevent avoidable friction by clarifying timing, restrictions, and costs before a transfer is initiated. In many cases, the ministry’s finance team and the donor’s advisor simply need to coordinate early.

A short set of donor-side practices tends to improve outcomes materially:

-

Ask the ministry whether it has a written gift acceptance policy and who has authority to approve complex gifts.

-

Clarify whether the ministry intends to liquidate the asset immediately or hold it, and how that decision is governed.

-

Confirm what documentation the ministry will provide and what the donor must retain for substantiation.

-

Discuss any restrictions in writing, with attention to whether they could constrain ministry work.

-

Anticipate transaction costs and timelines so the ministry is not forced into a hasty sale.

Verification and confidence when gifts are complex

Why trust becomes more important as the gift becomes less liquid

Cash gifts are straightforward: the ministry receives dollars and can usually deploy them quickly. Non-cash gifts introduce more decision points and therefore more opportunities for mismanagement, misunderstanding, or reputational harm. The donor’s need for confidence rises as liquidity falls.

This is one reason independent verification can matter. Most Trusted exists to help donors give with confidence by evaluating Christian nonprofits against The Most Trusted Standard, a 15-criteria framework across faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. Verification does not eliminate risk, but it can narrow the field to ministries that demonstrate disciplined stewardship practices and public accountability.

Acknowledging real tensions without retreating into cynicism

The field has had to reckon with legitimate questions about nonprofit reporting and donor expectations. The “Overhead Myth” conversation, for example, pushed donors to stop treating low administrative costs as a standalone indicator of effectiveness; the original letter was advanced by organizations including GuideStar (now Candid) and Charity Navigator. Candid maintains resources on nonprofit financial interpretation through Candid. The same principle applies to non-cash gifts: simplistic heuristics will not serve donors well.

At the same time, complexity is not an excuse for opacity. Donors are right to expect ministries to explain how non-cash gifts are received, recorded, liquidated, and reported. The ministries that meet The Most Trusted Standard tend to treat transparency as part of discipleship: not performative disclosure, but clear reporting that helps the church give with informed confidence. For donors specifically focused on gift types beyond cash, Non-Cash Giving Through Christian Stewardship Services is a natural place to continue.

FAQs for How Christian donors value non-cash charitable gifts

What non-cash gifts do Christian donors give most often?

Common non-cash gifts include appreciated publicly traded securities, real estate, vehicles, and sometimes closely held business interests. Donors often begin with appreciated securities because transfer and liquidation are typically straightforward for both donor and ministry, while real estate and business interests require greater due diligence, clear governance approval, and careful documentation.

How should we evaluate whether a ministry can handle a complex non-cash gift?

We recommend looking for a written gift acceptance policy, board-level oversight for complex gifts, evidence of competent financial reporting, and a track record of transparent communication with donors. Independent verification can also reduce uncertainty by assessing whether the organization’s governance, financial integrity, and transparency practices are consistent and publicly demonstrable.

Valuing non-cash gifts with sober faithfulness

Christian donors value non-cash charitable gifts well when they treat them as a form of worship governed by truthfulness and love, not as an exercise in financial cleverness. The goal is not to avoid complexity but to steward it: to give assets in ways a ministry can manage, to document valuations honestly, and to support organizations whose governance and transparency can bear the weight of significant gifts. Done with integrity, non-cash giving can strengthen the church’s witness and fund durable work that cash alone often cannot sustain.