How Christian donors give stock to ministries is usually presented as a tax tactic. That framing is incomplete. For Christians who want giving to be both generous and wise, donating appreciated securities is a way to convert God’s provision into ministry impact without incurring avoidable friction for either the donor or the ministry.

The question is not whether stock gifts are legitimate—they are a well-established charitable method in U.S. law—but whether the gift will be handled with integrity, receipted correctly, and directed to a ministry whose doctrine, governance, and financial practices can bear scrutiny. Mature stewardship does not separate the spiritual from the administrative; Scripture regularly holds them together (Luke 16:10–12).

Why stock is often a better gift than cash for mature givers

Appreciated assets can enlarge the gift without enlarging the tax bill

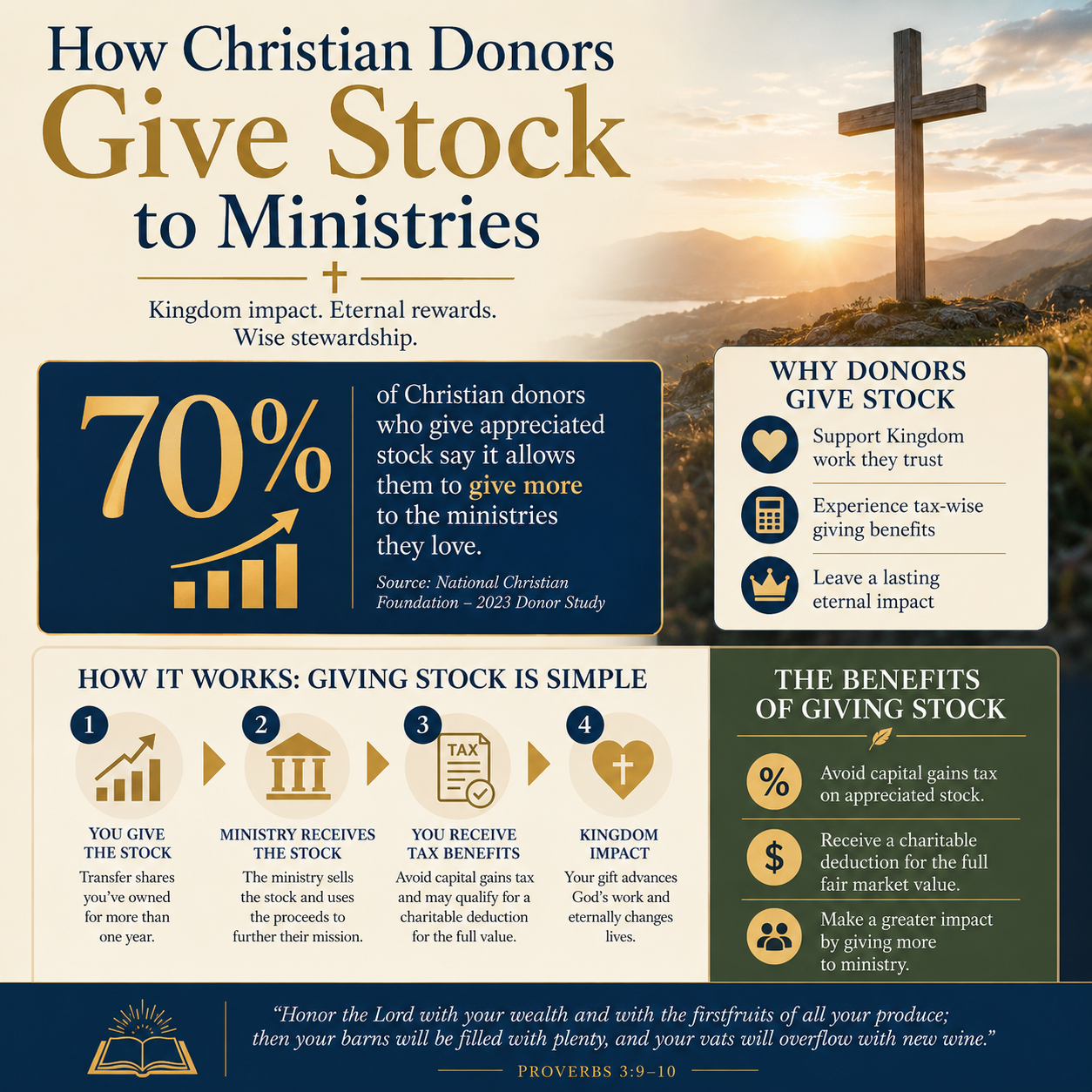

When a donor gives long-term appreciated stock directly to a qualified charity, the donor generally may deduct the fair market value and avoid paying capital gains tax on the appreciation, subject to IRS rules and limitations. This is not a loophole. It is a policy choice designed to encourage charitable giving, and it can allow a donor’s generosity to be expressed in fuller measure.

For donors who are already giving generously, the difference between “sell and give cash” and “give the shares” can be significant, especially after years of compounding. The IRS sets the governing definitions for long-term capital gain property and charitable contributions of appreciated securities, and donors should ground decisions in those primary sources rather than in hearsay from fundraising materials. See the IRS discussion of charitable contributions and substantiation requirements at IRS.gov.

Non-cash giving can align with how many donors actually hold wealth

Many Christian households build a meaningful portion of net worth in brokerage accounts rather than in checking accounts. The United States has tens of millions of shareholder accounts, which makes securities a mainstream asset class for households, not a niche tool for the ultra-wealthy. The Federal Reserve’s public reporting on household balance sheets helps illustrate how common financial assets have become over time; see FederalReserve.gov.

What this means in practice is that a donor may have both the desire to give and the financial capacity to give—yet feel “cash constrained.” Stock gifts often resolve that tension. They allow a donor to give from abundance without triggering the psychological and practical constraints of cash-flow.

The process ministries use to receive stock and what donors should expect

The standard transfer mechanics and why timing matters

Most ministries do not “receive stock” in the sense of holding and managing an investment portfolio. They typically receive shares into a brokerage account (often through a custodian) and then liquidate promptly according to a board-approved gift acceptance policy. The donor initiates the transfer from a brokerage account using DTC instructions supplied by the ministry (or the ministry’s receiving broker).

Timing matters because the date of gift for publicly traded securities is generally tied to when the charity receives control of the shares, not when the donor clicks “submit” at a brokerage. Donors who plan year-end gifts should build in time for processing delays, particularly in late December when brokerages and ministries experience heavy volume.

Receipting should be clean, accurate, and appropriately limited

Christian donors should expect a contemporaneous written acknowledgment that describes the non-cash gift without assigning a dollar value. Assigning value is the donor’s responsibility. Ministries that state a valuation on the receipt may create complications for the donor’s tax substantiation. The IRS publishes clear rules for non-cash charitable contributions and acknowledgments; donors can review the governing expectations at IRS.gov.

A serious ministry will also avoid language that implies a quid pro quo benefit. If a donor receives a benefit (a dinner, a product, a conference registration), it must be handled with clarity. Mature ministries treat receipting as an aspect of truthfulness, not as a fundraising afterthought.

Governance and integrity questions donors should ask before giving stock

Stock gifts expose weaknesses that cash gifts can conceal

Securities gifts require coordination: donor intent, ministry policy, broker instructions, internal controls, and prompt liquidation procedures. That coordination reveals whether a ministry has basic operational competence and oversight. If a ministry cannot provide clear transfer instructions, explain how gifts are processed, or issue proper acknowledgments, donors should pause. The issue is not sophistication; it is stewardship.

Across our verification work at Most Trusted, we observe that ministries meeting The Most Trusted Standard tend to treat non-cash giving as part of a larger integrity ecosystem: documented policies, functioning boards, segregation of duties where feasible, and clear public communication. Those practices do not guarantee fruitfulness, but they do reduce preventable risk.

The harder question is whether the ministry is worthy of concentrated trust

Stock giving often represents a donor’s most significant gifts. Concentrated giving demands concentrated due diligence. Christians genuinely disagree about how much scrutiny is appropriate—some worry that “analysis” erodes faith, while others see investigation as a moral duty toward the widow’s mite and the reputation of the gospel. Scripture commends both generosity and prudence (Prov. 21:5), and mature donors can hold them together without embarrassment.

Due diligence should not stop at overhead ratios or a charismatic founder’s story. It should include doctrinal clarity, board independence, conflict-of-interest management, audited financials when appropriate to size, and transparent reporting of outcomes and limits. For donors who want a coherent framework for this work, our coverage of Christian Stewardship Services addresses the stewardship questions that recur across ministry categories.

Practical steps for donors and ministries to execute a stock gift well

A disciplined workflow prevents most avoidable mistakes

Donors sometimes assume stock gifts are complicated. In practice, the complexity is manageable if both sides treat the transfer as a formal transaction, not a casual exchange. We recommend a short pre-transfer confirmation by email with the ministry (or its giving partner) to ensure the correct instructions and to clarify how the gift will be acknowledged.

- Confirm the ministry is a qualified 501(c)(3) and can receive securities.

- Request current DTC instructions and the correct account name and number.

- Clarify whether the ministry liquidates immediately and whether it accepts restricted gifts.

- Initiate the transfer through the brokerage and retain the confirmation.

- Wait for the ministry’s acknowledgment letter describing the shares received and the date.

Donors should also coordinate with a tax professional when gifts are large or when multiple lots are involved. The question is not only “Can we deduct this?” but “What is the most faithful and lawful way to document this gift so that the ministry and the donor are protected?”

Restricted gifts require particular care

Some donors want to designate a stock gift to a specific project. Designations can be appropriate, but restrictions can create operational strain or even legal complications if the restriction is drafted as a binding limitation rather than as a preference. Ministries should have a gift acceptance policy that defines what restrictions they will and will not accept, and donors should honor that boundary.

Wise donors also recognize that over-restriction can unintentionally distort a ministry’s priorities. The Starvation Cycle described by Gregory and Howard highlights how donor pressure can drive organizations toward underinvestment in administration and capacity, which can harm long-term effectiveness; see Stanford Social Innovation Review. Christian donors are not exempt from these dynamics, even when motives are sincere.

How verification strengthens confidence in non-cash giving

Non-cash giving magnifies both impact and risk

Stock gifts can accelerate kingdom work. They can also magnify the cost of misplaced trust. A large stock gift directed to a ministry with weak governance, unclear theology, or opaque reporting can unintentionally subsidize confusion and disorder. The goal is not risk elimination—Christian giving is an act of faith—but risk alignment, where the donor’s confidence is proportionate to the ministry’s demonstrated trustworthiness.

Most Trusted exists because donors deserve more than marketing claims. We evaluate ministries against The Most Trusted Standard, a 15-criteria framework that examines faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. Verification does not replace prayer, pastoral counsel, or personal discernment, but it does supply a disciplined way to test what is verifiable.

Donors can pair generosity with accountability without cynicism

Christians are rightly wary of a posture that treats every ministry as suspect. The answer is not naïveté on one side or cynicism on the other. It is charitable seriousness: honoring faithful laborers while insisting on practices that protect donors, beneficiaries, staff, and the witness of the Church.

For donors considering a stock gift in particular, the relevant category questions often overlap with other non-cash strategies—real estate, donor-advised funds, complex assets, and planned giving. Our coverage of Non-Cash Giving Through Christian Stewardship Services addresses how these approaches intersect with governance, receipting, and ministry readiness.

FAQs for How Christian donors give stock to ministries

Should we sell the stock and give cash, or donate the shares directly?

When the shares have appreciated and have been held long-term, donating the shares directly is often more tax-efficient because the donor may avoid capital gains tax and may be eligible to deduct fair market value, subject to IRS rules and limitations. The right answer depends on the donor’s tax situation, the kind of asset, and whether the ministry can receive securities. Donors should confirm the governing requirements and substantiation expectations at IRS.gov and coordinate with a qualified tax advisor.

What receipt should we expect from the ministry for a stock gift?

The acknowledgment should describe the donated property (for example, the name of the security and the number of shares) and the date the ministry received it. It should not state a dollar value. If goods or services were provided in exchange, the receipt should disclose that and provide a good-faith estimate of value. These are not optional best practices; they are part of lawful substantiation and basic honesty in communication.

A faithful stock gift is both generous and well-governed

Christian donors give stock to ministries most wisely when the method serves the substance: converting appreciated assets into durable kingdom impact under clear governance and truthful reporting. A ministry that cannot handle securities with competence may also mishandle other forms of trust. A ministry that can receive, receipt, and deploy a stock gift with clarity often signals a broader pattern of integrity.

The aim is not to make giving clinical. It is to make giving credible—so that generosity is strengthened, the vulnerable are protected, and the name of Christ is not associated with avoidable disorder.