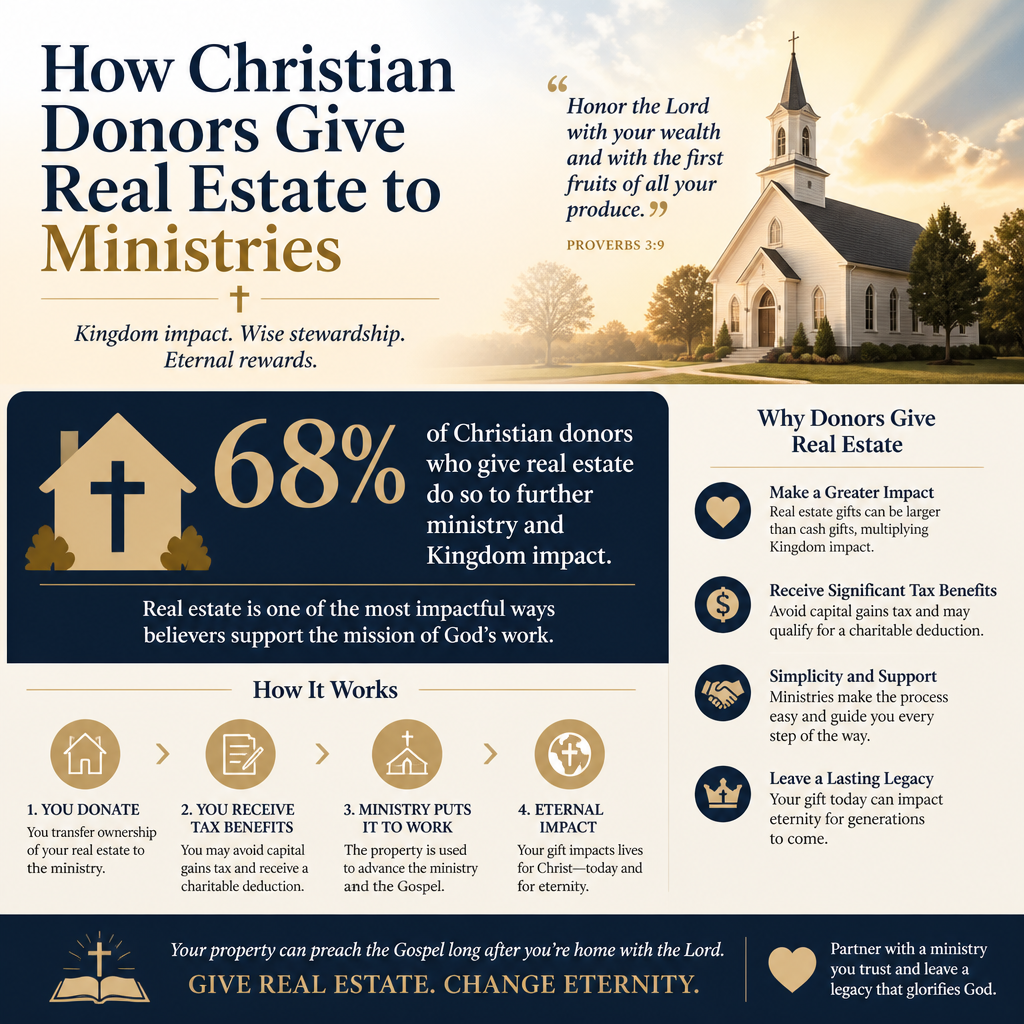

How Christian donors give real estate to ministries is rarely a simple transfer of property. Real estate is often a family asset, a tax-sensitive asset, and a spiritually weighty asset all at once. Many donors arrive with a clear desire to support kingdom work, yet also with understandable questions: Will the ministry handle this responsibly, will it create unintended burdens, and will the gift accomplish what we intend?

Scripture treats property as meaningful stewardship, not as a neutral possession. Land and homes can be sources of security, temptation, hospitality, and provision for the vulnerable. When Christians consider giving real estate, the question is not only “Can we donate this?” but “What form of gift best serves the mission, protects the integrity of the ministry, and honors the claims of prudence and love of neighbor?”

Real estate giving is spiritual stewardship and operational risk

Why ministries do not treat property like cash

Cash is immediately usable; real estate is not. A donated house may require repairs, insurance, property taxes, security, and ongoing maintenance. If the property is occupied, there may be landlord responsibilities, tenant protections, eviction constraints, or local housing codes. A piece of land may have access issues, encroachments, water rights, or restrictions that materially affect value and saleability.

For donors, these are not merely technical concerns. They are issues of faithful stewardship. Proverbs commends wisdom and counsel, not impulsiveness. A gift that burdens a ministry with unplanned carrying costs can harm the very work the donor aims to strengthen.

What we observe across verification work

Across our verification work at Most Trusted, we observe that ministries with strong internal controls tend to treat non-cash gifts as a governance matter, not only a fundraising matter. They define what kinds of real estate they can accept, how they will value it for accounting purposes, what conflicts of interest must be avoided, and who must approve an exception. Those patterns are consistent with the basic instincts behind The Most Trusted Standard: clarity of mission, financial integrity, accountable leadership, and transparent communication with donors.

For donors, this means the responsible ministry is often the one that is willing to say “no” to certain properties, or “yes, but only under defined conditions,” rather than accepting every gift that appears generous.

The primary ways Christian donors give real estate to ministries

Outright gifts, bargain sales, and retained life estates

Most real estate gifts fall into a small set of structures. The right structure depends on the donor’s goals, the property’s condition, the ministry’s capacity, and the donor’s need for liquidity or ongoing use.

- Outright gift: the donor transfers full ownership to the ministry. The ministry typically sells the property and uses proceeds for mission.

- Bargain sale: the donor sells the property to the ministry for less than fair market value, combining a partial sale with a partial charitable gift.

- Retained life estate: the donor gives the property now but retains the right to live in it for life (or for a term of years), with the ministry receiving the property later.

- Gift of an undivided interest: the donor gives a percentage interest in a property, sometimes over time.

- Gift through an entity: the property is held in an LLC, partnership, or trust, and the donor gives the interest, which introduces additional complexity.

These structures can be lawful and wise. They can also be misused when donors are pressured, when the property is hard to sell, or when the ministry’s leadership lacks clarity about obligations being accepted.

Be alert to the distinction between giving and underwriting

Some properties function less like a donation and more like an ongoing project. A ministry may be offered a building that requires major rehabilitation or a parcel that needs zoning changes. At that point, a “gift” can quietly become an expectation that the ministry will fund development. For donors, the moral question is not whether a ministry can accept a challenging asset, but whether doing so is consistent with its mission and fiduciary responsibilities.

Christians genuinely disagree about how much risk is appropriate in faith-driven work. Yet there is a clear difference between faith and presumption. Responsible real estate giving names the costs and constraints in advance.

Due diligence that honors the ministry and the donor

What donors should ask before offering property

Real estate carries legal and environmental liabilities that can follow the owner. A ministry that accepts a property may inherit problems it did not create. Donors can serve ministries well by offering full documentation early and welcoming sober evaluation rather than viewing questions as a lack of gratitude.

Before presenting a property, donors should be ready to discuss title status, mortgage balances, liens, recent inspections, known defects, insurance claims history, and any unusual restrictions. If the property is used commercially or has a long history of industrial activity nearby, environmental assessment may be required. The U.S. Environmental Protection Agency notes that property owners can face liability under certain environmental circumstances, which is one reason nonprofits often require environmental due diligence before acceptance. U.S. Environmental Protection Agency

What a well-governed ministry typically requires

Many ministries maintain a formal gift acceptance policy, often reviewed by legal counsel and approved by the board. Policies commonly specify the appraisal standards the donor must meet, the documents required for review, and the circumstances under which the ministry will decline. The Internal Revenue Service is explicit that for noncash charitable contributions above certain thresholds, donors must follow defined substantiation and appraisal requirements. Internal Revenue Service

These requirements are not bureaucratic obstacles; they are protections. They help ensure that donors receive accurate tax documentation, that ministries avoid misstatements in financial reporting, and that the gift does not become a source of future conflict.

Donors who want a broader view of this discipline across non-cash assets often find it useful to review Non-Cash Giving Through Christian Stewardship Services as a category of practices, not a single transaction type.

Tax and valuation realities that deserve clarity

Qualified appraisals and credible valuations

Real estate giving often hinges on valuation. Fair market value is not merely a number that benefits the donor; it is a number that can distort a ministry’s reporting if it is not credible. Mature ministries typically insist on donor compliance with IRS substantiation rules and refuse to “coach” donors into aggressive valuations.

The IRS guidance for charitable contributions establishes the expectation that donors obtain qualified appraisals for certain noncash gifts and complete the appropriate forms. When donors treat these steps as optional, they expose themselves to penalties and create reputational risk for the ministry. IRS Publication 526

The tension between tax benefits and spiritual motive

Tax benefits can be a legitimate secondary good. Yet Christians should be cautious about allowing tax strategy to become the functional driver of generosity. Jesus warned about the spiritual hazards of wealth precisely because money and assets have a way of quietly taking the place of trust in God. A mature posture is neither guilt about tax planning nor indifference to motive. It is clarity: the gift serves the mission first, and the tax consequences are addressed honestly and lawfully.

Some donors also consider how appreciated real estate compares to giving cash from income. In many cases, giving an appreciated asset can be more efficient than selling it and giving the proceeds, but the details depend on basis, holding period, and the donor’s broader situation. Ministries should not provide individualized tax advice, and donors should insist on their own qualified counsel.

Choosing ministries that can steward property with integrity

Why governance and transparency matter more with real estate

Real estate can create conflicts of interest: a board member who is also a realtor, a donor who wants a relative hired to renovate the property, a leadership team tempted to expand beyond mission because a building “appeared.” These pressures are not theoretical. They are common across the nonprofit sector, and they can be especially acute in Christian work where relational trust can be high and oversight can be informal.

For that reason, we recommend treating real estate gifts as a moment to evaluate institutional maturity. Does the ministry have clear governance practices? Does it disclose related-party transactions? Does it report financial statements in a way that is intelligible to donors? Does it communicate how proceeds from asset sales will be used?

Most Trusted exists to help donors answer those questions without cynicism. Our evaluation work applies The Most Trusted Standard to ministries so donors can give with confidence, especially when the gift is complex and irreversible.

Signals of a ministry prepared to accept real estate

Donors should look for evidence, not assurances. A prepared ministry can usually explain, in plain terms, who approves property acceptance, how it handles valuation and disposition, and how it will communicate outcomes to donors. It will also be clear about when it cannot accept a property.

Donors engaging real estate giving as part of a broader stewardship posture may also benefit from reviewing Christian Stewardship Services, since real estate decisions often intersect with estate planning, non-cash assets, and long-term generosity.

FAQs for How Christian donors give real estate to ministries

Should we offer a ministry a property before we have an appraisal?

In many cases, yes. A donor can begin with a conversation and a basic description of the property, then proceed to appraisal and formal documentation once the ministry indicates it is open to review. Ministries often need preliminary information first because their acceptance decision may depend on location, condition, liens, or use restrictions, not only on value. For tax reporting, however, donors should expect to obtain a qualified appraisal when IRS rules require it and to follow substantiation requirements carefully.

What if the ministry says it will accept the property only if it can sell it quickly?

That condition is often prudent. A ministry may not be called or equipped to hold real estate, assume landlord responsibilities, or carry ongoing costs. A quick-sale condition signals that leadership is thinking about mission focus and fiduciary duty. Donors should ask what the ministry’s plan is for marketing and disposition, what carrying costs could be incurred, and how proceeds will be directed to the ministry’s stated purposes.

Real estate gifts are strongest when they are both generous and governable

Real estate can become one of the most consequential gifts a Christian donor makes, not only because of value, but because it requires deliberate trust and careful moral reasoning. The best outcomes tend to occur when donors pursue generosity without sentimentality, and when ministries receive gifts with gratitude and disciplined governance. That combination honors the donor’s intent, protects the ministry’s mission, and reflects stewardship that is worthy of the gospel we profess.