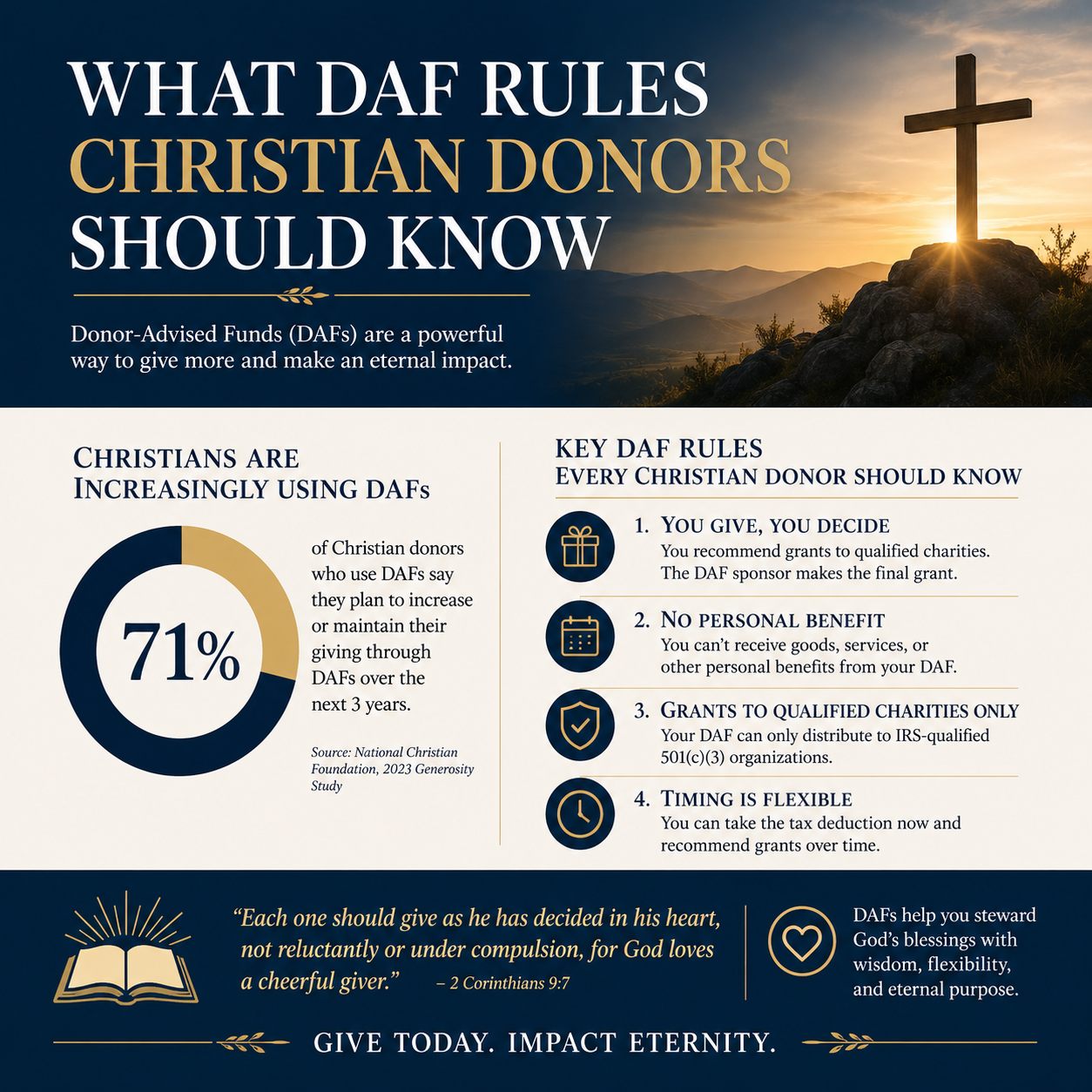

DAF rules Christian donors should know are not merely technical constraints; they shape whether our giving remains both faithful and accountable. Donor-advised funds can serve wise stewardship, but they also create blind spots if we treat them as private accounts rather than charitable assets held for the Lord’s purposes.

Scripture consistently frames wealth as entrusted, not possessed. “It is required of stewards that they be found faithful” (1 Corinthians 4:2). Fidelity in giving includes understanding the guardrails that govern a DAF, especially where tax law, ministry integrity, and public trust intersect.

1 DAFs are charitable accounts with real legal boundaries

A DAF is a completed charitable gift not a temporary parking place

When we contribute to a donor-advised fund, the receiving sponsor becomes the legal owner of the assets. We retain advisory privileges, not control. That distinction matters because some donors, often unintentionally, speak and act as if the DAF is still “our money” awaiting deployment. Legally and ethically, it is already a charitable gift held by a public charity and governed accordingly.

The Internal Revenue Service describes a donor-advised fund as a fund “separately identified by reference to contributions of a donor or donors” where the donor may advise on distributions and investments, but the sponsoring organization maintains “legal control.” IRS Donor-Advised Funds

The sponsor’s policies are part of the rules

Beyond federal law, each DAF sponsor sets policies that affect how recommendations are evaluated: whether international grants are permitted, how due diligence is conducted, and what documentation a ministry must provide. Some sponsors are permissive; others are careful to a fault. Neither posture is neutral. A permissive sponsor may expose donors to greater risk of funding problematic work; an overly restrictive sponsor may impede responsive generosity in crisis contexts. Mature stewardship accounts for both dimensions.

2 The tax deduction is tied to timing and to the type of asset

Deduction timing follows the contribution not the grant

One of the most common misunderstandings is assuming the deduction follows the grant to a ministry. Under DAF rules, the deduction generally occurs when we contribute to the DAF sponsor, not when grants are later made from the DAF. That can be strategically helpful for bunching gifts in high-income years, but it also creates a spiritual temptation: feeling “finished” with generosity because the tax event is complete, even if the funds have not been sent to active ministry.

In practice, this means we should build a granting plan at the same time we make the contribution, even if distributions will be staged. Otherwise, the DAF can drift toward indefinite accumulation, which may satisfy financial preferences while neglecting the Church’s call to meet pressing needs.

Asset type affects valuation and deductibility

DAFs are often used to give appreciated assets such as publicly traded stock. That can increase giving capacity by avoiding capital gains taxes and allowing a charitable deduction subject to applicable limits. The limits vary by asset type and by whether the charity is a public charity, a private foundation, or a DAF sponsor. Because these rules are detailed and fact-dependent, we recommend donors coordinate with qualified tax counsel.

The IRS provides the governing framework for charitable contribution deductions, including limitations and valuation rules. IRS Charitable Contributions

3 Some recommendations are prohibited and the penalties can be severe

You cannot recommend grants that provide more than incidental benefit

DAF rules restrict grants that provide a more than incidental benefit to the donor, the donor’s family, or entities controlled by the donor. This is where many well-intentioned Christians stumble. We may want to pay for a table at a gala, buy an auction item, cover the cost of a mission trip participant, or fulfill a pledge. Those are common practices in church and ministry culture, but in a DAF context they can create prohibited benefits or prohibited transactions.

Congress sharpened these boundaries in the Taxpayer Certainty and Disaster Tax Relief Act of 2019, which generally disallows using a DAF to pay for a charity event ticket or other benefit, even if the donor intends to waive the benefit. Congress HR 1865

Pledge payments and certain tuition related grants require special care

Christians genuinely disagree about the best way to formalize commitments to a ministry. Some ministries request written pledges for budgeting stability; some donors prefer informal commitments. Under DAF rules, paying a personal pledge from a DAF can be problematic because the pledge is considered a personal obligation. Many DAF sponsors will not process such grants, and donors should not pressure them to do so.

Similarly, grants connected to tuition, membership dues, or benefits tied to an individual often implicate prohibited benefits. There are legitimate ways to support Christian education and discipleship, but a DAF is not always the right vehicle. When the line is unclear, the faithful path is to slow down, ask for the sponsor’s written policy, and consult counsel rather than forcing an edge case through a system built for public accountability.

4 Due diligence is not optional if we want giving that honors Christ

DAF sponsors screen for compliance not for ministry credibility

A DAF sponsor’s compliance checks usually confirm that an organization is a qualified public charity and that the grant will be used for charitable purposes. That is necessary, but it is not the same as assessing whether a ministry is governed well, financially truthful, and spiritually grounded. Many Christian donors assume that because a grant is “approved,” the recipient has been vetted for integrity. That assumption is unwarranted.

This is one reason Most Trusted exists. Across our verification work, we observe that mature ministries welcome scrutiny: clear financial reporting, an accountable board, conflict-of-interest discipline, and transparent claims about outcomes. The ministries that meet The Most Trusted Standard tend to treat donor trust as a stewardship obligation, not a marketing problem. When we pair DAF convenience with serious verification, we reduce the likelihood that good intentions will fund manipulation, exaggeration, or governance failure.

What to check before recommending a grant

Donors do not need to become forensic accountants to practice responsible stewardship, but we should insist on a baseline of verifiable integrity. A practical short list is often enough to surface meaningful issues:

- Clear statement of faith and evidence it actually governs decisions

- Recent audited financials or reviewed statements when scale warrants

- Board independence and documented conflict-of-interest policy

- Transparent fundraising practices and truthful impact reporting

- Clarity on whether funds are restricted and how restrictions are honored

For donors building a repeatable process, Christian Stewardship Services offers a helpful context for how disciplined giving practices can be integrated with the tools donors already use.

5 Grantmaking discipline protects both witness and conscience

DAFs can unintentionally distance donors from the spiritual weight of giving

There is a quiet moral hazard in any system that makes generosity frictionless. A DAF can make giving as easy as clicking a button. That convenience is not evil; it can be a mercy in seasons of complexity. But it can also reduce giving to a transactional workflow rather than an act of worship that requires attention, prayer, and accountability.

Scripture’s warnings about money are often warnings about self-deception. We can appear generous while remaining fundamentally self-protective. A DAF structure can intensify that risk if it becomes a place to warehouse charitable assets indefinitely. The harder question is not whether we are “allowed” to keep funds in a DAF, but whether our granting pace and priorities reflect love of neighbor, confidence in God’s provision, and sober awareness of urgent need.

Grantmaking practices that fit Christian donors

Many donors want their giving to be both strategic and relational: aligned with convictions, responsive to needs, and accountable to truth. A few disciplines tend to serve that aim well.

First, establish a granting cadence. Some donors recommend grants quarterly; others align with ministry budgeting cycles. Second, differentiate between core commitments and responsive giving so that emergency appeals do not erode long-term faithfulness. Third, keep documentation of restrictions and correspondence, especially when grants are intended for specific programs. Fourth, periodically review whether the ministries we fund still exhibit the doctrinal clarity, governance strength, and transparency that justified trust in the first place.

Donors who want to understand operational realities of DAF administration in Christian contexts will find additional perspective in How Christian Stewardship Services Manage Donor-Advised Funds, including common decision points where donors benefit from clearer rules and stronger guardrails.

FAQs for What DAF rules Christian donors should know

Can we use a DAF to pay for a gala table or event ticket if we decline the dinner?

Generally no. DAF rules restrict grants that provide a more than incidental benefit to the donor. Federal law has clarified that using a DAF to pay for the charitable portion of an event ticket is generally not permitted, even if the donor intends to waive the benefit. The prudent approach is to pay event benefits personally and use the DAF only for amounts that confer no donor benefit, consistent with the sponsor’s written policy. Congress HR 1865

Can a DAF make a grant to a church or explicitly Christian ministry?

Yes, if the recipient is a qualified organization and the grant is for charitable purposes. Most churches qualify as tax-exempt charities, but some do not appear in the IRS searchable database because churches are not required to apply for recognition in the same way other charities are. DAF sponsors often have their own verification process for churches, and they may request documentation. The controlling principle is that the sponsor must maintain legal control and ensure the grant is used for charitable purposes. IRS Donor-Advised Funds

Stewardship worthy of the gift

DAF rules can feel like bureaucratic limits, but they exist because charitable assets are meant to serve the public good and to be handled with integrity. For Christian donors, the standard is higher than compliance. Our giving should be truthful, accountable, and aimed at love of neighbor, with a conscience trained by Scripture and a practice shaped by verifiable evidence. When a DAF is used within its rules and paired with disciplined ministry verification, it can support generosity that is both free and faithful.