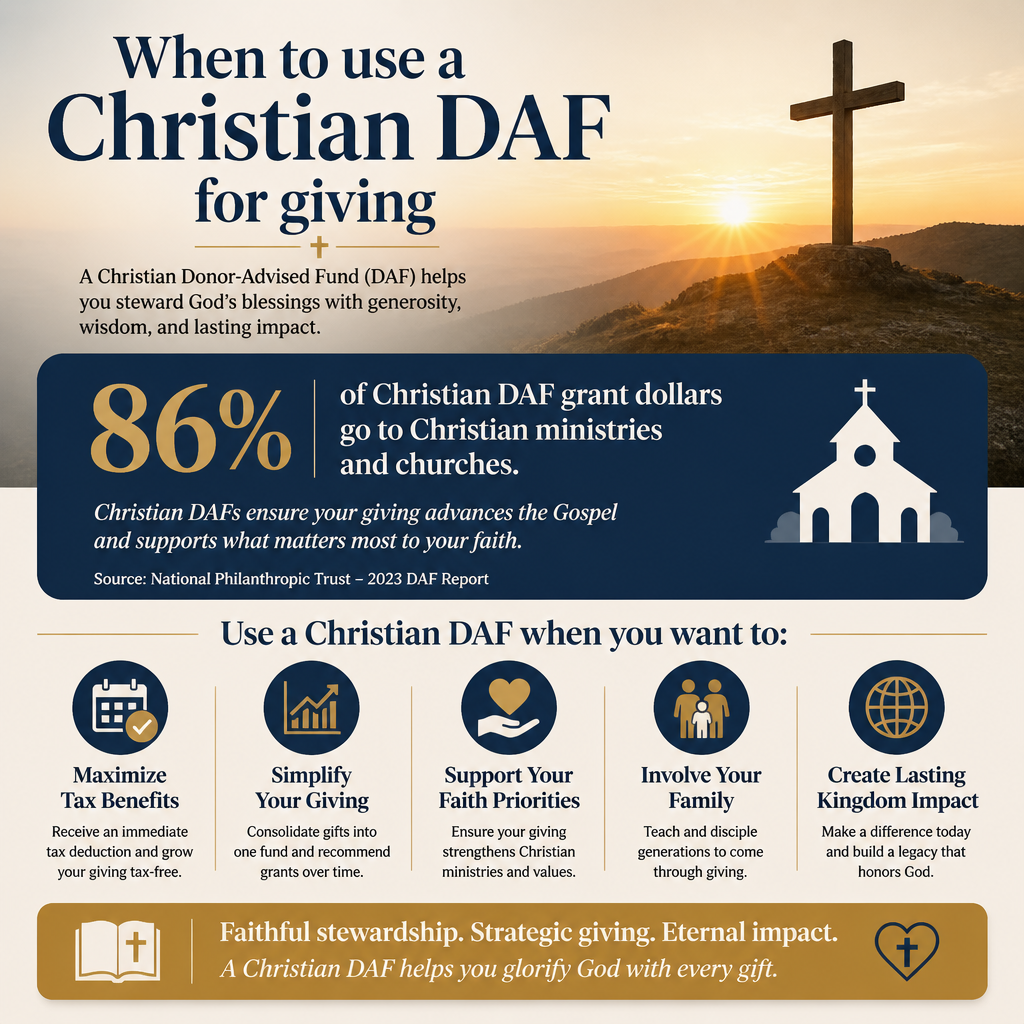

When to use a Christian DAF for giving is ultimately a stewardship question: how to structure generosity so that it is both spiritually intentional and administratively faithful. A donor-advised fund can strengthen long-term giving, but it can also introduce distance between donor and ministry if it becomes merely a tax mechanism rather than a discipline of worshipful generosity.

Scripture does not prescribe modern charitable vehicles, but it does insist on integrity, foresight, and love of neighbor. Jesus’ warnings about wealth are not mainly about accounting. They are about the spiritual gravity of money and the danger of confusing righteous means with righteous ends. A Christian DAF is best used when it helps a donor give more freely, more wisely, and more consistently—without diminishing accountability or the donor’s responsibility to know what they are supporting.

A Christian DAF is a tool for committed giving, not a substitute for discernment

What a DAF does well

A donor-advised fund allows a donor to make an irrevocable charitable contribution, receive a tax deduction (subject to IRS rules), and then recommend grants to eligible nonprofits over time. For many Christian donors, the most significant advantage is not complexity but clarity: it separates the decision to give from the administrative work of distributing grants, and it can support disciplined, planned generosity across years and seasons.

DAFs have become a significant part of the charitable landscape. In 2023, donors recommended an estimated $52.16 billion in grants from DAFs in the United States, as reported in the National Philanthropic Trust annual DAF report (National Philanthropic Trust).

What a DAF cannot do for a donor

A Christian DAF cannot decide which ministries are faithful, effective, and well-governed. It cannot verify whether a charity’s stated outcomes match reality, or whether financial reporting is transparent. It cannot tell a donor whether a ministry’s theological commitments are consistent with the donor’s convictions. The DAF may simplify execution, but it does not remove the donor’s obligation to practice discernment and to give in a way that honors God.

What this means in practice is that DAF use should be paired with a verification mindset. Most Trusted exists for this reason: donors can give with greater confidence when ministries are evaluated against The Most Trusted Standard, a 15-criteria framework spanning Faith Foundation, Financial Integrity, Governance and Leadership, and Transparency and Effectiveness. Tools are helpful; trust must be warranted.

Use a Christian DAF when you need a stable structure for volatile seasons

When income is irregular or unusually high

Many donors experience “lumpy” years: a business sale, a major bonus, a concentrated stock position, a real estate transaction, or a year of unusually high income. A DAF can help a donor be generous in the year resources are received while distributing grants thoughtfully over time. That is not merely tax strategy; it can be a way of resisting the tendency to let high-income years expand lifestyle rather than expand generosity.

The harder question is not whether the deduction is legal; it is whether the donor remains committed to actual grantmaking rather than letting funds sit indefinitely. DAF assets are already dedicated to charitable purposes. Yet donors still bear responsibility to ensure that charitable intentions become charitable action.

When you want to avoid erratic giving patterns

Some Christian donors give inconsistently because their administrative load is high, not because their convictions are weak. Others find themselves reacting to emotionally compelling stories rather than sustaining commitments to long-term work. A DAF can support steadier rhythms: recurring grants, planned distributions, and seasonal discernment. That stability matters for ministries that budget staff, programs, and direct service around expected revenue.

Christians genuinely disagree about the best way to balance spontaneous generosity with planned generosity. The New Testament commends both readiness and order: “Each of you should give what you have decided in your heart to give” (2 Corinthians 9:7) and “on the first day of every week, each one of you should set aside a sum of money in keeping with your income” (1 Corinthians 16:2). A DAF can serve either impulse, but it most often strengthens the second.

Use a Christian DAF when you want to give appreciated assets without distorting ministry incentives

Appreciated stock and complex gifts

For donors with appreciated securities, contributing stock to a DAF can be a straightforward path to charitable giving that may avoid capital gains tax and convert an asset into grantmaking capacity. The details depend on the donor’s tax situation and the DAF sponsor’s policies, and counsel from a qualified tax professional remains prudent.

What we have learned across our verification work is that donors who give complex gifts often care deeply about mission integrity and long-term outcomes. Yet complexity can create distance: the more a gift is processed through intermediaries, the easier it is to stop asking hard questions about how ministries are governed, how results are measured, and whether claims are verifiable.

Guarding against perverse incentives

Designing a giving plan around appreciated assets can unintentionally steer donors toward organizations that are simply “easy to fund” rather than those that are best positioned to serve. This is one reason donors should resist letting the vehicle determine the mission. Ministries should not be chosen because they are administratively convenient but because they are faithful to Christ’s call and demonstrably responsible with resources.

For donors who are comparing organizations, we encourage a disciplined practice: confirm legal status, read audited financials when available, examine board governance, and look for transparent reporting that matches a coherent theory of change. Our work at Most Trusted is built around these due-diligence priorities, expressed in The Most Trusted Standard, because mature generosity is not only generous; it is accountable.

Use a Christian DAF when you need distance from fundraising pressure without distancing from the Church

Reducing noise without losing pastoral accountability

Some donors consider a DAF because they feel worn down by persistent fundraising. A DAF can create a healthier boundary: donors can decide a budget for giving, then distribute grants without being pulled into every campaign cycle. This can be especially helpful for donors whose public visibility invites constant requests.

Yet boundaries can also become isolation. Christian giving is not only a private financial act; it is part of the Church’s shared life, shaped by teaching, mutual exhortation, and local responsibility. A DAF should not become a mechanism for avoiding the relationships that keep generosity honest.

Practical decision points for donors

A Christian DAF is more likely to serve a donor well when it supports a clear, written set of convictions about where and why to give. In our observation, donors make better long-term decisions when they can articulate the ministries and outcomes they are committed to support, rather than granting only when an appeal is emotionally compelling.

- Use a Christian DAF when you have a defined annual giving budget and want predictable grantmaking.

- Use a Christian DAF when you need to separate the timing of income from the timing of grants.

- Use a Christian DAF when you plan to give appreciated assets and want clean administration.

- Be cautious if you already struggle to follow through on giving intentions.

- Be cautious if anonymity will reduce necessary accountability to family, elders, or trusted counsel.

For donors who are building their broader stewardship approach, we address adjacent questions across Christian Stewardship Services with the same emphasis: generosity should be spiritually serious and operationally responsible.

Use a Christian DAF when your due diligence process is mature enough to match your giving capacity

Why verification becomes more necessary as giving increases

Larger giving capacity does not merely increase impact; it increases the consequences of error. Donors with significant DAF balances can inadvertently fund weak governance, financial opacity, or exaggerated impact claims at scale. The scandals that periodically surface in the nonprofit sector are rarely caused by a single missing policy; they are more often the result of weak oversight, concentrated authority, and the absence of transparent reporting.

The IRS requires public charities to file Form 990, and the form remains a baseline source for nonprofit financial and governance information (IRS). Yet a Form 990 cannot tell the whole story. It is a starting point for questions, not the end of diligence.

How The Most Trusted Standard fits a DAF strategy

DAFs are structurally well-suited for donors who want to build a portfolio of trusted ministries and sustain them over time. But that portfolio should be constructed on evidence rather than reputation alone. Across our verification work, we see meaningful differences in how ministries articulate doctrine, handle restricted funds, manage conflicts of interest, report outcomes, and respond to criticism. These are not peripheral matters. They signal whether a ministry is likely to endure in faithfulness and whether donor funds are likely to be used as represented.

This is where Most Trusted can serve donors: we evaluate ministries against The Most Trusted Standard so that confidence is grounded in verification rather than sentiment. Donor-advised funds can make giving more efficient; verification makes giving more trustworthy. For donors who want deeper insight into operational realities of DAF administration, we discuss related considerations in How Christian Stewardship Services Manage Donor-Advised Funds.

FAQs for When to use a Christian DAF for giving

Should we use a Christian DAF for tithing to our local church?

Many churches can receive grants from a DAF if they are recognized as eligible public charities, but whether it is wise depends on what the tithe represents in a donor’s theology and practice. Some donors prefer to give their tithe directly from cash flow as a regular act of worship tied to the church’s ordinary ministry. Others use a DAF to stabilize giving during irregular income years. If using a DAF creates distance from the Church’s shared life or weakens regularity, direct giving may be the better discipline.

Is a Christian DAF mainly a tax strategy?

A DAF has real tax implications, but a Christian approach should treat those as secondary to stewardship. The moral question is whether the structure strengthens generosity, accountability, and thoughtful partnership with ministries. If a DAF leads to delayed grantmaking, reduced diligence, or disengagement from the needs of neighbor and Church, the tool is being misused even if it is being used legally.

A faithful DAF strategy serves mission, accountability, and love of neighbor

When to use a Christian DAF for giving becomes clearer when the donor’s aim is clear: to honor God with resources by giving freely, wisely, and verifiably. A DAF is well-suited for irregular income, complex assets, planned generosity, and sustainable support for trusted ministries. It is poorly suited for donors who want the benefits of giving without the ongoing responsibility of discernment. Mature Christian generosity requires both a ready heart and a rigorous commitment to truth.