Tax-smart giving through Christian stewardship services is not a tactic for the spiritually indifferent. It is a way of ordering our financial lives so that generosity is steady, accountable, and free from panic when April arrives. The harder question is whether tax planning subtly becomes the point, displacing worship and mercy with private financial advantage.

Scripture refuses that separation. Jesus warned that “where your treasure is, there your heart will be also” (Matthew 6:21), and Paul commended purposeful, planned generosity rather than impulse alone (1 Corinthians 16:2). The goal is not to give because the tax code rewards it; the goal is to give because Christ is Lord, and then to give wisely within the lawful structures of our time.

Stewardship and tax planning belong together, but in a proper order

Christian donors often feel a tension that is not merely psychological. We want to give freely, but we also want to be prudent with what God has entrusted to us. Some believers worry that any attention to deductions compromises the purity of the gift. Others assume that “good stewardship” means minimizing taxes at nearly any cost. Both instincts miss something.

Tax policy in the United States is designed, in part, to encourage private philanthropy. When a donor deducts a charitable gift, the donor is not “taking from the ministry”; the donor is following a public incentive created by law. Yet the New Testament does not frame generosity as a strategy for self-benefit. Christian giving is an act of worship, a participation in the care of neighbor, and a sign of the coming kingdom. The tax result is secondary.

When deductions help, and when they do not

Many committed givers assume they will “get credit” for every gift on their tax return. That is no longer automatically true. After the Tax Cuts and Jobs Act, far fewer taxpayers itemize deductions, which means many households receive no federal income tax benefit from charitable giving beyond the standard deduction. The IRS has noted this shift, and it materially changes how many families should plan their giving IRS.

What this means in practice is that donors who are motivated by faithful generosity should not be discouraged if their giving does not reduce their federal tax bill. The faithfulness of the gift is not measured by its deductibility. At the same time, households with significant itemized deductions, business owners, and donors with appreciated assets often have legitimate opportunities to give more effectively by planning ahead.

Stewardship services should strengthen formation, not replace it

A Christian stewardship service can be a genuine pastoral good when it teaches restraint, contentment, and disciplined generosity. It becomes spiritually thin when it is reduced to “how to keep more.” The best advisors ask questions that are as moral as they are technical: Are we giving in a way that is proportionate to our means? Are we avoiding hidden control motives by insisting on excessive restrictions? Are we willing to give even when it costs?

Because many donors support ministries beyond their local church, tax-smart giving should also increase the quality of our discernment. A donor’s responsibility is not only to be generous, but to be truthful about where gifts go and what they accomplish.

How Christian donors actually maximize charitable deductions responsibly

The most common deduction mistakes are not exotic. They involve timing, documentation, and misunderstanding what counts as a charitable contribution. Mature stewardship pays attention to these ordinary details, because carelessness can create needless conflict with the IRS and can expose ministries to reputational risk.

Itemizing, bunching, and the discipline of planned giving

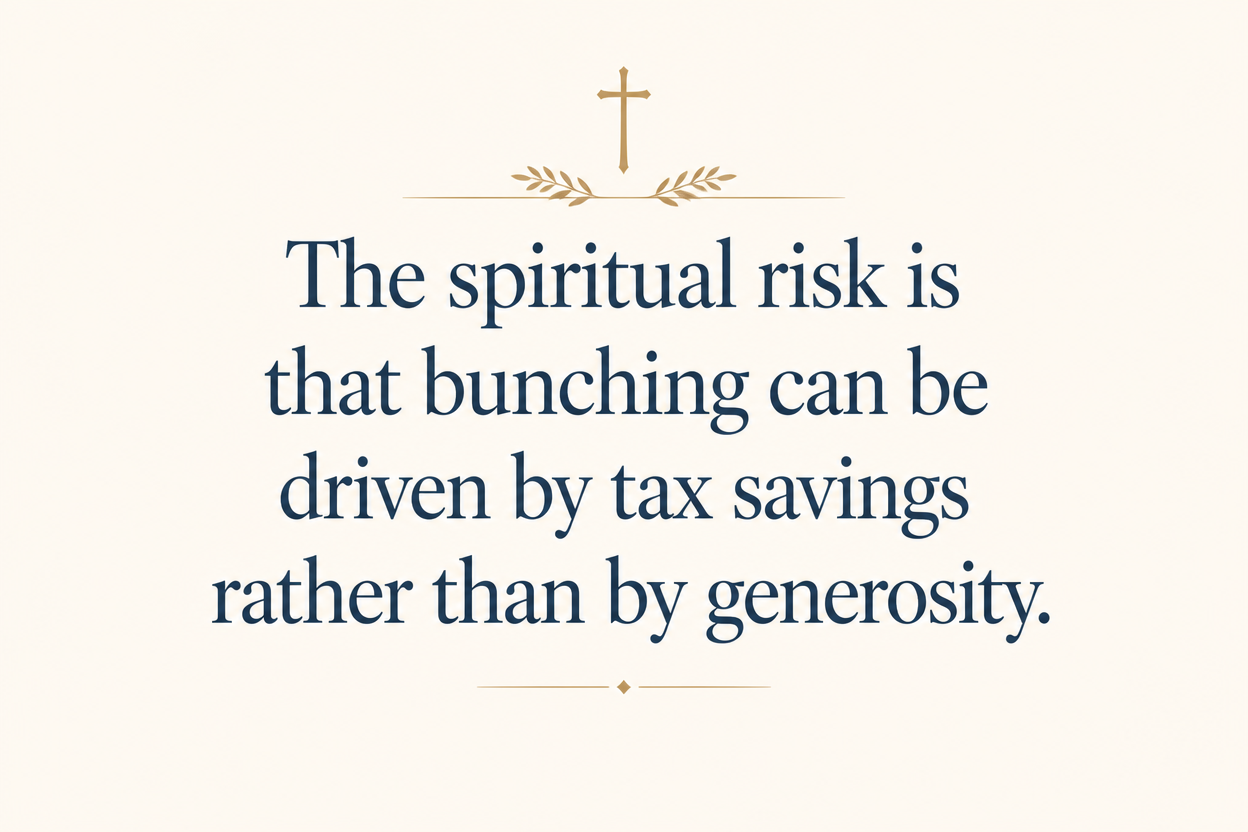

Because the standard deduction is significant, some donors choose to “bunch” charitable gifts—giving multiple years of intended generosity in one tax year—so that itemized deductions exceed the standard deduction in that year, then taking the standard deduction in alternating years. This is a legal strategy recognized in mainstream philanthropic planning and discussed widely among nonprofit and tax professionals Fidelity Charitable.

The spiritual risk is that bunching can be driven by tax savings rather than by generosity. The spiritual opportunity is that it forces disciplined planning. Donors who bunch often use a donor-advised fund to preserve a steady cadence of ministry support while timing the tax deduction in a single year. Donor-advised funds also introduce governance questions—recommendation privileges, family succession, and anonymity—that should be considered carefully rather than treated as neutral financial plumbing.

Gifts of appreciated assets and capital gains

For donors with taxable investment accounts, giving long-term appreciated securities is often one of the most tax-efficient ways to fund ministry. When structured properly, donors can generally avoid capital gains tax on the appreciation and may claim a charitable deduction for the fair market value, subject to applicable limitations. The IRS provides the governing rules for charitable contributions and substantiation requirements, and donors should consult them directly or through competent counsel IRS Publication 526.

Christian donors sometimes hesitate here because securities feel “less personal” than writing a check. That is a category mistake. The moral substance is the same: a relinquishing of control and a real transfer of value for the good of others. When appreciated assets allow us to give more without diminishing our capacity to meet other obligations, that can be a form of prudent generosity rather than a clever workaround.

Qualified charitable distributions and retirement assets

Donors who are age 70½ or older may be able to make qualified charitable distributions (QCDs) directly from an IRA to eligible charities. A QCD can satisfy required minimum distributions while keeping the distribution out of taxable income, which can matter for Medicare premium calculations and other income-based thresholds. This is not a niche technique; it is a widely used method for older givers, and the rules are governed by the IRS IRS.

Not every ministry is equipped to answer QCD questions quickly. Donors should expect responsiveness and clarity, because administrative confusion can turn a well-intended gift into a compliance problem.

Documentation is moral as well as legal

Tax-smart giving is often treated as a paperwork exercise. But Christian donors should treat substantiation as a matter of truthfulness. When the IRS requires a contemporaneous written acknowledgment for gifts of $250 or more, it is not merely bureaucracy. It is a safeguard against inflated claims and a protection for the integrity of the charitable sector.

What forms and receipts actually matter

For cash or check gifts, donors generally need bank records and written acknowledgments from the charity for gifts of $250 or more. For noncash gifts over certain thresholds, additional forms apply, and qualified appraisals may be required for higher-value property. The IRS provides detailed guidance on substantiation and the relevant forms, including rules around noncash contributions and Form 8283 IRS.

Christian donors sometimes assume that a ministry’s spiritual credibility excuses administrative weakness. In our work at Most Trusted, we observe the opposite: ministries that are doctrinally serious often treat financial administration as an extension of discipleship. They issue accurate receipts, avoid ambiguous language about quid pro quo benefits, and make it easy for donors to keep clean records.

Quid pro quo and the integrity of the gift

If a donor receives goods or services in return for a contribution—banquet tickets, merchandise, special access—the deductible amount is generally limited to the portion that exceeds the fair market value of what was received. This is a frequent source of donor confusion, and it can create reputational harm for ministries that blur the line between generosity and purchase. Christian organizations should be especially careful here, because the church has long understood the spiritual peril of turning gifts into transactions.

Wise stewardship services will press donors to ask whether certain “benefits” should be refused, even if they are technically permissible, when they distort motives or create inequity among supporters.

Verification matters when tax-smart giving increases complexity

As giving becomes more tax-sensitive—through donor-advised funds, gifts of securities, complex restricted gifts, or estate plans—the margin for misunderstanding increases. Complexity can serve generosity, but it can also conceal dysfunction. A donor may “execute” a technically sophisticated gift to a ministry whose governance is weak, whose reporting is thin, or whose claims cannot be evaluated.

That is where independent verification becomes a form of stewardship. Most Trusted exists to help donors give with confidence by evaluating ministries against The Most Trusted Standard, a 15-criteria framework that examines faith commitments, financial integrity, governance, and transparency about outcomes. Many donors already apply rigor to asset allocation and tax planning; applying similar seriousness to ministry credibility is not cynicism. It is obedience to the biblical call to walk in the light.

For donors evaluating stewardship services or philanthropic vehicles, the central question is not merely “Is this tax-efficient?” It is “Does this help us give faithfully, and does it direct resources toward ministries that can be trusted?” A natural starting point for that due diligence is our work on Christian Stewardship Services.

Restrictions, donor intent, and ministry flexibility

Christian donors often want to restrict gifts to a specific program: a school scholarship fund, a church plant, a translation project, a relief effort. Sometimes restrictions are appropriate, especially when a ministry is raising funds for a clearly defined project with measurable costs. But restrictions can also constrain leaders in ways that undermine effectiveness or encourage unhelpful internal accounting games.

Christians genuinely disagree about how much donor intent should control organizational decisions. Some argue that restrictions increase accountability and reduce mission drift. Others note that over-restriction can distort priorities and divert leadership attention toward fundraising rather than pastoral and programmatic competence. The wise path is neither to restrict reflexively nor to give unrestrictedly without discernment. It is to match the form of the gift to the maturity of the ministry and the clarity of the need.

Year-end planning without turning giving into a deadline

Year-end is a real planning window. Donor-advised fund contributions, securities transfers, and receipt deadlines can require lead time, and ministries are often strained in December. Yet a December surge can also tempt donors into impulsive giving that bypasses due diligence, especially when marketing is emotionally charged.

Stewardship services serve donors well when they establish rhythms earlier in the year: periodic reviews of giving commitments, pre-approved organizations, and clear criteria for evaluating emergency appeals. That kind of preparation reduces the likelihood that a tax deadline will govern our generosity.

A mature approach to tax-smart giving strengthens generous freedom

Tax-smart giving through Christian stewardship services is best understood as disciplined clarity: we give because Christ commands and compels, and we plan because stewardship is accountable to God and neighbor. The tax code can reward certain choices, but it cannot confer righteousness, and it cannot substitute for wisdom about which ministries deserve trust.

When our giving is planned, well-documented, and directed toward verifiable ministry work, it becomes easier to be generous without anxiety. That is not a small good. It is one way our financial lives can bear quiet witness that the Kingdom of God is more secure than any portfolio, and that faithful stewardship is measured by love, truthfulness, and sustained obedience.