What donation receipts Christian legal ministries should provide is not a cosmetic administrative question. For Christian donors, it is one of the clearest moments when integrity becomes verifiable: the ministry either tells the truth plainly about what was given, what was received, and what can be claimed, or it leaves the donor to guess. Given the moral weight Scripture places on honesty in money matters, a receipt is a small document with disproportionately spiritual significance (Proverbs 11:1).

Legal ministries also operate in a category where donors often give under pressure: a crisis phone call, an urgent asylum case, a family facing eviction, a church leader needing counsel after a scandal, a prisoner seeking representation. Urgency can be appropriate, but urgency also increases the risk of sloppy documentation. The ministries worth supporting do not treat compliance as secular nuisance; they treat it as part of faithful stewardship.

Receipts are not merely tax paperwork

Truthfulness is the first purpose of a receipt

Christian ministry is accountable to a higher standard than avoiding IRS penalties. A donation receipt is a ministry’s written testimony that it will not shade the truth when money is involved. That is why a mature organization does not bury key facts in fine print or use ambiguous language about “impact” that obscures what the donor actually purchased, received, or restricted.

Across our verification work at Most Trusted, we observe that ministries with serious governance and financial controls tend to have consistent receipting practices regardless of gift size or donor prominence. That consistency matters because Scripture’s warnings about partiality apply with particular force in financial dealings (James 2:1–4). Receipts are one place where a ministry can demonstrate impartial integrity at scale.

The legal context is real, and donors bear some responsibility

American tax law places responsibilities on both the charity and the donor. The donor must substantiate deductions, and the ministry must provide contemporaneous written acknowledgment when required. For donors who itemize, the IRS rules are not optional suggestions; they are binding standards that protect the public trust in the charitable system. The governing source for deduction substantiation is IRS Publication 526 and related regulations (Internal Revenue Service).

What the IRS requires for cash and noncash gifts

For cash, check, and card gifts over 250 dollars

When a single contribution of $250 or more is made, donors generally need a contemporaneous written acknowledgment from the charity to claim the deduction. Christian legal ministries should provide a receipt that includes the amount received and whether any goods or services were provided in exchange for the gift. This is not a matter of preference; it is the standard set out in IRS guidance (Internal Revenue Service).

The phrase “contemporaneous” also carries meaning. The acknowledgment should be received by the donor by the earlier of the date the donor files the return or the due date of the return. Ministries that send receipts months late force donors into uncertainty or retroactive reconstruction. Where a ministry is serious about protecting donors, it builds systems that prevent this predictable failure.

For noncash gifts, more information and more care

Noncash gifts raise additional complexity: property, vehicles, appreciated securities, and in-kind goods have different substantiation rules. A sound ministry receipt will acknowledge what was donated (without asserting a value the ministry did not determine), the date received, and a description sufficient for donor records. Donors may also need Form 8283 in certain cases, and ministries may have to sign the form or provide additional documentation depending on the gift type. The best starting point for donors is the IRS’s official noncash contribution guidance (Internal Revenue Service).

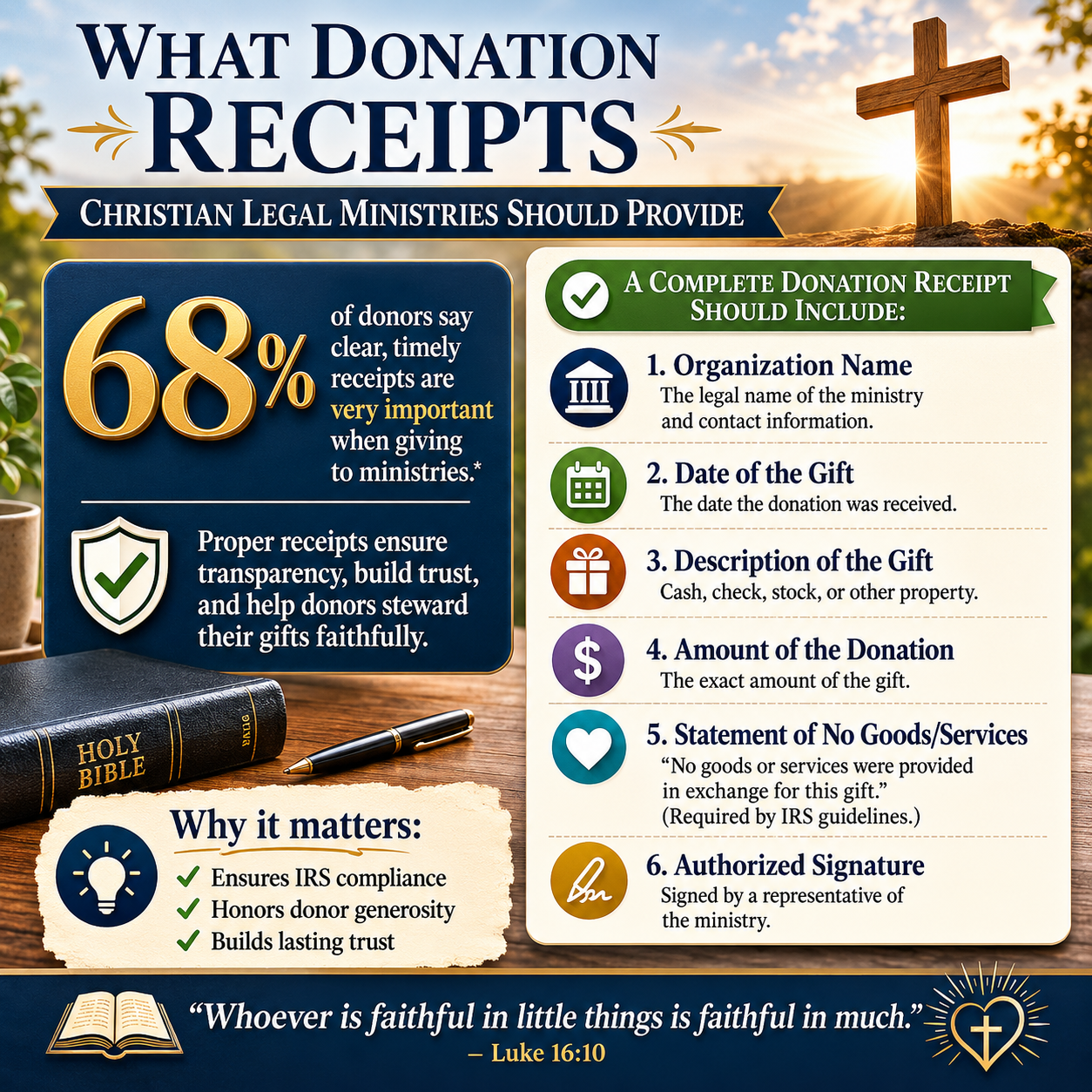

What a Christian legal ministry receipt should include every time

Core elements that should appear on the acknowledgment

Many ministries can recite the IRS minimums, yet still issue receipts that are unhelpful, vague, or inconsistent. For Christian legal ministries—where gifts may fund direct client services, litigation costs, training, or policy work—clarity should be standard practice. A donor should not need a phone call to interpret a receipt.

- Ministry name and contact information sufficient for donor records and follow-up.

- Date the contribution was received (and for recurring gifts, the date(s) covered if issuing a year-end statement).

- Amount received for cash, check, and card gifts, or a description of noncash property (without assigning an unsupported value).

- A clear statement about goods or services: either “no goods or services were provided in exchange for this contribution,” or a good-faith estimate of the value of any goods or services provided.

- For quid pro quo events, a clear separation of the payment and the deductible portion, with the value of benefits disclosed.

Ministries sometimes hesitate to include the goods-and-services statement for fear of sounding “legalistic.” That hesitation is misplaced. Scripture does not commend ambiguity. Christian leaders should be able to say plainly what happened, particularly when handling other people’s money.

Consistent terminology prevents donor confusion

Receipts should consistently use the language of a “charitable contribution” or “gift,” not “payment,” unless it is in fact a payment for goods or services. For example, a registration fee for a professional continuing education course offered by a legal ministry may be partly or entirely non-deductible. Precision helps donors avoid overstating deductions and helps ministries avoid accidentally mischaracterizing revenue.

Donors evaluating ministries in the broader space of Christian Legal Services Ministries should treat receipt quality as one data point among many. It cannot prove faithfulness by itself, but it often reveals whether operational discipline exists under the surface.

Special situations where receipts often go wrong

Quid pro quo giving and fundraising dinners

Christian legal ministries sometimes host banquets, briefings, or prayer breakfasts. If a donor receives a meal, a book, admission, or other benefits in exchange for a payment, the ministry should disclose the fair-market value of those benefits and clearly state the deductible portion. When ministries handle this sloppily, donors face real risk. The IRS has explicit rules for quid pro quo contributions and disclosure obligations (Internal Revenue Service).

There is also a pastoral dimension. Many donors attend these events because they want to stand with a ministry’s mission. They should not be made to feel that asking for accurate documentation is unspiritual. A ministry can be warm and grateful without being imprecise.

Restricted gifts and designated giving

Legal ministries often raise funds for specific casework, client emergency assistance, or a particular program area (immigration representation, anti-trafficking advocacy, religious liberty litigation, or prison reentry clinics). Donors may give with restrictions; ministries may also receive “designations” through intermediaries such as donor-advised funds.

A receipt should not promise what the ministry cannot guarantee. If a donor writes “for the Smith family case,” but the ministry’s policy is to treat such notes as donor preferences rather than binding restrictions, the receipt and donor communication should reflect that reality. Overpromising can create moral hazard: it tempts ministries to fundraise around emotionally compelling specifics while reserving discretion to reallocate without clarity. Donors deserve candor, and ministries deserve the freedom to tell the truth even when it complicates fundraising.

How receipt practices signal trustworthiness under The Most Trusted Standard

Receipting reflects controls, not just courtesy

Within The Most Trusted Standard, receipting sits close to the question of whether a ministry’s financial reporting and donor communications are disciplined, verifiable, and consistent. A receipt cannot substitute for audited financials, conflict-of-interest policies, board oversight, and clear reporting of program outcomes. Yet it is often the first concrete artifact a donor sees.

Ministries that meet higher standards tend to treat receipts as part of a broader transparency posture: consistent year-end giving summaries, clear treatment of noncash gifts, and prompt correction when an error is discovered. The opposite pattern is also common: ministries that are evasive in receipts are frequently evasive elsewhere, because the underlying issue is not paperwork but accountability.

Donor questions that deserve clear answers

For donors seeking to give wisely within Tax-Smart Giving to Christian Legal Services, the following questions are reasonable to ask before significant gifts:

Do receipts arrive promptly and consistently? If timing depends on who gave and how much, that is a governance concern.

Does the receipt clearly address goods and services? Ministries should not force donors to interpret silence.

How does the ministry handle restricted gifts? Policies should be written, and donor communication should reflect them.

Is there a clean separation between donations and fees? Legal services ecosystems can blur lines, and clarity protects both donor and ministry.

These questions do not imply suspicion. They are ordinary due diligence for Christian stewardship, especially when donors are trying to be faithful with resources God has entrusted.

FAQs for What donation receipts Christian legal ministries should provide

Does a Christian legal ministry have to send a receipt for every gift?

No. The IRS rules focus on substantiation requirements, and a contemporaneous written acknowledgment is generally required for any single contribution of $250 or more if the donor intends to claim a deduction. Many ministries still choose to send receipts for smaller gifts as a matter of good practice. Donors should retain bank records for smaller cash gifts and seek the required acknowledgment for larger ones (Internal Revenue Service).

Should the ministry put a dollar value on donated goods or a vehicle?

Generally, the donor—not the charity—determines the value for noncash donations, and the ministry should acknowledge receipt with a description of the item(s) rather than asserting a value it did not establish. Vehicles and other property can trigger specific forms and rules. Donors and ministries should follow the IRS’s noncash contribution guidance and, when needed, seek qualified tax advice (Internal Revenue Service).

A faithful receipt is a small act of stewardship

Christian donors are not asking ministries to be bureaucratic; they are asking ministries to be truthful and careful. A proper donation receipt protects the donor’s conscience, protects the ministry’s witness, and strengthens trust in Christian charity as a public good. When a legal ministry handles receipting with clarity and consistency, it signals that it is prepared to handle larger responsibilities with the same seriousness.