What donation records donors need to keep is a stewardship question before it is a tax question. Christians give not merely to satisfy a line on a return, but to honor the Lord with integrity, to protect the ministries we support, and to avoid preventable confusion when memory fades and leadership changes.

Tax law sets a floor, not a ceiling. The IRS rules exist because charitable deductions reduce taxable income, and the government expects verifiable documentation. The church has long taught that our “yes” should be “yes” (Matthew 5:37), and that integrity is not situational. Good records are one practical way donors embody that consistency.

Start with the IRS standard for substantiation

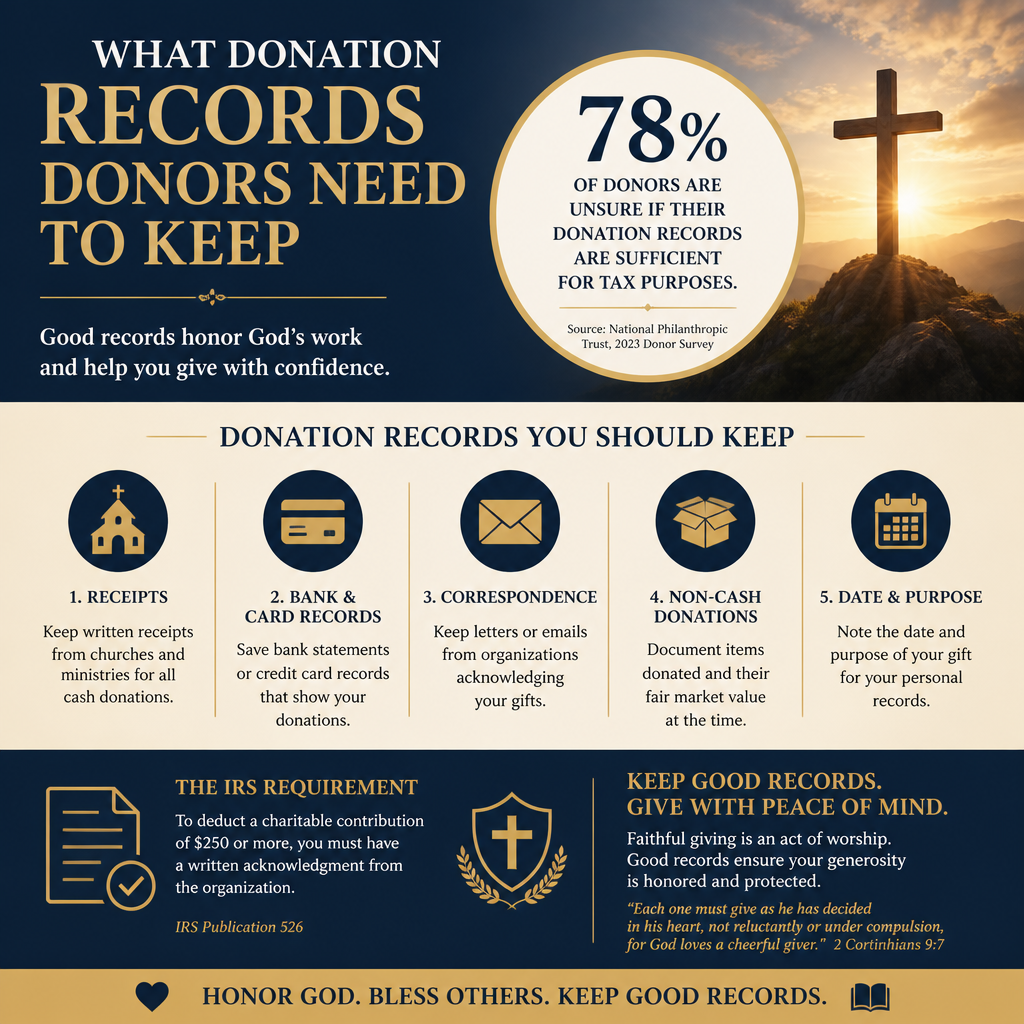

The IRS is explicit: if a donor wants to claim a charitable contribution deduction, the donor must keep records that substantiate the gift. That requirement applies even when the ministry is trustworthy and even when the gift was made in good faith. What this means in practice is that donors should collect documentation at the time of giving, not after a year-end scramble.

For gifts under 250 dollars, keep a bank record or written communication

For any single contribution of less than $250, the IRS generally allows substantiation through either a bank record (such as a canceled check, bank statement, or credit card statement) or a written communication from the charity showing the name of the charity, the date, and the amount. If the communication is electronic, retain it in a form that can be reproduced. The IRS summarizes these rules in its Charitable contributions guidance. IRS

For gifts of 250 dollars or more, you need a contemporaneous written acknowledgment

For any single contribution of $250 or more, a bank record alone is not sufficient. The donor must have a contemporaneous written acknowledgment from the charity, which must state (1) the amount of cash contributed, (2) a description of noncash property contributed (if applicable), and (3) whether the charity provided any goods or services in exchange for the gift, with a good-faith estimate of value if it did. The requirement is “contemporaneous” because it must be received by the time the donor files the return or the due date (including extensions), whichever comes first. IRS Publication 526

Match your records to the way you gave

Christian donors now give through donor-advised funds, recurring online gifts, text-to-give, appreciated securities, and in-kind donations. Each method has a distinct paper trail. The harder question is not whether documentation exists; it is whether donors can retrieve it quickly and prove what was given, when it was given, and what was received in return.

Online and recurring gifts

For online giving, retain the confirmation email or PDF receipt and keep bank or card statements that show the charge. For recurring gifts, donors often assume the year-end statement is enough. It may be, but only if it contains the required acknowledgment language for any gift of $250 or more and clearly identifies the ministry and dates. When a processor appears on statements under a different merchant name, keep the processor receipt as well; it can resolve disputes later.

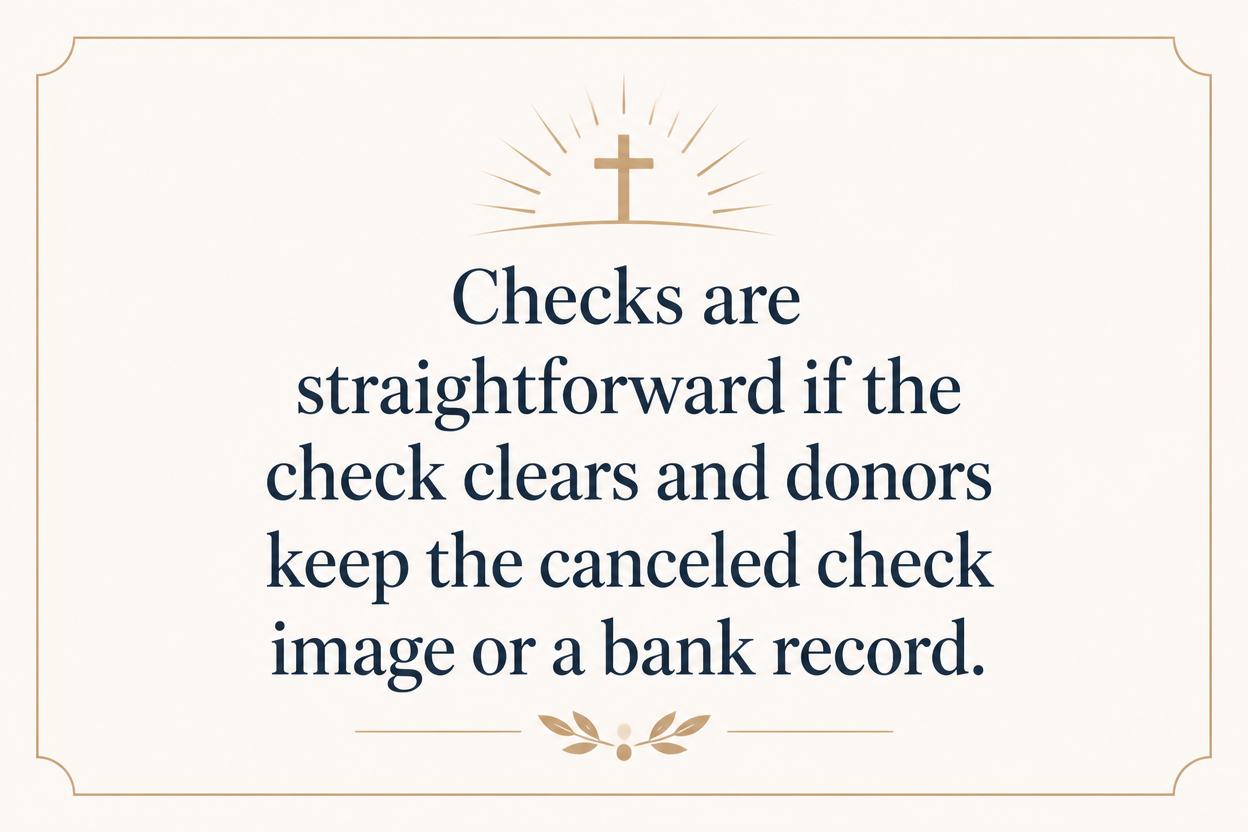

Checks, cash, and text-to-give

Checks are straightforward if the check clears and donors keep the canceled check image or a bank record. Cash is where mature practice matters most. If cash is given, donors should secure a written receipt from the ministry at the time of the gift; a personal ledger entry is not sufficient for tax substantiation. For text-to-give, save the text confirmation and the card statement, and ensure the ministry’s acknowledgment includes the required wording for larger gifts.

Noncash gifts require more rigor than most donors expect

Many Christians give property because it is a meaningful form of generosity and, in some cases, a tax-wise way to give. But noncash gifts are where donors most often discover that “we meant well” is not the same as “we documented well.” The IRS distinguishes between noncash gifts below certain thresholds and those that trigger additional forms and appraisals.

Keep detailed descriptions and fair market value support

For noncash gifts, donors should keep records describing the item, its condition, how it was acquired, and the method used to determine fair market value. If the gift is a vehicle, there are special rules and a specific written acknowledgment requirement (Form 1098-C or equivalent statement). IRS vehicle donations guidance

When Form 8283 and qualified appraisals come into play

For larger noncash gifts, donors may need to file Form 8283 with their tax return, and for certain property above specific thresholds, a qualified appraisal is required. The technical details depend on the type of property and the claimed value. Donors should avoid retroactive valuation and should not treat a ministry’s gratitude letter as a valuation document; charities generally acknowledge what was received, not what it was worth.

Keep records that address the spiritual and governance realities of giving

Christian giving is often relational. Donors support missionaries they know, crisis needs that arise quickly, and ministries that invite designated giving for specific projects. Relationship is not the problem; ambiguity is. Records protect both donor and ministry from later disputes about intent, restrictions, and benefit.

Restricted gifts and designated giving

If a donor intends a gift to be restricted to a particular program, missionary, or project, keep documentation that shows the restriction in writing and that the ministry acknowledged it. Donors should also understand a common governance distinction: many ministries treat “designations” as donor preferences rather than binding restrictions, because boards retain fiduciary responsibility to use funds for the ministry’s exempt purposes. When donors expect legal restriction, they should confirm the ministry’s policy in writing before giving.

Quid pro quo and benefits received

When a donor receives something of value in exchange for a gift—event tickets, a dinner, a premium, or other goods or services—the tax-deductible portion is generally only the amount that exceeds the fair market value of what was received. The ministry is required to provide a disclosure statement when quid pro quo contributions exceed $75. Donors should keep that disclosure with their year-end records. IRS quid pro quo guidance

Build a recordkeeping system that can stand up to scrutiny

Recordkeeping is not about living under suspicion; it is about being prepared for ordinary administrative realities: staff turnover at ministries, donor transitions, family estates, and the occasional IRS inquiry. The ministries that donors can trust over decades tend to make documentation easy to obtain and easy to understand. Across our verification work at Most Trusted, we observe that ministries that meet The Most Trusted Standard typically pair gratitude with clarity: receipts arrive on time, the acknowledgment language is correct, and restricted-gift policies are stated plainly.

A practical file set we recommend

Donors do not need a complicated system, but they do need a complete one. We recommend keeping the following in a dedicated annual folder (digital or physical):

- Year-end giving statements from each ministry and any donor-advised fund sponsor

- Contemporaneous written acknowledgments for any single gift of $250 or more

- Bank and credit card statements showing the date and amount of each gift

- Documentation for noncash gifts, including descriptions, valuation support, and any required forms

- Copies of correspondence about restrictions, designations, or special gift agreements

Where donors commonly get tripped up

Three patterns recur. First, donors rely on a credit card statement for a gift of $250 or more and later learn that the IRS requires a written acknowledgment. Second, donors give noncash property without keeping enough detail to support fair market value. Third, donors assume that because a ministry is Christian, it will automatically issue correct receipts; most are trying to do the right thing, but administrative competence varies widely.

For donors giving through a Christian financial service ministry context—where gifts, fees, and member benefits can coexist—clarity matters even more. Not every payment associated with a ministry is automatically a charitable contribution. Donors should distinguish between (a) deductible gifts, (b) program-related payments that are not gifts, and (c) purchases or services. When in doubt, ask the ministry for a written explanation of what portion, if any, is treated as a charitable contribution.

For donors evaluating which organizations consistently handle these matters well, our coverage of Christian Financial Service Ministries reflects a broader pattern: administrative rigor is not opposed to faith. It is often one indicator that a ministry is prepared to steward resources with sobriety.

FAQs for What donation records donors need to keep

Do donors need receipts for every church or ministry gift?

If donors want to claim a charitable contribution deduction, they need substantiation for each gift. For gifts under $250, a bank record or written communication from the charity is generally sufficient. For any single gift of $250 or more, donors need a contemporaneous written acknowledgment that includes the required IRS language about goods or services provided in exchange for the gift.

How long should donors keep donation records?

The IRS generally recommends keeping records as long as they may be needed for the administration of any provision of the Internal Revenue Code. In practice, many donors keep donation records at least as long as the statute of limitations for the relevant return, and longer when gifts involve noncash property, carryforwards, or estate planning. Donors should consult a qualified tax professional for guidance aligned to their situation.

Give with the clarity that integrity requires

Christian generosity is meant to be free, not careless. Good donation records let donors give with peace of mind, support ministries without later confusion, and honor the Lord in the small, concrete acts of truthfulness that sustain trust over time. For donors who want to understand how receipts, disclosures, and reporting practices vary across organizations, our work in Tax Receipts and Reporting for Donations to Christian Financial Service Ministries addresses the specific documentation questions that arise when ministry, finance, and compliance intersect.