Claiming Christian financial service ministry donations on taxes is straightforward in principle: the IRS allows a charitable deduction only for gifts to qualified organizations, and only when a donor can substantiate the gift. The complexity is that many Christian financial service ministries sit close to the boundary between “charitable contribution” and “payment for services,” and the boundary matters for both tax integrity and Christian stewardship.

Christian donors tend to ask two honest questions at the same time. First, “How do we do this correctly?” Second, “How do we remain faithful to the spirit of generosity rather than treating giving as a transaction?” Jesus’ warning that we cannot serve both God and money (Matthew 6:24) does not forbid tax deductions, but it does press us toward clarity, truthfulness, and clean accounting.

Start with the IRS question the deduction depends on

The IRS does not allow a charitable deduction because a gift is meaningful; it allows a deduction because a gift is made to a qualifying recipient and is properly documented. The first task is not receipt management. It is identifying what, exactly, the ministry is in legal and tax terms.

Confirm the ministry is a qualified charitable organization

For a U.S. federal income tax deduction, the ministry generally must be recognized as a tax-exempt organization eligible to receive deductible contributions, typically a 501(c)(3). Donors can verify status using the IRS Tax Exempt Organization Search, which is the authoritative public directory for this purpose: IRS.

Some ministries that serve Christians financially are not structured as 501(c)(3) charities. They may be a 501(c)(4), a mutual benefit arrangement, a for-profit business with Christian commitments, or a program housed within a church. These structures can be legitimate, but they change the tax answer. A Christian donor should not assume deductibility from a Christian name, a pastoral endorsement, or even a ministry’s internal language of “giving.”

Distinguish a donation from a fee, premium, or member benefit

The IRS framework is simple: a deductible contribution cannot be a payment made in exchange for goods or services. That matters for ministries that provide financial counseling, debt management plans, insurance-like coverage, tuition benefits, member tools, or other tangible services. When a donor receives something of value, the deductible portion is generally limited to the amount that exceeds the value of what was received, and sometimes the payment is not charitable at all.

What this means in practice is that a “support payment” may function like a fee even when it is spiritually framed. Donors should read the ministry’s own disclosures carefully and, when the ministry provides a written statement describing a quid pro quo benefit, follow it rather than improvising a larger deduction.

Document gifts the way the IRS expects, not the way newsletters describe

Once the gift is truly charitable and made to a qualified organization, the next issue is substantiation. Donors do not need complexity, but they do need to follow the IRS rules that apply to their gift size and method.

Know what records you need for cash and noncash gifts

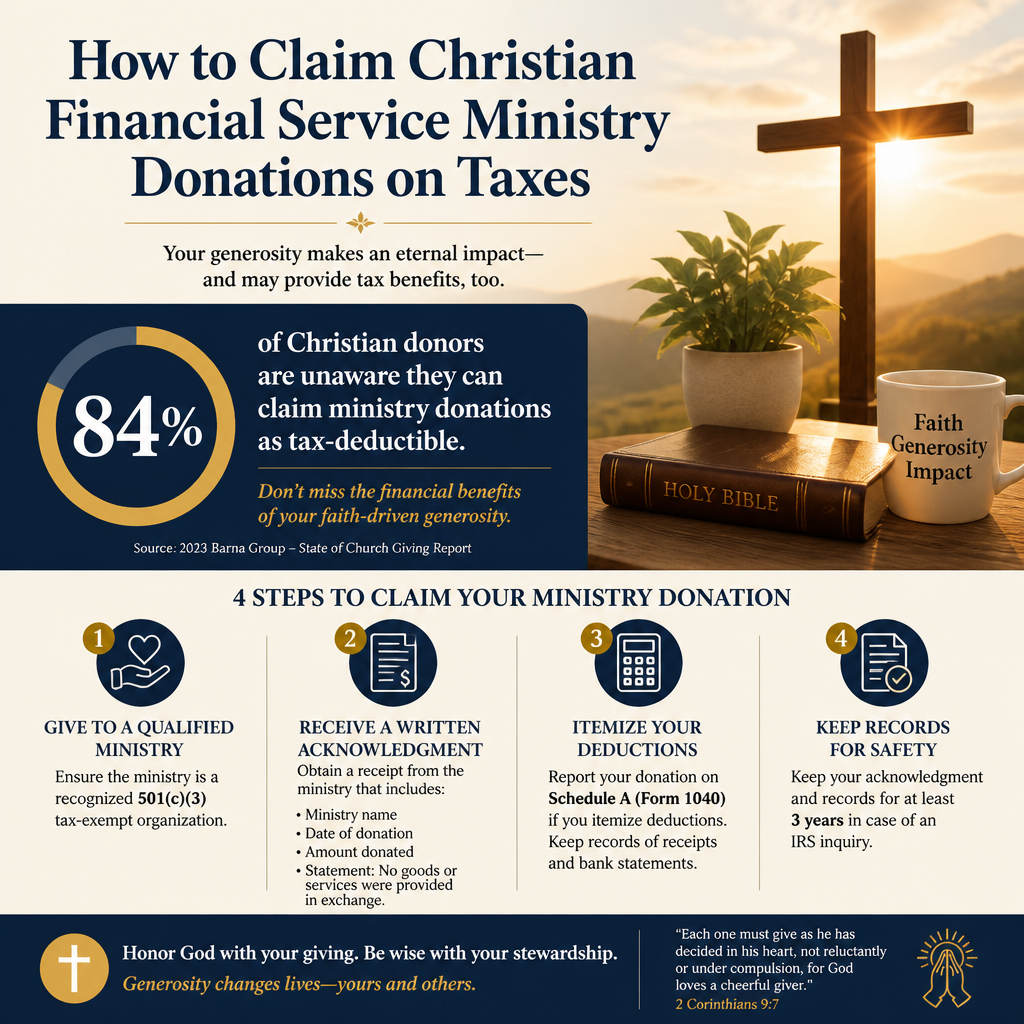

For cash gifts, the IRS requires a bank record or a written communication from the charity showing the name of the organization, the date, and the amount. For gifts of $250 or more, donors must have a contemporaneous written acknowledgment from the charity, and it must state whether any goods or services were provided in exchange for the contribution. These requirements are not optional and can determine whether the deduction is allowed: IRS.

For noncash gifts, the recordkeeping requirements grow more detailed, and higher-value gifts may require formal appraisal and specific IRS forms. Many Christian donors give appreciated securities, property, or other noncash items precisely because doing so can be tax-wise and mission-forward. The discipline is to document the gift with the same seriousness with which one would document any significant financial transaction.

Store receipts in a way that will endure a real audit

Church and ministry donors are often surprised by how ordinary audit-proof documentation looks. It is rarely impressive; it is simply consistent. Our team has seen donors lose deductions because they had good intentions and poor records.

- Keep year-end giving statements and individual acknowledgments together.

- Retain proof of payment such as canceled checks or bank confirmations.

- For online gifts, save the confirmation email and the transaction detail page.

- For noncash gifts, keep the donation description, valuation support, and any required forms.

- Note any benefits received, such as event meals or member services, and the charity’s stated value.

Handle quid pro quo and designated gifts with care

The harder tax questions for Christian financial service ministries often involve benefits and restrictions. Donors want their gifts to be effective and aligned with conviction. The IRS wants clarity about whether the payment is a gift, and if it is, whether it is a gift to the organization rather than to a particular person.

Quid pro quo contributions are common in service-oriented ministries

If a ministry provides something in return, the organization should provide a disclosure statement for contributions over $75 that are partly a contribution and partly a purchase. Donors should retain that disclosure because it is a direct indicator of how the organization views the transaction and what portion, if any, is deductible: IRS.

Christians genuinely disagree about how to think about “benefit” when ministries serve donors directly. Some will treat any personal benefit as disqualifying. Others will recognize that Christian ministries often serve the giver and the wider community at once, and that service is not automatically a commercial exchange. The tax answer, however, is not theological interpretation. It is whether the payment is a contribution under IRS rules.

Designated gifts must remain under the ministry’s control

Donors often want to designate funds: a benevolence fund, a scholarship pool, a hardship grant, a counseling subsidy. Designation can be appropriate, but only when the ministry retains full discretion and control over how the funds are used within the charitable purpose. A “gift” earmarked for a specific individual is usually not deductible, even when the need is real and the cause is Christian.

This is one place where donors can honor both Scripture and the law. The New Testament’s emphasis on integrity in financial administration is not theoretical. Paul commended practical safeguards “so that no one should blame us about this generous gift” (2 Corinthians 8:20–21). Donors should expect ministries to structure restricted giving in ways that protect both recipient dignity and donor honesty.

Apply special rules for unusual gifts and modern payment methods

Many mature donors support Christian financial service ministries through appreciated assets, donor-advised funds, IRA distributions, and recurring electronic giving. These tools can be faithful instruments, but each carries different documentation and timing rules.

Donor-advised funds and IRA distributions require coordination

When giving through a donor-advised fund, the donor generally takes the deduction at the time of the contribution to the DAF, not when the DAF later grants to the ministry. The receipt that matters for taxes is the DAF sponsor’s acknowledgment, not only the ministry’s thank-you note. Similarly, for qualified charitable distributions from an IRA, the rules are specific about how the funds are transferred and how they are reported; donors should coordinate with their custodian and tax preparer rather than relying on informal assumptions.

These approaches are especially common among donors committed to long-term generosity. They also create room for misunderstanding when a ministry’s development communication assumes a simple checkbook donation. The administrative discipline is not a lack of faith; it is a commitment to truthful reporting.

Cryptocurrency, stock, and other noncash assets raise valuation questions

Noncash gifts can be especially powerful for ministry funding, but they also require disciplined valuation. A donor cannot “estimate” a deduction in a way that outpaces what can be substantiated. Ministries can help by providing accurate descriptions of what was received and the date received, while avoiding providing valuation advice that belongs with the donor and the donor’s advisors.

When donors are unsure, the wisest approach is to treat the tax deduction as a secondary good and the integrity of the gift as the primary good. That posture aligns with Christian moral seriousness and tends to reduce practical risk.

Use verification to clarify what you are supporting and how it is governed

Even when the tax mechanics are clear, donors often face a prior question: “Is this ministry administratively strong enough to handle gifts properly?” For Christian financial service ministries, that question touches financial controls, governance accountability, transparency, and a coherent Christian purpose.

What donors should evaluate beyond deductibility

At Most Trusted, we exist to help donors give with confidence by evaluating ministries against The Most Trusted Standard, a 15-criteria framework that examines faith commitments, financial integrity, governance and leadership, and transparency and effectiveness. Across our verification work, we observe that strong ministries tend to issue acknowledgments that are timely, accurate, and compliant, and they tend to maintain clear distinctions between charitable support and paid services.

Donors who want a broader view of the ministry landscape can begin with Christian Financial Service Ministries. The point is not to outsource discernment; it is to bring verifiable evidence into it, especially where money, trust, and spiritual language intersect.

Where donors commonly misstep and how to avoid it

Two errors appear frequently. The first is assuming that spiritual intent automatically creates a charitable deduction. The second is ignoring receipts and disclosures because “it is ministry.” Donors should instead treat documentation as part of faithful stewardship: an outward expression of inward integrity.

For donors working through receipts and reporting questions across multiple ministries, Tax Receipts and Reporting for Donations to Christian Financial Service Ministries is a useful reference point for the common documentation patterns and decision points.

FAQs for How to claim Christian financial service ministry donations on taxes

Are payments to a Christian financial service ministry always tax-deductible?

No. Payments are generally deductible only when they are charitable contributions to a qualified organization and are not made in exchange for goods or services. Some Christian financial service ministries charge fees for counseling, tools, or member benefits, and those payments may not be deductible. When benefits are provided, only the portion that exceeds the value of the benefits may qualify, and the ministry’s quid pro quo disclosure should guide the donor’s treatment.

What receipt do we need to claim a donation of $250 or more?

For a contribution of $250 or more, donors must obtain a contemporaneous written acknowledgment from the charity stating the amount, the date, and whether any goods or services were provided in exchange for the gift. Without that acknowledgment, the deduction can be disallowed even if the gift was real. Donors should store the acknowledgment alongside the proof of payment and any year-end giving statements.

Stewardship and accuracy belong together

Claiming Christian financial service ministry donations on taxes is not primarily an exercise in maximizing benefit; it is an exercise in truthfulness. Donors who confirm a ministry’s qualified status, distinguish gifts from fees, and keep audit-grade records can give freely without distorting their reporting. That combination of generosity and integrity reflects the kind of stewardship Scripture consistently commends.