How to bunch giving through a Christian donor-advised fund is, at its core, a question of stewardship under real-world constraints. Many Christian donors want to increase generosity without letting tax strategy dictate their theology, yet they also recognize that wise planning can free more resources for the work of the Kingdom.

“Each one must give as he has decided in his heart, not reluctantly or under compulsion, for God loves a cheerful giver” (2 Corinthians 9:7). That verse does not cancel prudence; it disciplines it. Bunching is best understood not as a way to give less, but as a way to give steadily to ministry while contributing strategically to a giving account in selected years.

Understand bunching as timing the contribution, not timing obedience

What bunching is and why it exists

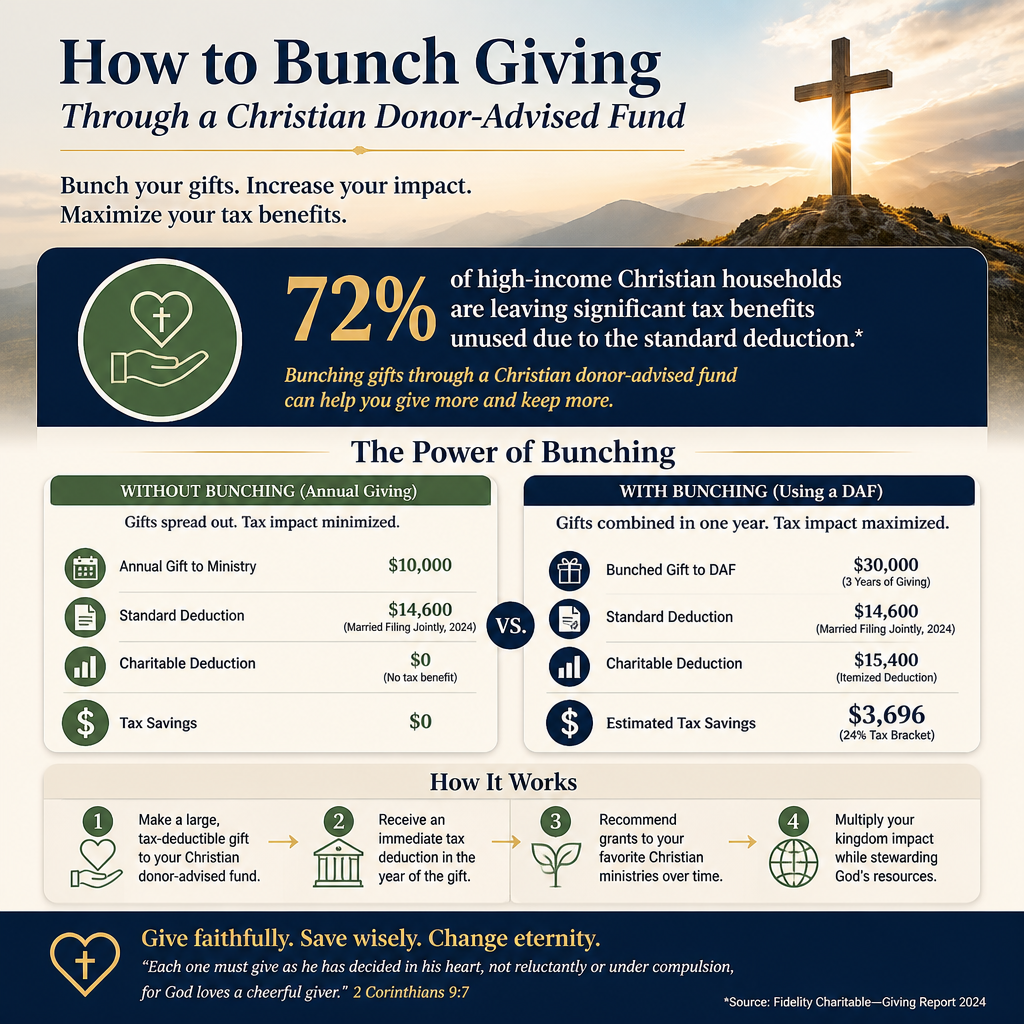

Bunching is the practice of combining multiple years of charitable contributions into one tax year so that itemized deductions exceed the standard deduction in that year. The standard deduction is high enough for many households that they no longer itemize, which means many faithful givers receive no marginal tax benefit from their charitable gifts even when their giving is substantial.

A donor-advised fund is designed for this timing question. You contribute to the fund in a year when itemizing makes sense, and then you recommend grants to ministries over time. In other words, the tax deduction is tied to the contribution to the fund, while the ministry’s cash flow can remain steady through consistent grants.

What the DAF changes and what it does not

A Christian donor-advised fund does not change the spiritual question of generosity; it changes the mechanics of when you fund the giving account. Used well, it can prevent an unhealthy swing between “high giving years” and “low giving years” at the church or ministry level. Used poorly, it can become a justification for treating giving as a financial instrument rather than an act of worship.

The discipline is to hold two truths together: God’s people are called to thoughtful stewardship, and God’s people must not allow prudence to become a substitute for obedience.

Use the standard deduction threshold as the practical trigger

The reason bunching has become more common

Bunching has become more relevant because the standard deduction is substantial. For 2024, the standard deduction is $29,200 for married couples filing jointly and $14,600 for single filers, which means many donors will not itemize unless they have significant deductions beyond charitable giving, such as mortgage interest and state and local taxes within applicable limits. Source: Internal Revenue Service.

What this means in practice is that donors often face a binary choice: either keep giving annually and take the standard deduction every year, or concentrate contributions in some years to itemize and claim a deduction for charitable gifts in those years.

A simple way to think about the math without reducing giving to math

We have found it helpful to frame the decision with a straightforward question: “In which years will our total itemized deductions exceed the standard deduction by enough to matter?” If the answer is “rarely,” bunching may be worth exploring. If the answer is “most years,” the added complexity may not be justified.

Christians genuinely disagree about how much attention to give to tax outcomes. Some prefer simplicity as a form of integrity. Others see careful planning as an extension of stewardship. The stronger position is not necessarily the more complex one; it is the one that best serves consistent generosity and clear conscience.

Pair a bunching strategy with a Christian donor-advised fund grant rhythm

Contribute in one year, grant over several years

The basic pattern is simple: contribute a larger amount to your Christian donor-advised fund in a year when you will itemize, then recommend grants to your church and other ministries over the next several years. This can preserve steady support for ministries while allowing the donor to claim the deduction in the year of contribution.

Many donors choose an every-other-year rhythm. Others choose a three-year rhythm, particularly when income varies meaningfully (business owners, farmers, those with a one-time liquidity event). A donor-advised fund can accommodate either approach, but the right rhythm depends on cash flow, conviction, and the ministries’ need for predictability.

A basic operational checklist

- Decide a grant plan that keeps church and ministry support stable year to year.

- Choose the “bunching year” when you expect itemizing to be most beneficial.

- Fund the DAF with cash and or appreciated assets, as appropriate to your situation.

- Schedule grants in advance so giving remains disciplined rather than reactive.

- Reassess annually as tax law, income, and ministry priorities change.

For donors giving to multiple organizations, the DAF also adds administrative clarity: one contribution receipt for the year, then a set of grants that can be paced and documented without losing sight of where the money is actually going.

Consider asset type, not just dollar amount

Appreciated assets can strengthen the strategy

Bunching is often discussed as a cash decision, but many donors hold appreciated assets. Contributing appreciated securities can be particularly efficient because it may allow the donor to avoid capital gains tax while still claiming a charitable deduction for the fair market value, subject to IRS rules. Source: Internal Revenue Service.

That efficiency is not an argument for giving; it is an argument for giving wisely once the decision to give has already been made. The moral hazard is subtle: donors can begin to treat the “most efficient” gift as the “most faithful” gift. Faithfulness is measured by love of God and neighbor, not by tax engineering.

Restrictions, eligibility, and the limits donors must respect

Donor-advised funds are not a private checking account for charitable preferences. Grants must go to eligible organizations, and the donor cannot receive impermissible benefits in return for a grant. Christians should welcome these constraints. The purpose of charitable giving is not to create a parallel economy of personal advantage; it is to fund mission.

When donors want to support individuals directly, or to fund activities that do not fit charitable eligibility, a DAF may not be the right tool. In those cases, donors may need to give outside the DAF, or fund through structures designed for those purposes, with counsel that respects both legal compliance and Christian conscience.

Protect your giving with verification and discernment

Bunching can magnify both impact and risk

When donors bunch, they may contribute a larger amount at one time. That can be a gift to ministry, but it also concentrates decision-making. A larger pool of charitable capital can be granted quickly to excellent work, or it can be granted quickly to unaccountable work. The same strategy that increases capacity can increase exposure.

This is where diligence belongs. Scripture’s warnings about wealth are not only about greed; they are also about the distortions that come from power without accountability. Mature giving includes asking whether an organization is financially sound, well-governed, and truthful about results.

How Most Trusted fits into a bunching plan

Across our verification work at Most Trusted, we observe that donors are often forced to choose between speed and certainty. The ministries that meet The Most Trusted Standard tend to make that trade-off less painful because they show verifiable strength across Faith Foundation, Financial Integrity, Governance and Leadership, and Transparency and Effectiveness. That does not make giving risk-free, but it does make it more defensible.

As donors consider a bunching strategy, we encourage a parallel discipline: decide in advance which types of ministries will receive grants, and apply consistent standards to those recipients. For many donors, that means starting with the commitments closest to home—local church, long-term partners—and then expanding to additional ministries with the same seriousness.

For donors evaluating the broader landscape of Christian Donor-Advised Funds, the most important question is not merely which platform is convenient, but which practices help donors keep giving accountable, theologically coherent, and stable over time.

And for donors building a wider set of practices around Giving Strategies Using Christian Donor-Advised Funds, bunching is best treated as one tool among several—useful when it serves generosity, misused when it serves control.

FAQs for How to bunch giving through a Christian donor-advised fund

Does bunching reduce what a ministry receives year to year?

It does not have to. The donor can contribute a large amount to the donor-advised fund in a bunching year and then recommend grants on a steady schedule so the church and ministries receive consistent support. The key is to separate the timing of the contribution from the timing of the grants.

Should we bunch giving if we already take the standard deduction every year?

Possibly, but only if bunching would cause you to itemize in the bunching year and if the added complexity will not disrupt consistent generosity. Many donors decide the spiritual and relational costs of complexity outweigh the tax benefit. Others find that bunching, paired with disciplined grantmaking, meaningfully increases capacity for long-term ministry support.

A faithful bunching strategy is steady, accountable, and ministry-centered

Bunching giving through a Christian donor-advised fund can be a prudent way to align tax timing with steady support for ministry. The stronger aim is not a larger deduction but a more stable pattern of generosity, with recipients chosen through discernment and supported with consistency. When the mechanics serve the mission—and when accountability is treated as part of stewardship—bunching can help donors give with both freedom and clarity.