How to donate stock to a Christian donor-advised fund is, for many serious givers, less about mechanics than about stewardship. Appreciated securities can be one of the cleanest ways to fund long-term, prayerful giving while avoiding unnecessary tax friction that reduces what ultimately reaches ministry.

Done well, a stock gift through a Christian donor-advised fund can increase the resources available for the work of the Kingdom, sharpen decision-making, and add discipline to a donor’s process. Done casually, it can create avoidable compliance problems, misaligned expectations with ministries, or an unexamined drift toward treating giving as mere tax planning.

Why stock gifts and why a Christian donor-advised fund

What stock giving accomplishes that cash cannot

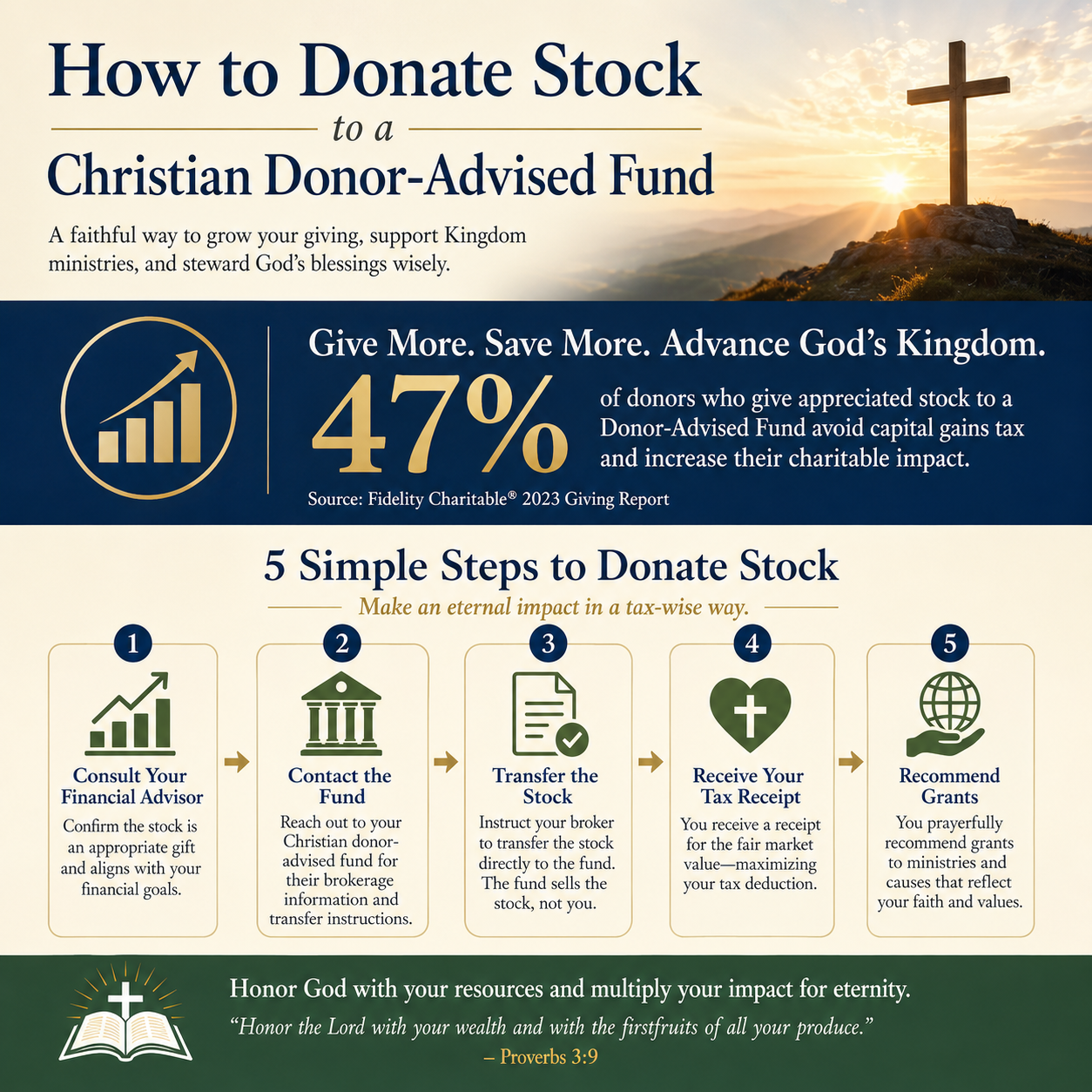

When a donor gives appreciated publicly traded stock held longer than one year, the charitable gift is generally valued at fair market value, and the donor generally avoids capital gains tax that would be triggered by selling first. That is not a loophole; it is a longstanding feature of U.S. charitable tax policy intended to encourage giving.

The practical consequence is straightforward: giving stock often allows more to be deployed for ministry than giving the same economic value in cash after a taxable sale. For donors with concentrated positions, long-held shares, or meaningful unrealized gains, this can be one of the more material stewardship decisions available.

Why donors choose a Christian donor-advised fund specifically

A donor-advised fund, in its simplest form, separates the moment of contribution from the moment of granting. For many Christian households, that separation serves spiritual ends as well as administrative ones: it creates room to discern, to verify, and to give in a manner consistent with convictions about doctrine, integrity, and fruitfulness.

Christians genuinely disagree about how much weight to place on tax efficiency versus sacrificial immediacy. Yet Scripture does not pit prudence against generosity. The same Proverbs tradition that commends openhandedness also commends wisdom, honest scales, and foresight. A Christian donor-advised fund can be one appropriate tool for donors seeking to practice both generosity and discernment.

Prerequisites before you initiate a stock transfer

Confirm the asset is eligible and properly held

Most donor-advised funds readily accept publicly traded securities. Complex assets are different: restricted stock, private company shares, cryptocurrency, and partnership interests often require additional review and may not be accepted at all. Before you begin, confirm the fund’s acceptance policy and timeline, especially if year-end giving is involved.

Also confirm how the stock is held. If shares are in a brokerage account, a transfer can usually be done via DTC. If shares are in certificate form, additional steps may be required. If the shares are held in a retirement account, the rules change materially; those situations should be handled with specific tax counsel.

Understand valuation and substantiation expectations

Publicly traded securities are typically valued based on the average of high and low trading prices on the date the donor-advised fund receives control of the shares. The receipt issued by the fund will generally acknowledge the contribution without stating a dollar value; donors document valuation through brokerage statements and standard tax reporting.

If you are considering non-cash gifts valued above certain thresholds, the IRS has specific substantiation requirements, including Form 8283 in many cases. The relevant guidance is published by the Internal Revenue Service at IRS.gov.

The step by step process to donate stock to a Christian donor-advised fund

Step 1 Open or access your donor-advised fund account

If you already have a Christian donor-advised fund, you will typically find a “contribute stock” workflow in the portal, including DTC instructions and fields to identify the sending brokerage. If you do not yet have an account, opening one should be done well before a deadline; operational backlogs near December are common across the sector.

For donors building a long-term approach, clarity about the fund’s theological commitments and grantmaking guardrails matters. A “Christian” label can cover a wide range of doctrinal and institutional realities, and the donor-advised fund sponsor effectively becomes a gatekeeper to downstream giving.

Step 2 Notify your brokerage and initiate the transfer

Your brokerage will require the receiving institution’s DTC number and account details. Some brokerages require a signed letter of authorization. The donor-advised fund sponsor typically provides a template that includes the receiving custodian information and instructions.

Once initiated, the transfer may take several business days. If your giving is time-sensitive, build margin for delays and confirm when the fund considers a gift “received” for tax purposes: it is generally when the fund takes control of the shares, not when you submit the paperwork.

- Confirm the exact stock symbol and number of shares to be transferred

- Send the donor-advised fund’s DTC instructions to your brokerage

- Request written confirmation from the brokerage once the transfer is submitted

- Watch for the donor-advised fund’s receipt and verify the received share count

- Document the date of receipt for your tax records

Step 3 Allow the fund to liquidate and credit your giving account

Most donor-advised funds liquidate contributed stock shortly after receipt and credit the proceeds to your giving account. This is one reason the donor-advised fund is often preferred over gifting stock directly to a ministry: many ministries do not have brokerage capacity, securities policies, or internal controls strong enough to receive and liquidate stock without added risk.

Christians sometimes assume that “direct to ministry” is always more faithful. In practice, a donor-advised fund can be a protective layer when it reduces administrative burden on a ministry and lowers the chance of an error that distracts from mission.

Granting wisely after the stock gift is complete

Discernment does not end when the contribution clears

The gift to the donor-advised fund is the tax-deductible contribution. The grants that follow are moral decisions with spiritual weight. A donor can move quickly and still be careful, but carefulness takes time: verifying doctrine, governance, financial integrity, and truthful reporting often requires more than a compelling story.

This is where disciplined evaluation becomes part of Christian stewardship. Across our verification work at Most Trusted, we observe that ministries with strong internal controls and transparent reporting tend to be more resilient over time, especially when leadership transitions, crises, or rapid growth pressure the organization.

What meaningful due diligence tends to include

Donors often default to proxies that feel safe—brand recognition, a charismatic founder, or a low reported overhead ratio. The field has had to reckon with the limits of overhead metrics, including the ways they can punish necessary investments in compliance and effectiveness. Charity Navigator’s long-standing discussion of this problem is a useful starting point at charitynavigator.org.

Most Trusted exists because mature Christian giving requires more than intuition. Our evaluations measure ministries against The Most Trusted Standard, a 15-criteria framework spanning faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. The aim is not to replace prayerful discernment but to discipline it with verifiable evidence.

For donors building an approach to giving through these vehicles, the broader context on Christian Donor-Advised Funds helps clarify common structures, constraints, and decision points.

Common risks and how to avoid them

Year end timing pressure and the temptation to improvise

Many stock gifts fail at the simplest point: timing. A transfer initiated in late December may not settle before year-end, and the donor may discover too late that “submitted” is not “received.” The safeguard is unglamorous: initiate earlier, confirm receipt dates, and treat calendars as part of stewardship rather than as an inconvenience.

For donors who intend a specific year’s deduction, clarity on IRS rules and the fund’s processing timelines is not optional. We have seen donors create avoidable frustration with ministries and fund sponsors simply by assuming a transfer would complete on their preferred timetable.

Complex assets and the necessity of specialist counsel

Some donors hold assets that can be transformative for generosity but complicated to contribute: private equity, closely held business interests, or restricted shares. Donor-advised fund sponsors vary significantly in whether and how they accept these gifts. These situations require careful coordination among the donor, the sponsor, legal counsel, and tax advisors.

This is also where donors should be cautious about confusing charitable intent with liquidity planning. A gift should not be structured in ways that compromise integrity or invite conflicts of interest. The charitable sector’s credibility depends, in part, on donors and institutions refusing cleverness that erodes trust.

Donors seeking a wider set of practices within this category of giving can also consult Giving Strategies Using Christian Donor-Advised Funds as they consider how tools, timing, and verification work together.

FAQs for How to donate stock to a Christian donor-advised fund

Can we donate stock directly to a ministry instead of through a Christian donor-advised fund?

Sometimes, yes. Some larger ministries have brokerage accounts, written gift acceptance policies, and the internal controls needed to receive and liquidate securities responsibly. Many do not. A Christian donor-advised fund often reduces administrative burden for the ministry and gives donors more time to verify the organization before granting.

When is the stock donation considered complete for tax purposes?

For publicly traded securities, the relevant date is generally when the donor-advised fund sponsor receives control of the shares, not when the donor initiates the transfer. Because processing times vary by brokerage and sponsor, donors should confirm the sponsor’s definition of “received” and retain documentation supporting the receipt date.

Stewardship that preserves both generosity and integrity

Donating appreciated stock to a Christian donor-advised fund can be a disciplined way to expand what is available for ministry, especially when giving is guided by verification rather than impulse. The goal is not merely a tax-efficient transaction, but a form of stewardship that honors the Lord with substance, refuses manipulative reporting, and directs resources toward ministries worthy of trust.