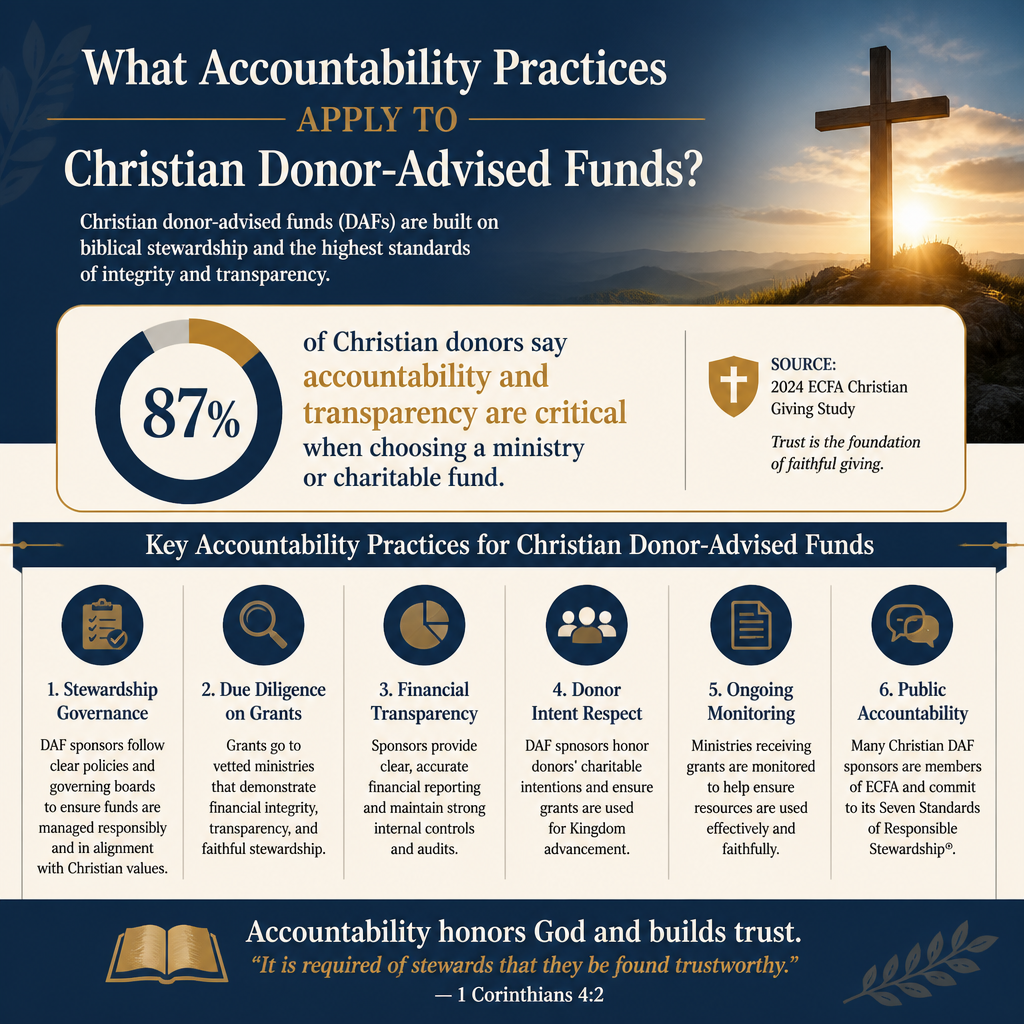

Accountability practices for Christian donor-advised funds begin with a sober premise: a DAF can be an instrument of faithful stewardship, but it can also distance the donor from the moral and practical consequences of giving. When a donor gives through an intermediary, the questions multiply. Who ensures grants align with Christian convictions? Who tests whether a ministry’s reporting is reliable? Who governs the sponsor itself with integrity worthy of the church’s trust?

Scripture does not treat money as neutral. Jesus’ warnings about wealth assume that financial decisions shape the soul, not merely the balance sheet. A DAF, at its best, can strengthen disciplined generosity and careful discernment; at its worst, it can become a spiritual “buffer” that replaces responsibility with convenience. Accountability practices are the difference.

Accountability begins with clarity about who bears responsibility

The donor’s role is not outsourced

A Christian donor-advised fund sponsor is the legal owner of assets once contributed, but the donor’s moral responsibility does not disappear with the tax receipt. The New Testament’s stewardship logic assumes accountable agency: “It is required of stewards that they be found faithful” (1 Corinthians 4:2). In DAF practice, that faithfulness includes diligence about where grants go, what they accomplish, and whether they honor Christ.

What this means in practice is that donors should expect an explicit division of responsibilities: the sponsor’s governance, compliance, and grant-processing controls; and the donor’s discernment about mission alignment and fruit. Where those lines are unclear, accountability usually weakens rather than strengthens.

The sponsor is not merely a payments platform

DAF sponsors vary widely. Some function primarily as administrative pass-throughs. Others take a more substantive posture, including due diligence on grantees, monitoring for legal and reputational risk, and setting faith-based eligibility standards. Christian donors should not assume that a “Christian” brand implies Christian controls. The sponsor should publish its policies in plain language and demonstrate that those policies are actually enforced.

Across our verification work at Most Trusted, we consistently find that donors confuse three different objects of trust: the sponsor, the grantee ministry, and the donor’s own intentions. Accountability requires distinguishing them. A sponsor can be well-governed and still facilitate grants to poorly governed ministries if donors are not equipped and standards are not clear.

Governance practices that deserve a donor’s scrutiny

Independent board oversight and documented controls

The sponsor’s governance is the first accountability layer. Donors should look for an active board with meaningful independence, documented conflict-of-interest policies, and a discipline of reviewing risk. A DAF sponsor is responsible for regulatory compliance, preventing prohibited benefits, and ensuring grants are made to eligible organizations for charitable purposes. Those duties require more than good intentions; they require controls.

Governance transparency is especially important because DAF sponsors often handle large balances relative to their staff size. Where oversight is thin, errors become systemic. The sponsor should be able to articulate how it reviews grant recommendations, handles exceptions, and audits internal compliance.

Conflicts of interest and donor influence

Christian donors also need candor about the moral hazards of donor influence. A sponsor may face pressure to approve grants that are technically legal but spiritually or ethically compromised: funding ministries with unaddressed leadership misconduct, financing “projects” that effectively benefit a donor’s family, or supporting organizations whose public theology is orthodox while their internal practices are not. Strong policies are necessary, but they are not sufficient; enforcement is the true test.

A responsible sponsor will publish clear standards on: private benefit, grants to individuals, scholarship practices, grants connected to donor-controlled entities, and the handling of restricted gifts. Donors should expect a process that can say “no,” not merely a workflow that processes requests.

Financial integrity and operational accountability in DAF administration

Transparent fees, investment policies, and grant processing

The sponsor’s financial accountability includes fee transparency, investment policy clarity, and timely, accurate grant processing. Donors should be able to understand what they pay, what services those fees cover, and how investment options are selected and monitored. Sponsors should also disclose whether they receive revenue sharing from investment providers and, if so, how that conflict is governed.

Delays and errors in grant processing are not merely inconveniences for ministries. Cash-flow volatility can distort program decisions, staffing, and long-term planning. The “Starvation Cycle,” described by Ann Goggins Gregory and Don Howard, shows how financial pressure and distorted funding expectations can degrade nonprofit effectiveness over time Stanford Social Innovation Review. DAF sponsors do not cause that cycle alone, but they can either reduce it through reliable operations or aggravate it through unpredictability.

Payout practices and the ethics of warehousing

Christians genuinely disagree about how aggressively DAF assets should be paid out. Some donors value the ability to give steadily through market cycles or to build capacity for a future, large gift. Others worry that DAFs encourage warehousing charitable dollars while needs are urgent. The law does not impose a universal payout requirement on DAF accounts, which places more moral weight on donors and sponsors to cultivate a culture of timely generosity.

Whatever posture a donor takes, accountability practices should include clear reporting of grants made and a disciplined plan for disbursement. The National Philanthropic Trust’s annual DAF report has long documented that aggregate DAF payout rates have generally exceeded the private foundation minimum in many years, but those are averages and do not resolve the question for an individual account National Philanthropic Trust.

Ministry due diligence and the question of spiritual credibility

Eligibility screens that go beyond 501c3 status

Legal eligibility is a baseline, not a verdict. A Christian DAF sponsor may rightly require that grantees be recognized charitable organizations, but donors also need accountability for distinctively Christian concerns: doctrinal fidelity, spiritual leadership integrity, safeguarding practices, and the truthful representation of impact. Those factors are not always visible from a Form 990 or a polished website.

For donors who want giving aligned with Christian conviction, a sponsor’s accountability practices should include some combination of: a faith statement standard, mission alignment questions, and a process for responding to credible allegations of abuse, fraud, or doctrinal misrepresentation. Silence and ambiguity are not neutrality; they are a decision to leave discernment entirely to donors, many of whom do not have the time or expertise to investigate well.

A disciplined approach to evaluating effectiveness

Effectiveness accountability is complicated. Not every ministry outcome can be reduced to metrics, and spiritual fruit does not always submit to measurement. Yet ministries routinely make claims that can be tested: number of pastors trained, translations completed, students served, prisoners discipled, crisis pregnancies supported, churches planted. Donors should expect ministries to report with enough specificity that a reasonable person can distinguish between aspiration and demonstrated work.

Two errors are common in the field. One is demanding business-style certainty where faithfulness and presence are central. The other is accepting vague stories in place of verifiable reporting. Mature accountability holds both: honoring the spiritual nature of ministry while insisting on truthfulness and basic evidence.

In our work evaluating ministries against The Most Trusted Standard, we focus on whether a ministry can demonstrate clear leadership accountability, responsible financial practices, and honest communication about results. Donors can use the same posture even when giving through a DAF: insist on integrity, not marketing.

Transparency practices that respect donors and protect ministries

What donors should be able to see in writing

Accountability is weakened when key policies are tribal knowledge. Donors should expect a Christian DAF sponsor to publish core documents or make them available on request. At minimum, donors should be able to understand how the sponsor governs itself, how it handles risks, and what it expects of grantees.

- Board and leadership identification, with conflict-of-interest standards

- Fee schedule and investment policy, including any revenue-sharing arrangements

- Grantmaking policies on restricted gifts, donor benefits, and grants connected to donor-controlled entities

- Eligibility standards for grantees, including any faith-based criteria

- Reporting practices: what donors receive and what the sponsor discloses publicly

Transparency should also include a posture toward questions. A sponsor that treats donor scrutiny as disloyalty is not prepared for the weight of Christian stewardship. The church’s giving is sacred, and those who administer it should welcome careful inquiry.

Privacy, anonymity, and the spiritual discipline of visibility

DAFs often permit anonymous giving. That can protect donors in sensitive contexts and reduce unhealthy dynamics of recognition. It can also complicate accountability when donors want to verify that a grant was received and used as intended, or when ministries depend on relational clarity to steward major gifts responsibly.

Wise practice distinguishes between healthy privacy and unaccountable opacity. Donors should ensure they can maintain adequate documentation of grants, follow up appropriately, and avoid patterns of giving that make it impossible to learn whether a ministry’s claims are credible. Christian giving is not performative, but neither is it meant to be untethered from truth.

For donors comparing sponsors and standards, it is often helpful to begin with the broader landscape of Christian Donor-Advised Funds and then evaluate how each sponsor articulates accountability in areas that matter most to Christian conscience.

Donors weighing these questions in the context of a broader stewardship approach may also find it clarifying to situate DAF practice within Faith-Based Stewardship in Christian Donor-Advised Funds, where the central issue is not merely administrative efficiency but faithfulness in how funds are held, released, and directed.

FAQs for What accountability practices apply to Christian donor-advised funds

What accountability should we expect from a Christian DAF sponsor versus from the ministries we support?

A sponsor should be accountable for governance, compliance, internal controls, fee and investment transparency, and a clear grantmaking policy that can be enforced. Ministries should be accountable for doctrinal clarity, leadership integrity, safeguarding, truthful fundraising, financial stewardship, and credible reporting of activities and results. A sponsor can improve donor confidence by offering due diligence resources, but it should not claim to “validate” a ministry unless it actually performs and updates that work.

How can we practice accountability if we want to give anonymously through a DAF?

Anonymous giving can still be accountable if we maintain documentation of each grant, verify receipt through the sponsor’s confirmation and the ministry’s acknowledgment when appropriate, and set a pattern of periodic review of the ministries supported. Where the giving relationship becomes complex or significant in size, anonymity should not prevent us from seeking sufficient clarity about leadership, safeguards, and the truthful representation of impact.

Accountability that serves love of neighbor

Christian donor-advised funds are not inherently faithful or unfaithful. They are instruments that can either strengthen stewardship or soften it. The accountability practices that matter most are the ones that keep money connected to responsibility: clear governance, transparent financial practices, disciplined due diligence, truthful reporting, and a culture that treats scrutiny as a form of love for the church and protection for the vulnerable.

When accountability is treated as an administrative add-on, donors drift toward convenience and ministries bear the cost. When accountability is treated as moral formation, DAF giving can become what it should be: deliberate generosity ordered by truth.