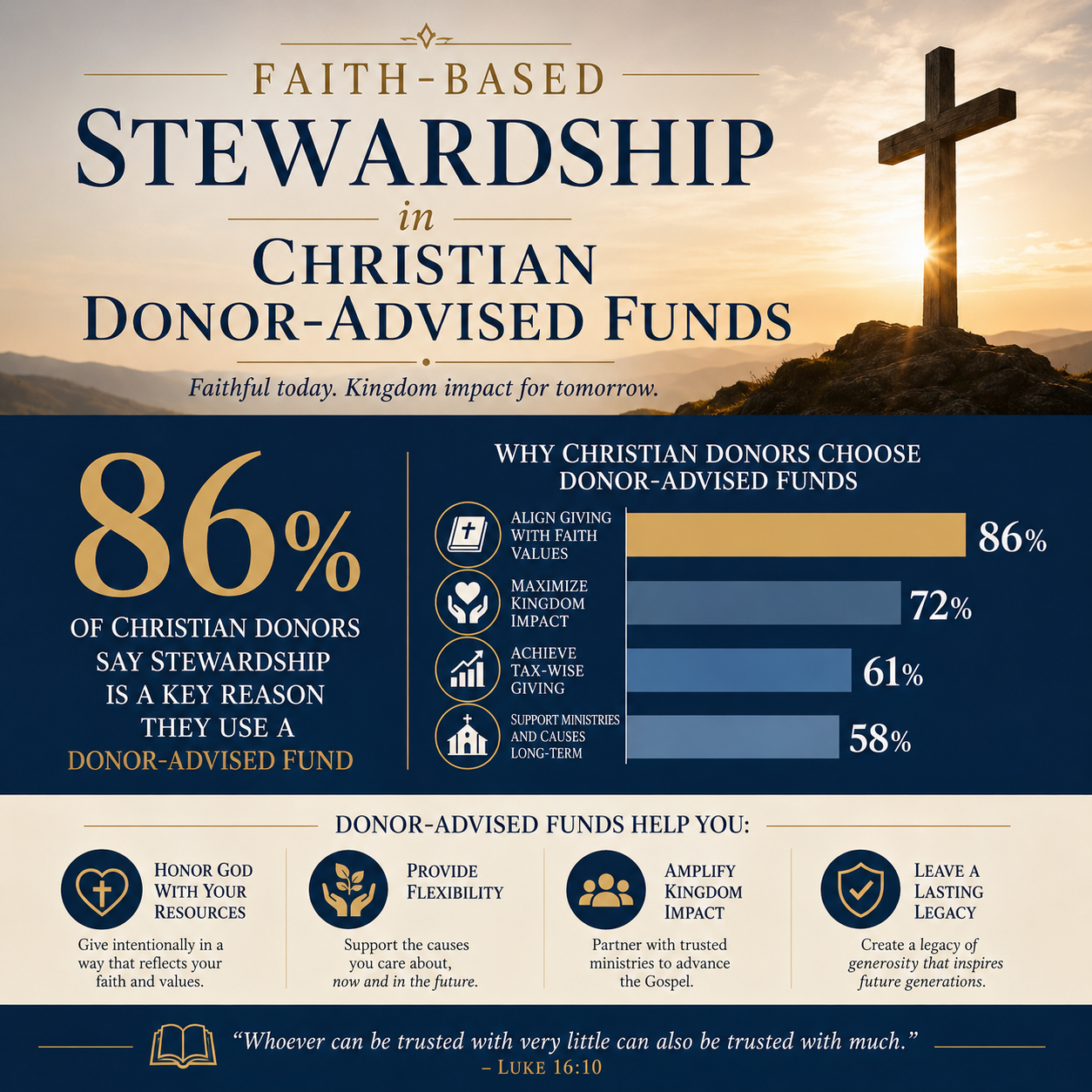

Faith-Based Stewardship in Christian Donor-Advised Funds is not a marketing preference; it is an attempt to bring a modern charitable instrument under the Lordship of Christ. A donor-advised fund can simplify giving, but it can also obscure moral responsibility if Christians treat it as a neutral container rather than a stewardship trust. The core question is whether a Christian DAF helps us give in a way that is faithful, accountable, and consistent with the ends Scripture sets for wealth.

Jesus spoke directly to the spiritual power of money: “You cannot serve God and money” (Matthew 6:24). The point is not that every financial tool is suspect, but that every financial tool must be examined in light of discipleship. A faith-based DAF exists for donors who want more than tax efficiency. They want alignment—between the source and stewardship of funds, the practices of the sponsoring ministry, and the moral shape of the resulting giving.

Christian stewardship in a DAF begins with a theology of ownership

Scripture’s stewardship frame is plain: “The earth is the LORD’s and the fullness thereof” (Psalm 24:1). Christians do not merely decide where to be generous; we are trustees of resources that belong to God. That theological claim changes the evaluation criteria for a donor-advised fund. The first question is not “What are the fees?” but “What does this structure form in us—and what does it incentivize in the institutions that receive our giving?”

The parable of the talents (Matthew 25:14–30) has often been flattened into a generic encouragement to productivity. Its sharper edge is accountability. Stewards answer to a master, and a faithful steward is not only generous but also responsible. In practice, Christian donors should expect a DAF sponsor to behave like an accountable steward: clear policies, sound controls, and decision-making that can be examined rather than merely trusted.

Giving becomes delayed when mission becomes optional

A DAF’s capacity to separate the timing of the tax deduction from the timing of the grant can be helpful in volatile income years, business exits, or estate planning. Yet the same feature can habituate delay. The New Testament’s moral urgency toward need—especially among the poor and vulnerable—does not map neatly onto indefinite warehousing of charitable capital (James 2:15–17).

Christians genuinely disagree about what “prudent timing” means in a DAF context. Some donors prefer to build a giving strategy over years; others see the delay as spiritually hazardous. What is not optional is intentionality: a giving plan that keeps generosity active, and a governance posture that treats the DAF as a means to love neighbor, not as a spiritualized savings account.

A stewardship tool is not spiritually neutral when it shapes behavior

Tools form habits. A DAF that makes giving frictionless can strengthen disciplined generosity, but it can also depersonalize it. A DAF that makes granting easy but accountability opaque invites a kind of charitable consumption—where donors feel good while remaining insulated from outcomes. Faith-based stewardship asks for the opposite: clarity about where funds go, and moral seriousness about whether those funds advance what God calls good.

Faith-based stewardship requires integrity in both investing and granting

Many Christian DAF conversations focus on investment screens, and for good reason. If donor assets are invested while awaiting distribution, the sponsor’s investment policy becomes part of the donor’s moral agency. A faith-based DAF should be able to explain, in specific terms, how it avoids profiting from industries that directly contradict Christian ethics and how it selects managers consistent with those commitments.

Investment screens are a moral claim, not a branding exercise

Negative screens (avoiding certain industries) and positive screens (seeking companies with beneficial practices) both carry trade-offs. Screens can reduce diversification, concentrate risk, and increase tracking error relative to broad indices. The harder issue is that screening is never exhaustive. Christians can agree that pornography and predatory lending are incompatible with neighbor-love while disagreeing about defense contracting, alcohol, or companies with mixed business lines.

What this means in practice is that a Christian DAF sponsor should publish its screening criteria, its process for reviewing disputed cases, and its escalation and exception policies. “Trust us” is not a Christian ethic. Donors do not need perfection; they need candor and verifiable process.

Grantmaking also needs a stewardship lens

Stewardship does not end once a grant is recommended. Donors should know how the sponsor confirms that recipients are legitimate charities, how it handles restricted gifts, and how it reduces the risk of funds supporting fraud or abuse. The modern nonprofit sector has experienced repeated failures of governance and accountability; Christian organizations are not immune. A faith-based DAF that treats diligence as optional is not practicing faith-based stewardship.

The IRS allows DAF sponsors to provide donors with advisory privileges while the sponsor retains legal control of funds. That structure can protect against self-dealing, but it also places moral weight on the sponsor’s governance. Donors should ask whether the sponsor’s controls and decision pathways make it easier to do what is right when pressures arise.

Accountability practices should be visible, not presumed

Many donors assume that because a DAF sponsor is Christian, it is automatically accountable. Scripture does not permit that assumption. The New Testament’s concern for financial integrity is explicit; Paul describes taking precautions so that “no one should blame us” in the administration of a gift (2 Corinthians 8:20–21). Accountability is part of Christian witness, not a concession to cynicism.

What strong accountability commonly includes

Donors should expect basic governance and financial practices that can be examined. This typically includes an independent audit (or, for smaller organizations, reviewed financials with clear justification), a functioning board with documented oversight, conflict-of-interest policies that are enforced, and grantmaking controls that prevent prohibited benefits and improper influence. It also includes clarity about fees, investment expenses, and any revenue-sharing arrangements with managers.

Where donors often struggle is translating “good intentions” into verifiable signals. That is one reason our team at Most Trusted evaluates ministries against The Most Trusted Standard, a 15-criteria framework that examines faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. The goal is not to replace relationships or pastoral counsel; it is to make trust more evidence-based, especially when giving decisions are complex.

The harder questions are often about transparency and outcomes

DAF sponsors can be transparent about internal governance while remaining vague about impact. For donors who care about stewardship, that is insufficient. Christians are not saved by results, but stewards are accountable for faithfulness, and faithfulness includes honest reporting about what happened after funds were deployed. Where outcomes are difficult to measure, the sponsor should say so plainly and explain what proxies it uses and why.

At the ministry level, the nonprofit sector has had to reckon with the “Overhead Myth”—the idea that low administrative costs automatically signal effectiveness. Charity Navigator, Candid (formerly GuideStar), and the BBB Wise Giving Alliance jointly warned donors that overhead ratios are a poor standalone measure and can incentivize underinvestment in governance and capacity Charity Navigator. Faith-based stewardship should be resistant to simplistic metrics, but it should still insist on meaningful disclosure.

Why pastors and donors must speak with clarity about DAF formation

Pastors often carry the burden of forming congregations in generosity while competing with cultural narratives of consumption and fear. Donor-advised funds can either reinforce a consumer mindset (“I control my giving portfolio”) or strengthen a biblical one (“I am accountable for entrusted resources”). The difference usually depends on whether pastors and church leaders teach DAFs as a discipleship tool rather than merely a tax tool.

Many congregants will never open a DAF, and that is not a spiritual deficiency. Yet for those who will, pastoral teaching can emphasize three disciplines: giving promptly when needs are clear, giving thoughtfully when complexities demand diligence, and giving humbly with accountability structures that protect both donor and recipient.

How donors can evaluate faith-based stewardship in a Christian DAF

Christians who want a DAF aligned with faith-based stewardship should evaluate it with the same seriousness they apply to the ministries they fund. The sponsor is not just a conduit; it is an institution that sets policies, holds assets, and exercises discretion. That institutional role deserves scrutiny.

Questions that reveal whether stewardship is substantive

- What is the sponsor’s theological posture toward stewardship? Is it articulated in a way that shapes real policies, or only aspirational statements?

- How are investment screens defined and governed? Are the criteria published? How are borderline cases handled? Who decides, and what accountability exists for those decisions?

- What does the sponsor disclose about fees and investment expenses? Is the total cost of ownership understandable, including underlying fund expenses?

- What controls exist around granting? How does the sponsor validate charities, handle restrictions, and prevent prohibited benefits?

- What reporting does the donor receive? Are grants and balances clear? Are there impact summaries where appropriate?

- How does the sponsor handle disputes and errors? Mature institutions plan for failure modes and document corrective action pathways.

Where donors should be cautious, even with Christian branding

Christian donors should be alert to vague claims of “faith-based investing” without published criteria, to unusually complex fee structures, and to sponsors that do not clearly separate donor advice from sponsor control. Caution is also warranted when a sponsor’s governance appears closely held—dominated by insiders, thin on independent oversight, or unwilling to share basic documentation.

Another common pressure point is donor intent across generations. A DAF can be a tool for family formation in generosity, but it can also become a contested asset if expectations are unclear. Donors should consider whether the sponsor provides clear successor policies, and whether those policies protect the charitable purpose rather than turning the fund into an intergenerational battleground.

For donors assessing the broader landscape of Christian Donor-Advised Funds, the essential task is not to find a perfect institution. It is to choose structures that make faithful stewardship more likely: institutions that can be examined, policies that are explicit, and practices that align with the moral contours of Christian discipleship.

Stewardship in a DAF should strengthen Christian accountability

A faith-based donor-advised fund can serve Christian donors well when it increases clarity rather than obscuring responsibility. The test is whether it encourages prompt generosity, disciplined governance, morally coherent investing, and transparent reporting that withstands scrutiny. When a DAF sponsor’s practices can be evaluated against clear standards—and when donors treat the tool as an instrument of discipleship rather than an instrument of control—faith-based stewardship becomes more than a label. It becomes a credible witness to the God who entrusts resources and calls stewards to give an account.