Tax and legal basics of Christian donor-advised funds are not a peripheral concern for serious stewardship. A donor-advised fund can be a clean way to give generously, reduce tax friction, and support long-term ministry commitments, but it also sits inside a regulatory framework with real constraints and real temptations. Christians who want their giving to be both faithful and orderly should understand what a DAF is, what it is not, and what the IRS actually enforces.

Scripture does not treat money as morally neutral. Jesus’s warnings about treasure and the heart (Matthew 6:19–21) are not in tension with prudent planning; they are a summons to integrity. The harder question for many donors is not whether a DAF is legal, but whether its convenience quietly shifts giving from worshipful surrender to personal control. Clear legal categories help us name those risks without suspicions or caricatures.

What a donor-advised fund is in the eyes of the law

A donor-advised fund is a charitable giving account held and controlled by a sponsoring organization, typically a public charity. The donor makes an irrevocable contribution, claims an income tax deduction if eligible, and then may recommend grants over time to other qualifying charities. The legal center of gravity is this: the donor advises, but the sponsor owns and controls the assets.

The IRS definition comes from Internal Revenue Code section 4966(d)(2), which describes a DAF as a separately identified fund or account owned and controlled by a sponsoring organization, where a donor has advisory privileges regarding distributions or investments. See IRS Donor-Advised Funds.

Irrevocable gifts and why that matters

When a contribution goes into a DAF, it is no longer the donor’s property. That irreversibility is not only a tax requirement; it is also a moral safeguard. If a donor can retrieve funds at will, the “gift” becomes an earmarked asset held for personal purposes, and the tax deduction becomes difficult to defend.

This is one reason Christian donors should be cautious about treating DAF balances as a personal ministry endowment. A DAF can support long-term generosity, but it should not become a private reserve insulated from accountability, church counsel, or real-time needs in the body of Christ.

Sponsoring organizations and how oversight differs

DAF sponsors include community foundations, financial institutions, and explicitly Christian sponsors. The legal rules apply across the board, but sponsor practices vary in grant approval, due diligence, and transparency. Some sponsors exercise substantial discretion and screening; others function with lighter review so long as the grantee is a recognized 501(c)(3) public charity and the grant is not used for prohibited purposes.

For donors who want to align giving with conviction, the sponsor’s policies on grant restrictions, international giving, and how they assess ministries matter as much as fee schedules. This is also where independent verification can serve donors well. Across our verification work at Most Trusted, we observe that ministries that meet The Most Trusted Standard tend to have clearer governance boundaries, stronger financial reporting discipline, and fewer avoidable compliance problems when receiving complex gifts.

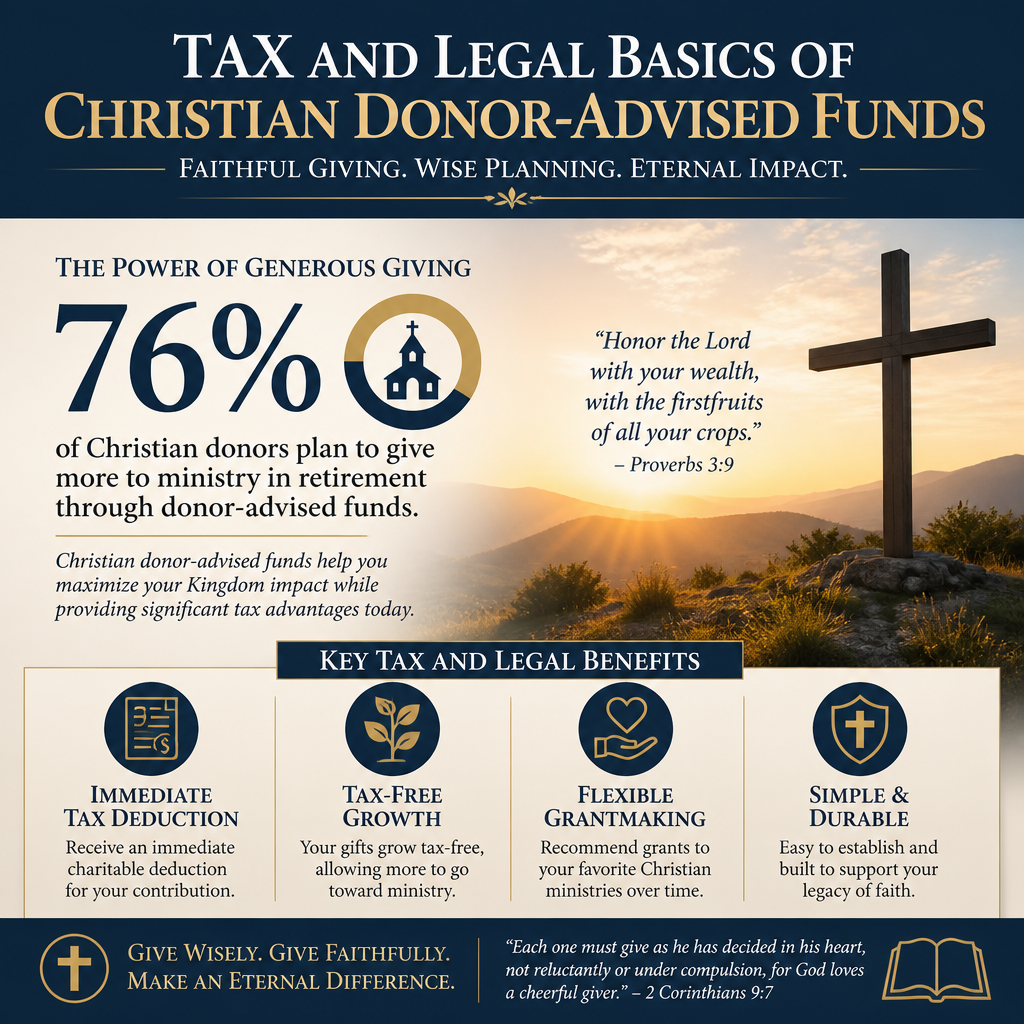

How DAF tax deductions actually work for Christian donors

The practical tax appeal of a DAF is straightforward: donors can separate the timing of their tax deduction from the timing of their grants. This can serve Christians whose generosity is steady but whose income fluctuates, or donors who want to respond quickly to emergencies without making hurried decisions about specific grantees.

The deduction happens at contribution, not at grant

In general, the charitable contribution deduction is tied to the moment the donor makes the irrevocable gift to the sponsoring organization. Grants made later are distributions from the sponsor, not new charitable contributions by the donor. That is the essential reason a DAF can “bunch” giving into a high-income year while sustaining support to ministries over multiple years.

Deduction limits depend on the type of property contributed and the nature of the recipient charity. For gifts to public charities, the IRS explains percentage limits and related rules in IRS Publication 526. DAF sponsors are typically public charities, but some contribution types can still trigger more conservative deduction treatment depending on asset type and valuation.

Itemizing, standard deduction, and the bunching strategy

Many Christian households no longer itemize because the standard deduction is substantial. The standard deduction for 2025 is $15,000 for single filers, $30,000 for married filing jointly, and $22,500 for heads of household, as published by the IRS. See IRS tax inflation adjustments. A DAF can make it possible to concentrate multiple years of giving into one year to exceed the standard deduction threshold, then recommend grants in subsequent years while taking the standard deduction.

This is morally neutral as a tool, but spiritually significant in its effects. Done well, it can protect ministry support during seasons of lower income. Done poorly, it can convert giving into a tax-driven transaction that becomes detached from prayer, accountability, and concrete responsibility to the local church and to neighbors in need.

Noncash gifts and capital gains complexity

DAFs are often used for appreciated assets such as publicly traded stock. The donor may avoid realizing capital gains and may claim a charitable deduction, subject to IRS rules. But the tax result depends on the asset type, holding period, and valuation requirements. Gifts of closely held business interests, real estate, or complex securities raise additional questions: qualified appraisals, sponsor acceptance policies, and liquidity constraints.

This is also where the line between sound stewardship and aggressive tax posture can blur. Christians who care about integrity should not treat “what is technically defensible” as the only ethical test. The governing principle is not maximization but faithfulness: gifts offered without deceit, and planning conducted without manipulation (Proverbs 11:1).

IRS rules that shape what a DAF can and cannot do

DAFs operate under rules aimed at preventing private benefit and maintaining the public character of charitable funds. These constraints are not arbitrary. They exist because charitable deductions represent foregone tax revenue, and the IRS expects public benefit, not disguised personal spending.

No personal benefit and no payback arrangements

DAF grants cannot be used to provide more than incidental benefits to donors or related persons. This includes, for example, payments that satisfy a donor’s personal pledge, or grants tied to goods and services that benefit the donor. Sponsors often require donors to affirm that no benefits will be received, and some will not process grants to certain types of events or memberships.

The IRS has addressed how charitable contributions interact with quid pro quo benefits and substantiation. The broader principle is captured in its guidance on charitable contributions and recordkeeping. See IRS Charitable Contributions. Christian donors should treat these restrictions as a prompt toward simplicity: let gifts be gifts, not leverage for recognition or access.

Grants must go to eligible recipients for charitable purposes

Most DAF grants are made to IRS-recognized 501(c)(3) public charities. Grants to individuals are generally prohibited unless made through carefully structured scholarship or assistance programs that satisfy detailed requirements and are administered by the sponsoring organization, not informally directed by the donor.

International giving requires additional care. Some sponsors will allow grants to U.S. public charities that operate internationally; others have specific equivalency determination or expenditure responsibility processes. These are not mere administrative hurdles; they are the legal mechanisms by which charitable dollars remain charitable rather than becoming private transfers.

Payout, warehousing concerns, and emerging regulation

Christians genuinely disagree about how long it is appropriate to hold funds in a DAF before granting. Some view long-term balances as prudent, especially for multi-year commitments or large, complex gifts. Others see “warehousing” as inconsistent with the urgency of need and the purpose of charitable deduction. Unlike private foundations, DAFs currently do not have a uniform federal payout requirement, though policy proposals have repeatedly surfaced.

Even without a statutory payout mandate, the ethical question remains. If a donor claims a deduction meant to advance public benefit, then delaying distribution should be a deliberate choice anchored in real ministry strategy, not indecision or a preference for control.

Legal prudence for ministry giving and why verification matters

Tax compliance does not guarantee ministry effectiveness, and ministry enthusiasm does not excuse weak governance. A DAF can distance donors from the lived realities of a ministry’s financial controls, board accountability, and reporting discipline because granting feels frictionless. Mature Christian stewardship brings the same seriousness to where funds go as to how they are deducted.

When it is wise to consult a tax attorney

Many DAF contributions are routine. But certain circumstances justify professional counsel: donating closely held business interests, significant real estate, cryptocurrency with complex basis records, contributions with retained rights, or any situation involving potential self-dealing or conflicts of interest. A tax attorney can also help donors think clearly about pledge language, event sponsorships, and any grant that could be construed as satisfying a personal obligation.

For donors with complex estates, DAFs also intersect with trusts, family foundations, and bequests. The aim is not complexity for its own sake. It is to ensure that generosity is ordered, truthful, and durable, especially when significant assets and public witness are involved.

How Most Trusted’s work fits alongside tax counsel

Attorneys and CPAs address legality and tax posture. Verification addresses credibility, governance integrity, and whether the stated mission is supported by verifiable evidence. At Most Trusted, we evaluate ministries against The Most Trusted Standard, a 15-criteria framework that examines faith commitments, financial integrity, governance and leadership, and transparency and effectiveness. That kind of diligence does not replace the donor’s spiritual discernment, but it does reduce avoidable risk and helps donors give with clear eyes.

What this means in practice is that donors can pair a tax-wise giving vehicle with a disciplined approach to selecting grantees. The goal is not cynicism. It is the kind of carefulness Paul commends when he describes taking pains to do what is right “not only in the Lord’s sight but also in the sight of man” (2 Corinthians 8:21).

DAFs and the Christian posture toward control

A DAF’s advisory feature can either serve humility or reinforce control. The distinction often shows up in how donors respond to being told “no” by a sponsor, how open they are to counsel from pastors and wise peers, and whether they treat ministry leaders as partners or as vendors. Christians are not required to give without strategy, but we are required to give without mastery over outcomes.

DAFs can also blur the role of the local church if donors begin to route all giving through a personal charitable account and neglect the ordinary, accountable support of their congregation. Christian donors should not assume that tax efficiency is the primary measure of stewardship. The New Testament places weight on integrity, mutual responsibility, and cheerful generosity shaped by grace (2 Corinthians 9:6–8).

Giving that is both lawful and faithful

Tax and legal basics of Christian donor-advised funds matter because Christians give under two kinds of scrutiny: the lawful scrutiny of the state and the spiritual scrutiny of the Lord who searches hearts. A DAF can serve the church and the world when it is used as a channel for timely, accountable generosity rather than a storehouse for postponed obedience.

For donors who want to go deeper on the practical and spiritual dimensions of these accounts, we address the broader landscape of Christian Donor-Advised Funds with the same commitment to clarity, evidence, and integrity that shapes our verification work at Most Trusted.