How Christian donor-advised funds avoid harmful industries is not a secondary question for serious Christian donors. It is a stewardship question about complicity, witness, and whether resources set apart for the Lord are being used, even indirectly, to profit from what Scripture calls evil.

Christian donors also know the modern reality: most money sits somewhere between the moment it is given and the moment it is granted. A donor-advised fund is not only a charitable tool; it is a holding vehicle. The harder question is what happens to those assets while they wait, and whether “waiting” quietly becomes participation in industries that harm neighbor, degrade human dignity, or normalize vice.

Why investment alignment is a discipleship issue, not a niche preference

Money is never morally neutral in Scripture

Scripture does not treat wealth as an indifferent substance that becomes “spiritual” only when it reaches a ministry. Jesus repeatedly ties money to the heart, to loyalty, and to the realities of worship and service (Matthew 6:24; Luke 16:13). That is why Christian donors often feel a specific unease when they discover that charitable dollars may be invested in predatory lending, pornography, gambling, or companies whose business model depends on addiction.

Christians genuinely disagree about where lines should be drawn. Some treat screening as a matter of conscience akin to Romans 14; others emphasize structural complicity and call for stricter separation. What rarely remains contested is the underlying moral intuition: a Christian should not seek financial gain from another person’s harm, even if the gains fund good works.

A DAF creates a stewardship “in-between” that must be governed

A donor-advised fund concentrates the stewardship question because the donor’s gift is typically invested before it is granted. If the DAF’s investment menu defaults to broad market funds, donors may unintentionally own small slices of industries they would not knowingly support. That is not a call to panic; it is a call to govern the “in-between” with the same seriousness we bring to the grant itself.

For donors comparing options across Christian Donor-Advised Funds, the practical question is straightforward: does the sponsor offer investment approaches that attempt to avoid harmful industries, and are those exclusions defined, disclosed, and implemented with integrity?

What it means to avoid harmful industries, and why definitions matter

Common exclusion categories and the theological logic behind them

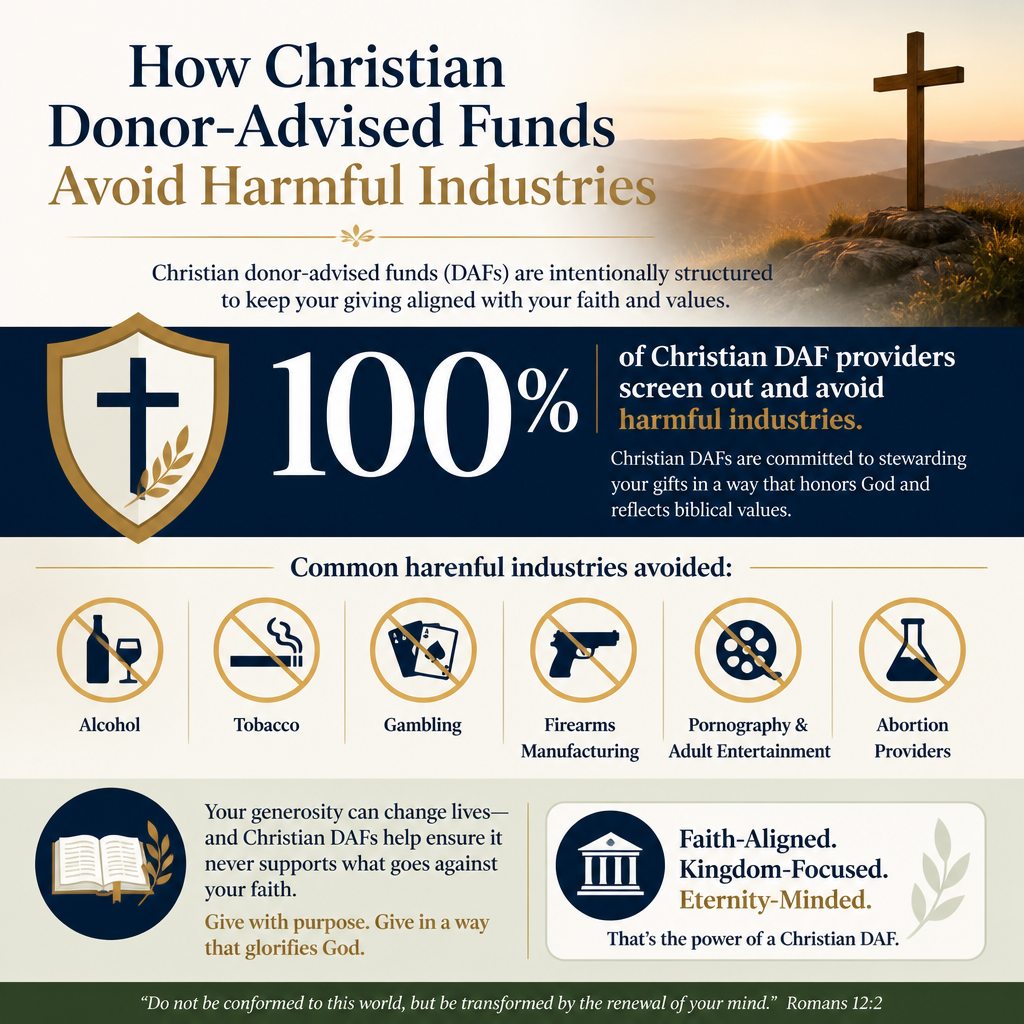

Most Christian DAF sponsors that pursue values-based investing use negative screens: explicit exclusions applied to the portfolio. The typical rationale is not moral superiority; it is moral coherence. Christians aim to give in a way that does not depend on revenue streams built on exploitation, coercion, or the deliberate cultivation of destructive appetites.

A short list of common screened areas includes the following:

- Abortion providers and businesses materially involved in abortion services

- Pornography and sexually explicit content businesses

- Gambling enterprises

- Tobacco and nicotine products

- Weapons categories beyond lawful defense and toward indiscriminate harm

These categories are not identical across sponsors. “Weapons,” for example, may be limited to controversial weapons or may extend to broader defense manufacturing. “Adult entertainment” can be defined narrowly (explicit content production) or broadly (platforms with substantial explicit-content revenue). A sponsor’s policy is only as meaningful as its definitions.

The contested edge cases donors should not ignore

Some industries are easier to name than to screen consistently. Alcohol is a recurring example: Scripture condemns drunkenness while allowing wine; Christians differ on whether the appropriate response is personal moderation or institutional exclusion. Cannabis businesses, gaming and online betting, and social media platforms implicated in sexual exploitation also produce legitimate debate about the difference between primary business purpose and downstream misuse.

Because these edge cases are real, donors should treat “faith-based investing” claims as hypotheses that require verification. Mature stewardship does not confuse aspiration with implementation.

How Christian DAFs implement screens in practice

Investment menus, model portfolios, and the screen behind the label

Most DAF sponsors operationalize exclusions through a defined set of investment options. Some provide a suite of faith-screened funds or models; others permit only a limited menu chosen by the sponsor’s committee; a few allow more customization through approved advisors or separately managed accounts.

Two practical realities often surprise donors. First, a sponsor can offer a “Christian” or “values” option that is still built on third-party funds with varying screen rigor. Second, a sponsor may rely on an index provider or ESG methodology that does not map neatly onto Christian moral concerns. ESG can reward corporate policies unrelated to the Christian moral imagination, and it can fail to address industries of particular concern to Christian donors. Donors should ask whether the screen is explicitly Christian in its exclusions, not merely “responsible” in generic terms.

Cash, sweeps, and interim holdings can undermine intent

A less discussed issue is what happens to uninvested cash. Some sponsors use cash “sweep” vehicles, money market funds, or bank deposits. If a DAF sponsor has a strong exclusion policy for equities but a weak approach to cash management, the stewardship problem can simply relocate rather than disappear. Donors should ask what instruments hold idle cash and whether those instruments follow the same moral commitments.

What donors should ask a sponsor before opening a fund

Questions that reveal whether screens are real or rhetorical

Christian donors do not need to become investment analysts to ask clear, governing questions. The sponsor should be able to answer in writing, with enough specificity to allow meaningful comparison across providers.

We recommend asking:

- What industries are excluded, and how are they defined?

- What threshold triggers an exclusion: any involvement, or a revenue percentage?

- Who provides the screening data, and how often are holdings reviewed?

- Do the screens apply to all asset classes offered, including cash and fixed income?

- Can donors view current holdings or receive periodic holdings reports?

Thresholds matter because many screens are not absolute. A fund may exclude companies with more than a stated percentage of revenue from certain activities. That approach can be reasonable, but it should be disclosed plainly because the moral meaning changes. “Avoid” can mean “minimize exposure,” not “zero exposure,” and donors deserve to know which is being promised.

Cost, tracking error, and concentration are real trade-offs

Exclusions can increase expense ratios, reduce diversification, or create tracking error against broad market indices. Donors should not be shamed into ignoring these trade-offs, nor should they accept them without scrutiny. The question is whether the sponsor is candid about the costs and whether the donor’s goals justify them.

Theologically, Christians are not called to maximize returns at any moral cost. Yet Scripture does commend prudence, planning, and wise administration (Proverbs 21:5). A sponsor that treats faith alignment as an excuse for avoidable sloppiness does not honor the donor, and it does not honor the Lord.

Verification, transparency, and the stewardship integrity donors should demand

Avoiding harmful industries is part of a larger trust question

For many donors, investment alignment is one element of a larger concern: can we trust the institutions that handle charitable assets and represent Christian commitments? DAF sponsors often sit at the intersection of theology, finance, and nonprofit practice. That intersection can be healthy, but it can also create incentives to market “faith-based” language without providing commensurate transparency.

At Most Trusted, our work focuses on independent verification of Christian nonprofits so donors can give with confidence. While our primary evaluations are designed for ministries rather than financial products, the same disciplines of trust apply: clear doctrinal commitments that are not merely symbolic, financial integrity that can be tested, governance that is accountable, and transparency that does not depend on persuasion.

What The Most Trusted Standard clarifies for grantmaking decisions

Even when a sponsor’s investments are well-screened, donors still face a second stewardship duty: ensuring that the ministries receiving grants are worthy of trust. Misalignment can appear on the recipient side as readily as on the investment side—especially when donors give quickly in response to crisis appeals, emotionally charged storytelling, or celebrity endorsements.

The Most Trusted Standard is our 15-criteria framework that examines faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. Donors who grant from a DAF are often giving at higher volume and with more strategic intent; that makes disciplined verification more necessary, not less. When donors want to approach this with consistent Christian seriousness, the broader field of Faith-Based Stewardship in Christian Donor-Advised Funds provides a vocabulary for asking better questions of both sponsors and recipients.

FAQs for How Christian donor-advised funds avoid harmful industries

Do Christian donor-advised funds guarantee zero exposure to harmful industries?

Not always. Many Christian DAF sponsors offer screened investment options that aim to avoid certain industries, but the rigor depends on definitions, thresholds, data sources, and how frequently holdings are reviewed. Some options may reduce exposure rather than eliminate it entirely, especially when using pooled funds, indexes, or third-party managers.

Is using ESG funds the same as Christian values-based investing in a DAF?

No. ESG is a broad framework that often evaluates environmental, social, and governance factors through nonreligious criteria that may not address distinctively Christian concerns such as pornography, abortion, or gambling. Some ESG funds may overlap with Christian exclusions, but donors should confirm whether the screen is explicitly defined around the industries they intend to avoid.

A coherent witness requires coherent stewardship

Christian donors open donor-advised funds because they want disciplined generosity: planning, tax efficiency, and grantmaking that can endure. That same discipline should govern the assets while they are invested. Avoiding harmful industries is not a performance of purity; it is a refusal to finance what harms the neighbor in the name of helping the neighbor.

The most credible sponsors will define exclusions clearly, disclose their methods, acknowledge trade-offs, and invite scrutiny. For mature Christian donors, that is not an inconvenience. It is part of what it means to give in a manner worthy of the gospel we confess.