Family and legacy giving through Christian donor-advised funds raises a question many faithful households eventually face: how do we turn a lifetime of generosity into a durable pattern of discipleship after we are gone. A Christian DAF can serve as an account, a set of permissions, and a set of habits. It can also become a quiet battleground of family dynamics, theological differences, and unfinished estate planning if those realities remain unnamed.

Christian donors often want more than tax efficiency. We want continuity: the ability to fund gospel work steadily, to teach children what stewardship looks like, and to keep generosity tethered to the church’s mission rather than to the news cycle. The challenge is that money tends to reveal what we love, and it exposes what we have not talked about. Jesus’ warning that “where your treasure is, there your heart will be also” (Matthew 6:21) is not a pious aside; it describes how financial authority and spiritual formation stay linked across generations.

Why Christian families choose donor-advised funds for legacy giving

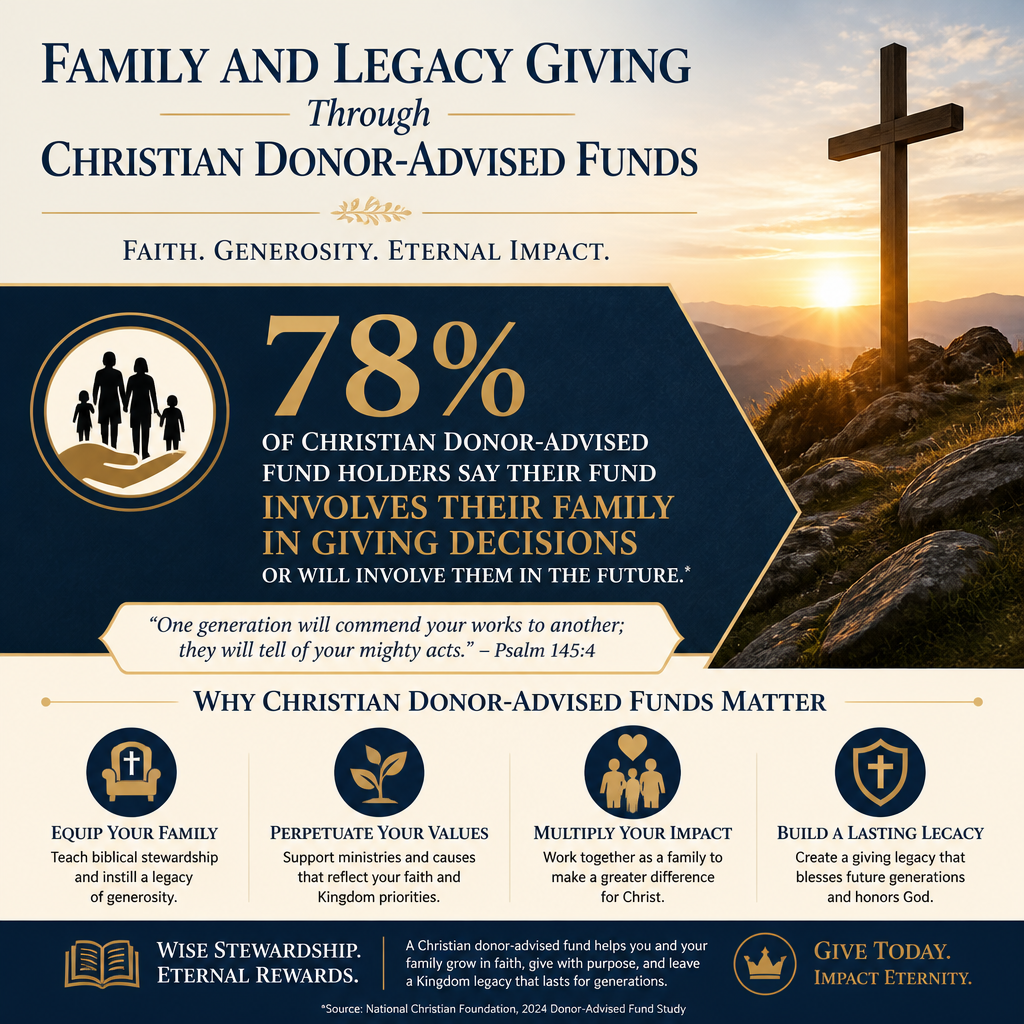

Families usually arrive at a Christian donor-advised fund because they want a faithful structure for giving that outlasts a single season. The DAF can receive appreciated assets, support annual grantmaking, and create an orderly way to involve spouses and children. Yet the deepest motivation is often spiritual: to build a household culture where generosity is normal, discussed, and accountable.

What this means in practice is that a DAF can function like a family giving table. It creates a recurring moment to ask: What is the Lord calling us to support, and why? A DAF’s administrative simplicity can free attention for discernment—if the family actually uses the space for discernment rather than defaulting to habit or sentiment.

Formation, not merely funding

Christian legacy giving tends to go wrong when we treat giving vehicles as morally neutral containers. The account may be neutral; the formation is not. A DAF can unintentionally teach children that generosity is a private hobby, detached from the local church, or that charity is primarily a brand preference. A well-governed family process can teach the opposite: that giving is worship, that the poor are not projects, and that ministries should be evaluated for faithfulness and integrity.

Even broad patterns of generosity in the American church show why formation matters. Average giving among U.S. churchgoers is commonly reported in the low single digits as a share of income; one widely cited synthesis puts it at about 2–3% for many Christians, a figure frequently discussed by research organizations and church finance analysts such as Barna. Because estimates vary by dataset and definition, we treat the exact percentage with caution, but the pastoral point remains: drift is common, and households rarely become generous by accident.

Stewardship constraints can be a gift

A DAF is not the only way to leave a legacy. Some families prefer direct bequests to churches and ministries, charitable trusts, or foundations. Christians genuinely disagree about whether DAFs encourage “warehousing” charitable resources or whether they provide prudent pacing for volatile markets and complex giving. That tension is real.

What is often missed is that constraint itself can serve discipleship. A DAF’s policies about grants, eligible recipients, and successor decision-making can protect the family from impulsive giving and from being manipulated by persuasive fundraising. A clear structure does not guarantee wisdom, but it can prevent predictable failure modes.

Building a shared family practice without turning generosity into a power struggle

The hardest question in family giving is not technical. It is relational and theological: who gets to decide, and what are the non-negotiables. A Christian DAF can include multiple advisors, recommend grants over time, and name successors. Without explicit agreements, those features can magnify conflict rather than reduce it.

Start with a common theological center

When families attempt “values-based” giving without a theological center, values become a substitute for doctrine. For Christian households, the center is clearer: the lordship of Christ, the authority of Scripture, and the Church’s mission to make disciples while practicing mercy. That does not settle every downstream question, but it does set boundaries. It also gives adult children a framework that is not merely sentimental: giving is a response to grace, not a way to purchase meaning.

Many families benefit from writing a brief giving statement that names (1) what kinds of ministries are in scope, (2) what doctrinal commitments matter, and (3) what practices are disqualifying (for example, chronic lack of financial disclosure or refusal to answer basic governance questions). A DAF can hold money; it cannot hold conviction unless the family makes conviction explicit.

Give children real agency with real limits

Inviting children into DAF giving can be fruitful, but token participation teaches cynicism. Mature families often do better with defined lanes: a portion of annual grants that children can recommend, guardrails about eligible recipients, and a predictable rhythm for proposals and discussion. The goal is not to run a miniature grant committee for its own sake. The goal is to train discernment: how to listen, how to ask hard questions, and how to weigh competing needs without performing generosity.

Agency also requires clarity about the difference between a family’s DAF and a child’s personal giving. Some adult children will want to support causes that the parents cannot conscientiously endorse. It is usually better to acknowledge that divergence honestly than to force unanimity. Christian unity is not the same as aesthetic agreement, and family harmony purchased by silence tends to fail under pressure.

Verification protects relationships as well as resources

Disagreements about ministries often mask a simpler dispute: which information sources are trustworthy. This is where independent verification can serve family unity. Most Trusted evaluates Christian nonprofits against The Most Trusted Standard, a 15-criteria framework that examines faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. When a family can point to a shared set of criteria rather than to personal impressions, the conversation becomes less accusatory and more accountable.

Across our verification work, we observe that ministries with strong governance and candid disclosure tend to weather leadership transitions and fundraising shocks more faithfully than ministries that depend on a charismatic founder and thin reporting. Those patterns matter for legacy giving because families are not only choosing a cause; they are choosing a stewardship partner.

Planning for death, successor advisors, and estate alignment

Legacy intentions collapse when the account outlives the clarity. A DAF does not automatically translate a donor’s convictions into a successor’s practice. The handoff must be designed. Most DAF sponsors allow you to name successor advisors or successor charitable recipients, but the options and constraints differ by provider, and Christian donors should read those policies with care.

What happens to a Christian DAF at death

At a donor’s death, the DAF sponsor typically looks to the account’s legal paperwork: successor advisors, secondary successors, or default charitable beneficiaries. If none are named, sponsors often apply a default policy that may distribute funds according to internal procedures. That outcome may be perfectly charitable and still be misaligned with what the donor intended.

Because the DAF is not the same as a will or trust, donors should confirm how their DAF integrates with their broader plan. Families frequently assume their estate documents “cover everything,” but DAF succession is usually governed by the sponsor’s forms. Coordinating these instruments is not busywork; it is a stewardship responsibility.

Naming successor advisors is a spiritual decision

Choosing a successor is not only about competence. It is about spiritual stability. The successor will inherit decision rights over charitable resources, and decision rights shape formation. Donors should consider a successor’s church commitments, doctrinal clarity, track record of generosity, and willingness to engage in due diligence. It is reasonable to name co-successors to prevent unilateral drift, but co-successors can also deadlock without a tie-break process.

The tension is that some donors want to “lock in” giving priorities indefinitely, while others want to give successors room to respond to future needs. Christians can differ here in good faith. A wise approach often balances both: a defined set of enduring priorities (gospel proclamation, local church health, mercy and justice consistent with Scripture) and a discretionary portion for emergent opportunities.

Aligning the DAF with your will and attorney counsel

Estate planning attorneys rightly ask whether a DAF is the best receptacle for a particular asset and whether the donor has understood the control implications. A DAF is irrevocable once contributed. It offers advisory privileges, not personal ownership. For some families, that is a protection; for others, it feels like a loss of control. The counsel should be candid.

For donors who want to integrate DAF succession with the rest of their estate, coordination is essential: beneficiary designations, charitable bequests, and any family foundation governance should not contradict each other. Donors should also confirm whether their chosen DAF sponsor permits specific types of grants and whether there are faith-based restrictions that match the family’s intent. For broader context on selecting and governing these accounts, see Christian Donor-Advised Funds.

Choosing ministries your heirs can trust

A legacy plan is only as durable as the ministries it supports. Donors sometimes assume that a ministry’s fruitfulness is self-evident, but mature donors know that outcomes can be difficult to measure, and that moral failures and governance breakdowns are not rare. The question is not whether risk exists, but whether it is managed with integrity.

Transparency is not the same as effectiveness

Some ministries report extensively and still struggle to demonstrate durable impact. Others do meaningful work in difficult contexts where measurement is genuinely complex. Christian donors should resist simplistic scorekeeping. At the same time, “ministry is hard to measure” is sometimes used as a shield against basic accountability. Both errors are common.

We encourage donors to ask for ordinary evidence: audited financials when appropriate, clear leadership structures, conflict-of-interest policies, a coherent theology of ministry, and honest reporting about what is working and what is not. This aligns with the broader field’s recognition that overhead ratios are a poor proxy for quality. The joint letter known as the Overhead Myth, signed by major evaluators, argued that focusing on overhead can do harm and distract from effectiveness; see Charity Navigator for a primary organizational reference to that position.

Faithfulness includes governance

Christian donors sometimes treat governance as a secular concern, separate from “spiritual” ministry. Scripture does not allow that split. The New Testament’s qualifications for leaders emphasize character, reputation, and stewardship (1 Timothy 3). Financial controls, independent boards, and candid disclosure are not faith-neutral; they are practical expressions of accountability before God and neighbor.

Across our work at Most Trusted, we find that donors gain confidence when they can see who leads a ministry, how decisions are made, how conflicts are handled, and whether results are described with appropriate humility. These are not secondary matters for legacy giving, because heirs will often inherit not the original donor’s relationships but only the record the ministry has made available.

Legacy giving as discipleship across generations

Family and legacy giving through Christian donor-advised funds works best when the DAF is treated as a tool serving a larger spiritual purpose: to cultivate a household that loves what Christ loves and gives accordingly. The administrative conveniences of a DAF can support that purpose, but they cannot replace the conversations that legacy requires.

When donors name successors carefully, align the DAF with estate documents, and establish a shared standard for ministry trustworthiness, the account becomes more than a holding vehicle. It becomes a means of continuity—one that helps heirs practice generosity with clarity, humility, and accountability before God.