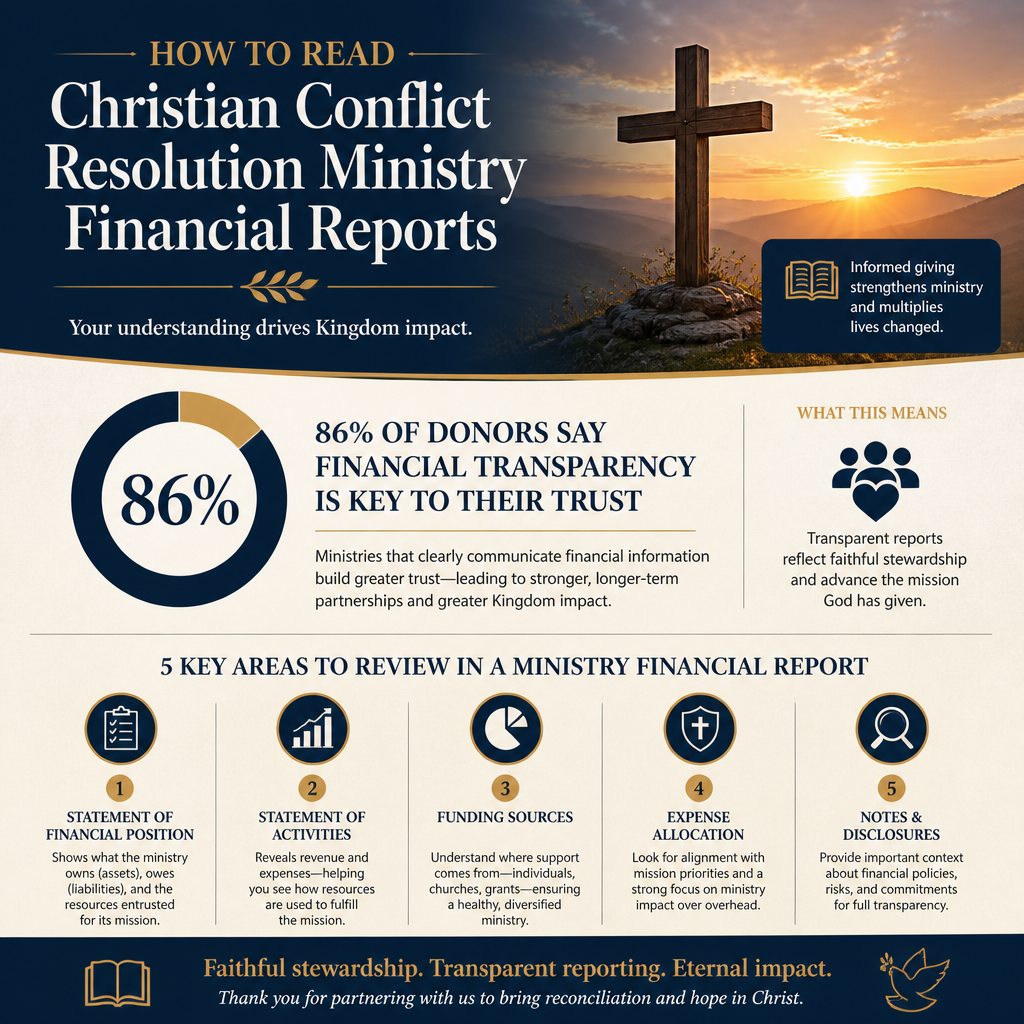

Learning how to read Christian conflict resolution ministry financial reports is not an exercise in suspicion. It is an act of stewardship. When a ministry claims to serve churches and families in crisis, its financial reporting should show the same commitment to truth, clarity, and repair that it urges upon others.

Conflict resolution work is often quiet by design. Many cases are confidential. Outcomes are not always measurable in public ways. Those realities make donor due diligence more demanding, not less. Mature giving asks for candor about limits, careful reading of what is disclosed, and a willingness to ask for what is not.

Start with the ministry model before you start with the numbers

Financial reports are intelligible only in light of the ministry’s actual work. A Christian conciliation organization that trains elders will look different from a ministry that conducts mediations, provides counseling referrals, or offers restorative processes after abuse. The accounting should match the stated mission and the operational model.

Identify what the ministry actually delivers

Begin by naming the ministry’s “product,” even if it is not sold in a commercial sense: training hours, coaching, mediation services, case administration, content production, or church consulting. A credible report will tie expenses and staffing to those deliverables with straightforward explanations.

What this means in practice is that donors should expect a coherent line from mission statement to program description to spending categories. If the ministry describes itself as field-based and relational, but financials show most costs in media production with minimal program staff, that mismatch deserves questions.

Clarify who pays and why that matters

Many conflict resolution ministries are funded by a mix of donations, training fees, retainers from churches, and sometimes book or resource sales. Each revenue stream carries incentives. Fee-based services can strengthen discipline and focus; they can also create pressure to prioritize paying clients over harder cases. Donor-funded services can protect access for the financially strained; they can also create opacity if the ministry treats donors as the audience and churches as the “customers.”

When reviewing a ministry in the wider ecosystem of Christian Conflict Resolution Ministries, we recommend explicitly mapping the revenue model to the ministry model before drawing conclusions from any single ratio.

Read the Form 990 and audited financials with different expectations

For U.S. nonprofits, the IRS Form 990 is often the most accessible financial document, but it is not designed to answer every donor question. Audited financial statements, when available, are stronger for assessing overall financial position and accounting practices. Each document has strengths, and sophisticated donors use both when they can.

What the Form 990 is reliable for

The 990 helps donors examine governance signals, compensation disclosure, major revenue categories, and how the organization describes its programs in Part III. It also provides a standardized view across ministries. The IRS requires tax-exempt organizations (with limited exceptions) to make certain returns publicly available, which is why the 990 has become a common accountability tool (IRS).

Donors should read Part I and Part III together: the summary numbers and the narrative of what was accomplished. If the narrative reads like marketing copy without concrete program detail, treat that as a transparency indicator, not merely a writing style choice.

What audited financials are reliable for

Audited financial statements (and their notes) are typically better for understanding cash, reserves, liabilities, revenue recognition, and restricted funds. They also signal that the board has agreed to external scrutiny. An audit is not a guarantee of virtue, but it is a meaningful procedural discipline.

Be careful with the absence of an audit. Smaller ministries may legitimately lack the scale to justify the cost. Larger ministries with complex finances and no audit should be prepared to explain why, and what alternative controls exist.

Trace the story of revenue, not only the ratio of expenses

Expense ratios have been overused in donor culture. The field has worked to correct simplistic thinking about “overhead” because under-investing in administration can create fragility, compliance risk, and ethical failure. The joint statement often called the “Overhead Myth” reflects that concern and is endorsed by major evaluators, including Charity Navigator and BBB Wise Giving Alliance (Charity Navigator).

For conflict resolution ministries, the more revealing question is whether revenue is stable, appropriately diversified, and honestly presented.

Look for concentration and dependency

A ministry funded primarily by one or two donors is not automatically unhealthy, but it is exposed. Donors should check whether the report discloses major donor concentration, whether the board discusses contingency planning, and whether the ministry’s budgeting assumptions are sober.

Similarly, a ministry funded largely by conference revenue may be vulnerable to disruptions. This became plain across the nonprofit sector during the COVID-19 era; revenue concentration is not a theoretical risk.

Restricted gifts and designated funds should be intelligible

Conflict resolution work sometimes includes scholarship funds for training, subsidized services for low-income churches, or special initiatives after public crises. Those gifts are often restricted. The financial statements should distinguish restricted from unrestricted funds and explain how restrictions are honored.

When donors cannot tell whether restricted funds are being used as intended, trust becomes difficult to sustain. A ministry committed to reconciliation should not treat financial clarity as an adversarial demand.

Interpret program spending with the ministry’s ethics in view

In reconciliation work, “program” is not only a category; it is a moral claim. If a ministry teaches truth-telling, impartiality, and accountability, then donors should expect the financial report to support those commitments with credible internal controls and disclosure practices.

Staffing patterns often explain the real allocation

Conflict resolution ministries are often labor-intensive. Skilled staff time is the primary input. Donors should examine the mix of program staff, administrative staff, and fundraising staff, and whether compensation is transparently disclosed and consistent with organizational scale.

The Form 990 can help here because it lists key employees and certain compensation details. If the ministry’s narrative emphasizes front-line work but staffing costs are largely administrative or executive, donors should ask how “program” is defined and allocated.

Travel, hospitality, and case costs need context

Some reconciliation work requires travel to churches, denominational meetings, or crisis sites. Hospitality can be legitimate in ministry settings, but it also can be abused. The best reporting provides context: why travel is necessary, what policies govern it, and how expenses are approved.

Across our verification work at Most Trusted, the ministries that meet The Most Trusted Standard tend to document policies that keep ordinary expenses ordinary: clear approval thresholds, board oversight for executive spending, and consistent treatment of reimbursements. These are not glamorous disciplines, but they keep a ministry credible when tensions rise.

Use transparency signals to decide what questions to ask next

Financial reports rarely answer every question a donor should ask, especially in ministries where confidentiality is central. A wise donor reads reports as one piece of a broader integrity picture that includes governance, doctrinal commitments, grievance handling, and evidence of outcomes that can be shared without violating trust.

A short set of questions that often clarifies the picture

- Do we see a clear connection between stated programs and the largest expense categories?

- Is revenue diversified enough to withstand the loss of a major donor or a major event?

- Are restricted funds clearly described and visibly honored in the financial statements?

- Does the ministry disclose board members, key policies, and conflicts-of-interest practices?

- Is the ministry candid about what cannot be disclosed due to confidentiality, and does it offer alternative accountability?

Christians genuinely disagree about how much information donors should expect when a ministry’s work involves private disputes, pastoral discipline, or allegations of wrongdoing. Some argue that confidentiality requires minimal disclosure; others argue that confidentiality must be paired with stronger governance transparency precisely because the work is hidden. The wise path is not maximal disclosure at any cost, but demonstrable accountability with appropriate boundaries.

Where to look beyond the numbers

Because reconciliation work touches power dynamics, donors should look for evidence that the ministry has mechanisms for handling complaints, safeguarding the vulnerable, and correcting errors. A financial report will not fully show that. A transparent ministry, however, will point donors to governance documents, policy summaries, and clear lines of responsibility.

This is where category-level expectations matter. Within Accountability and Transparency in Christian Conflict Resolution Ministries, donors typically find that the strongest organizations treat transparency as part of ministry fidelity, not as a concession to modern skepticism.

FAQs for How to read Christian conflict resolution ministry financial reports

Should we prioritize low overhead when giving to a conflict resolution ministry?

We should prioritize integrity and capacity, not merely low overhead. Conflict resolution ministries often require experienced staff, careful administration, and documented processes. The sector has recognized that overhead ratios can be misleading, which is why major evaluators have warned against using overhead as a primary measure of nonprofit performance (Charity Navigator). A better approach is to assess whether spending matches the ministry’s stated work and whether governance and controls support faithful practice.

What if a ministry cannot share outcomes because cases are confidential?

Confidentiality can be legitimate, but it does not remove the obligation to be accountable. We recommend looking for alternative forms of verification: anonymized outcome summaries, third-party evaluations, board-level oversight descriptions, documented policies for complaints and conflicts of interest, and audited financials or reviewed statements when appropriate. A ministry committed to truth should be able to explain what it can disclose, what it cannot, and what safeguards stand in place either way.

Stewardship that fits the work of reconciliation

Christian conflict resolution ministries ask others to tell the truth, submit to wise process, and pursue repair rather than triumph. Donors have standing to ask for the same virtues in financial reporting. When a ministry’s reports are coherent, appropriately detailed, and governed by clear controls, donors can give with confidence that generosity is strengthening peace rather than funding confusion.