How to give required minimum distributions to apologetics ministries is, at its core, a stewardship question: how to meet a legal obligation with moral clarity, and how to direct taxable assets toward gospel work without weakening the rest of a household’s giving. For many Christian donors, the practical problem is not willingness. It is the burden of complexity—custodians, IRS rules, ministry eligibility, and the quiet fear of making an avoidable mistake.

Apologetics ministries sit in a particular place in the Christian ecosystem. They fund scholarship, public reasoned witness, campus engagement, publishing, media, and pastoral support for the church’s evangelistic and discipleship calling. That work can be profoundly fruitful, and it can also be difficult for donors to evaluate because outputs are not as easily counted as meals served or beds provided. That is precisely why RMD giving requires both competent tax execution and careful discernment about ministry credibility and accountability.

Required minimum distributions are not merely a tax event

What the IRS requires and what stewardship requires

Required minimum distributions are mandatory withdrawals from certain retirement accounts after a donor reaches the applicable age under federal law. If an RMD is not taken in the required amount and timeframe, the tax consequences can be severe. The IRS explains the basic RMD rules, including timing and calculation mechanics, in its retirement plan guidance and related publications at IRS Retirement Plans.

For Christian donors, however, the question rarely ends with compliance. Scripture consistently treats wealth as entrusted, not possessed. Jesus’ teaching on treasure and the heart presses beyond legality to love rightly ordered (Matthew 6:19–21). What this means in practice is that an RMD can become a disciplined act of giving that strengthens the church’s witness rather than a reluctant withdrawal that simply increases taxable income.

Why qualified charitable distributions matter

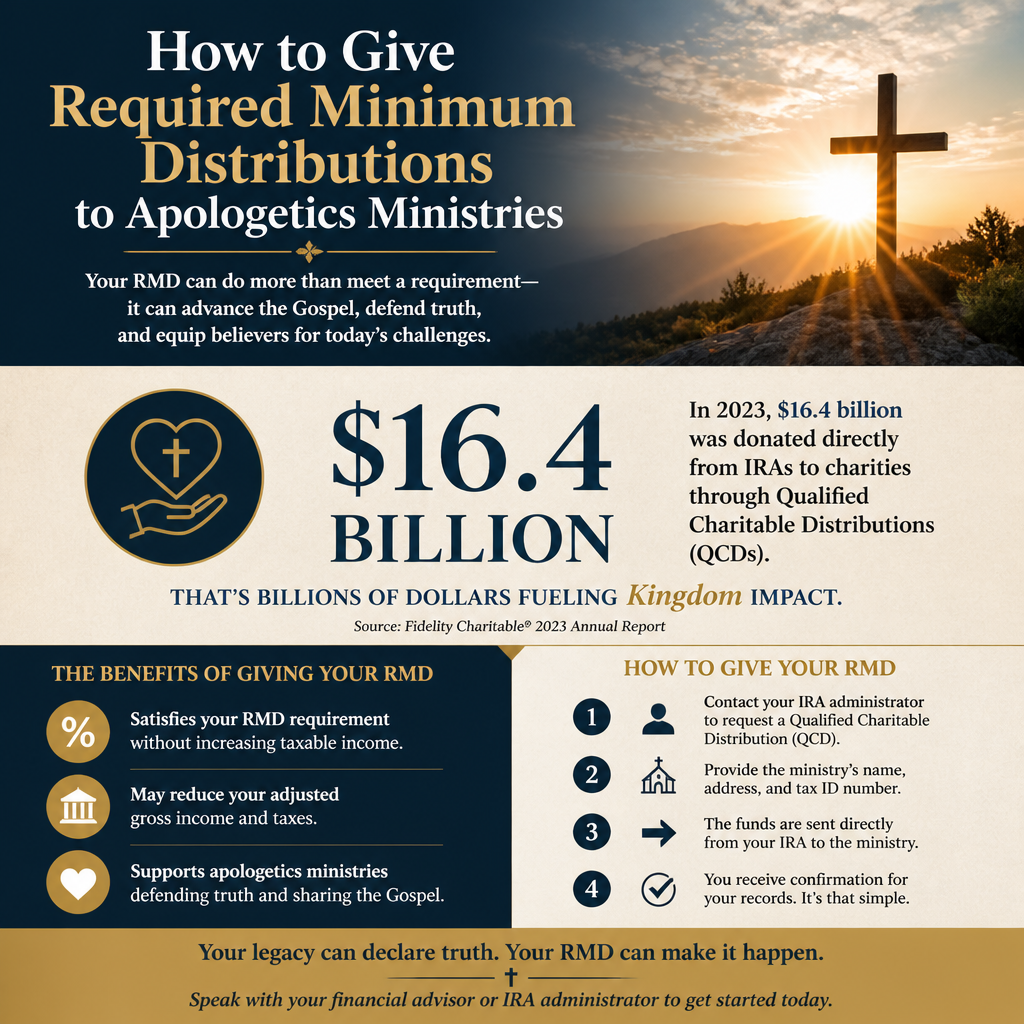

For donors who are eligible, a qualified charitable distribution (QCD) can allow IRA assets to be transferred directly to a qualified charity in a way that can reduce taxable income. This is often the cleanest way to align an RMD obligation with charitable intent. The IRS addresses QCD rules and limitations in its QCD guidance, including eligibility, dollar limits, and what counts as a qualified recipient, at IRS Qualified Charitable Distributions.

Christians genuinely disagree about how much tax efficiency should drive giving decisions. Some prefer a simpler posture: give generously, pay what is owed, and avoid elaborate planning. Others see careful tax planning as a legitimate form of stewardship that frees resources for ministry. The moral center is not the mechanism. The question is whether a household’s approach increases faithfulness, honesty, and generosity rather than serving as an excuse for control or self-protection.

Choosing the right channel for giving your RMD

Direct IRA-to-ministry gifts are usually the cleanest

If you want your RMD to support apologetics work, the first decision is the channel. For eligible donors, a QCD is typically the most straightforward because the distribution goes directly from the IRA custodian to the ministry, reducing the chance that the withdrawal will be treated as taxable income. That directness also tends to reduce administrative ambiguity: the gift is documented as coming from the IRA, and the donor receives the ministry’s acknowledgment.

Not every retirement account supports QCDs, and not every gift arrangement is compatible with them. A QCD must go to an eligible public charity. It generally cannot be made to a donor-advised fund or private foundation. These limitations are not bureaucratic trivia; they protect both donor and ministry from unintended noncompliance.

When taking the RMD and giving cash may be appropriate

Some donors will not be eligible for QCDs, or they may have giving priorities that require flexibility. In those cases, a donor can take the RMD as income and then give from other assets. That approach can still be faithful stewardship, but it changes the tax picture. It may also increase the need for recordkeeping discipline so the donor’s charitable deduction is properly substantiated.

Across our verification work at Most Trusted, we observe that administrative clarity is a quiet predictor of long-term ministry health. Ministries that meet The Most Trusted Standard tend to have well-defined gift acceptance practices, clear receipting, and governance controls that reduce avoidable donor confusion. That matters for any gift, but it matters especially when the donor is using a legally constrained mechanism like an RMD.

- Confirm the account type and your eligibility for QCD treatment with your custodian.

- Verify the ministry’s legal status as a qualified public charity before initiating the transfer.

- Initiate the transfer early enough to clear before year-end deadlines.

- Request proper gift acknowledgment and retain it with your tax records.

- Coordinate with a tax professional when your giving involves multiple accounts or beneficiaries.

Evaluating apologetics ministries before you send retirement assets

Apologetics effectiveness is real but not always easily measured

Apologetics is often criticized for being overly intellectual, or for winning arguments without winning people. Those critiques have substance when apologetics becomes a substitute for evangelism, prayer, repentance, and embodied love. At the same time, apologetics has served many believers who were near the edge of disbelief, and it has strengthened churches facing aggressive secular catechesis. Donors should not demand simplistic metrics, but we should demand integrity, theological seriousness, and accountable stewardship.

What this means in practice is that donors can ask disciplined questions: Is the ministry accountable to a biblically faithful local church or a credible board? Does it represent orthodox Christianity honestly when speaking in public settings? Are its claims careful and sourced, or built on rhetorical heat? Does its public communication cultivate charity toward opponents, or does it train Christians in contempt?

Due diligence that honors both truth and neighbor

Some donors assume apologetics ministries are inherently sound because they defend the faith. That is not always the case. The moral hazards are familiar: celebrity-centered governance, unaccountable platforms, financial opacity, and a temptation to treat controversy as a fundraising engine. A ministry can be doctrinally articulate and still fail basic standards of governance and transparency.

Our work at Most Trusted is designed to help donors give with confidence by evaluating ministries against The Most Trusted Standard, a 15-criteria framework that tests Faith Foundation, Financial Integrity, Governance and Leadership, and Transparency and Effectiveness. When you are considering where to direct RMD dollars inside the category of apologetics, it is wise to begin with organizations whose internal controls and public accountability can bear the weight of mature donor trust.

For donors surveying the field broadly, it is often helpful to start with the larger landscape of Christian Apologetics Ministries and then narrow to ministries whose practices are verifiably aligned with responsible stewardship.

Executing the gift without creating compliance problems

Coordination with custodians and ministry finance teams

The strongest giving intentions can be undermined by weak execution. QCDs and RMD-related gifts involve at least three parties: the donor, the custodian, and the receiving ministry. Each has a responsibility, and miscommunication is common. Custodians may require specific forms, medallion signatures, or mailing instructions. Ministries may have gift processing practices that are well-suited for online giving but less prepared for custodian-issued checks.

We recommend asking the ministry for clear instructions for IRA-originated gifts, including the payee name, mailing address, and any memo language they prefer to help them attribute the gift correctly. If the ministry cannot provide clear guidance, that is not a decisive disqualifier, but it is a warning sign that the organization may not be prepared to steward more complex gifts.

Recordkeeping and acknowledgments that withstand scrutiny

Donors sometimes assume that because a QCD is not taken as a charitable deduction, receipts do not matter. They do. Proper acknowledgment supports faithful bookkeeping and resolves disputes about whether a transfer was completed and credited. It also reduces confusion when multiple gifts are made in December and processed after year-end.

Beyond receipting, donors should keep custodian confirmations and any correspondence about the gift. These records protect both donor and ministry, particularly when an RMD is involved and timing is decisive. The IRS is explicit that the distribution must occur within the required year, and custodians can have holiday backlogs that cause delays. The best practice is not fear-driven; it is disciplined stewardship.

Aligning RMD giving with a long-term apologetics strategy

RMD giving works best when it is integrated, not episodic

RMD giving can become a stable funding stream for apologetics ministries, which often plan multi-year initiatives: publishing pipelines, curriculum development, campus partnerships, and media production. Stability matters because thoughtful apologetics is slow work. It requires scholarship, editorial rigor, and pastoral wisdom. If donors treat RMD giving as a once-a-year scramble, ministries receive volatility rather than strength.

A more mature approach is to set a giving policy for your household: decide what proportion of annual giving will go to your local church, to mercy ministries, to global missions, and to the intellectual and cultural work that apologetics supports. The proportions will vary by conviction and calling, but clarity reduces reactive giving and helps households avoid being led by the news cycle.

Testing a ministry’s posture toward truth, money, and power

Apologetics ministries should be held to a high standard precisely because they claim to speak for truth. Across our verification work, we find that strong ministries usually share a set of quiet traits: boards that are not composed of friends and employees, financial statements that can be understood by non-specialists, candid descriptions of outcomes and limitations, and a tone that reflects the gentleness Scripture commends even when argument is necessary (1 Peter 3:15).

For donors who want to go deeper on the giving methods that commonly support ministries in this space, Planned Giving for Christian Apologetics Ministries is a practical place to consider how RMDs relate to beneficiary designations, appreciated assets, and multi-year commitments.

FAQs for How to give required minimum distributions to apologetics ministries

Can we give our RMD to an apologetics ministry without increasing our taxable income?

Often, yes—if you are eligible to make a qualified charitable distribution and the receiving apologetics ministry is a qualified public charity. A QCD is made directly from the IRA custodian to the ministry and can satisfy the RMD while keeping the distribution out of taxable income, subject to IRS rules and limitations. The IRS QCD guidance is the primary reference point for eligibility and restrictions: IRS Qualified Charitable Distributions.

What should we verify about an apologetics ministry before directing an IRA distribution?

At minimum, confirm that the organization is legally eligible to receive the type of gift you are making and that it practices basic financial and governance accountability. For more substantive discernment, we recommend evaluating whether the ministry’s doctrine, leadership oversight, financial integrity, and public posture are consistent with mature Christian witness. At Most Trusted, we assess these questions through The Most Trusted Standard so donors can direct high-stakes gifts, including retirement assets, with greater confidence.

A disciplined way to turn an obligation into witness

An RMD is required, but its destination is not. When retirement distributions are directed with discernment, they can become a durable part of Christian generosity—supporting apologetics ministries that strengthen the church’s confidence, clarify the gospel in public life, and do so with accountable stewardship. The work is to unite technical competence with moral seriousness: the IRS rules matter, and so does the kind of ministry those dollars will shape.