Why Christian donors use charitable gift annuities is ultimately a question about how believers hold together two callings that Scripture refuses to separate: prudent stewardship and generous love of neighbor. A charitable gift annuity (CGA) can serve that integration by turning an irrevocable gift into a predictable stream of income for the donor, followed by a remainder gift to ministry.

The instrument is not new, and it is not simplistic. CGAs sit at the intersection of Christian ethics, retirement reality, and nonprofit trustworthiness. They can be a wise act of stewardship for some donors, and a poor fit for others. Mature Christian giving names those trade-offs plainly rather than baptizing every planned-giving tool as automatically “faithful.”

Charitable gift annuities join provision and generosity in a single commitment

Stewardship is not only about giving more

Christian stewardship includes generosity, but it also includes legitimate responsibility. Paul’s warning that a person who does not provide for family has “denied the faith” (1 Timothy 5:8) has often been misused, yet it still establishes that prudence is not a secular concession. Many Christian donors carry a real tension: they want to give meaningfully now, but they also fear becoming financially dependent later and shrinking their long-term generosity.

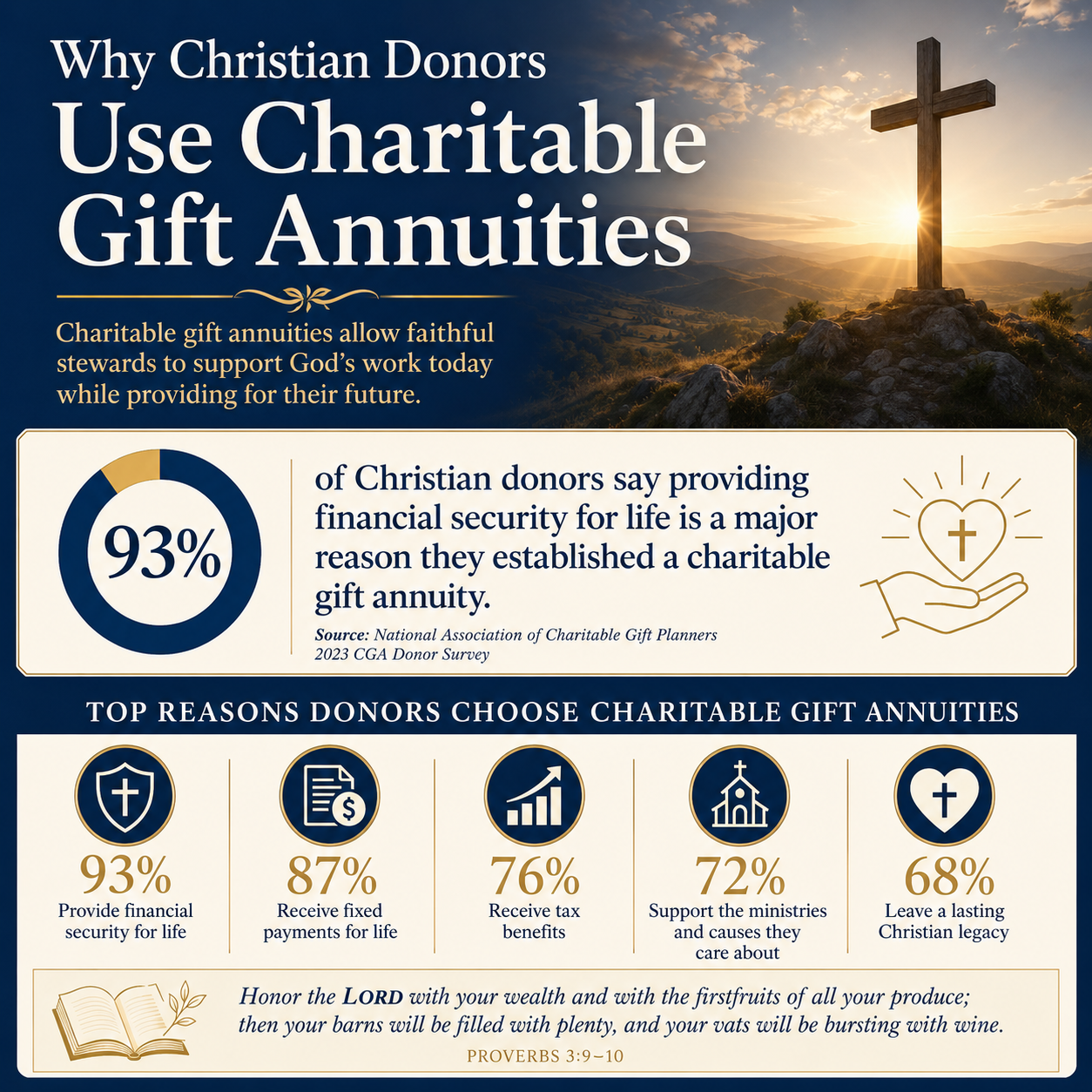

A charitable gift annuity can address that tension by exchanging assets for two outcomes: an immediate charitable gift and a contractual promise of fixed payments for life (or for two lives). The simplicity is part of the appeal. Unlike market-based investments, the payment amount is fixed in the contract. Unlike a typical donation, the donor receives ongoing income.

Clarity can be a spiritual relief for some households

Retirement planning creates uneven burdens. Some Christian households are asset-rich but cash-flow constrained, especially those who hold appreciated securities or property but live on a disciplined monthly budget. In those cases, converting a portion of assets into steady payments can create the margin to give with joy rather than anxiety.

The harder question is not whether stability matters. It is whether the stability is priced appropriately and whether the ministry promising payments is financially able to keep that promise for decades. That is where serious due diligence belongs.

Many donors value charitable gift annuities because they can be tax-efficient

Tax considerations are not the same as tax motives

Christians genuinely disagree about how directly believers should engage tax strategy in giving. Some worry that focusing on deductions undermines sacrificial generosity. Others argue that stewardship includes not paying more tax than required, freeing more resources for Kingdom purposes. Scripture does not command maximal tax liability; it commands honesty, generosity, and wise management.

A CGA often creates tax advantages because a portion of the gift may be treated as a charitable contribution, and part of the annuity payments may be taxed differently than ordinary income depending on the funding asset and the donor’s situation. The Internal Revenue Service describes the general treatment of charitable contributions and related substantiation requirements in its guidance for individuals and nonprofits at IRS.gov.

Appreciated assets make the question more concrete

Many planned gifts are funded not with checking-account cash but with appreciated securities. Donors may be trying to avoid selling assets, incurring capital gains, and reducing the amount available for ministry and for retirement income. CGAs can sometimes spread recognition of gain over time, though the precise outcome depends on the asset type and the donor’s basis.

What this means in practice is that donors should treat a CGA as a coordinated decision involving their tax advisor, their estate plan, and the ministry’s financial posture—not as a form pulled from a brochure.

Christian donors use charitable gift annuities to express long-term commitments to specific ministries

A CGA can be a disciplined way to “store up” toward future giving

Some giving decisions are episodic, driven by immediate needs. Others are covenantal, grounded in a sustained conviction about a ministry’s calling. A charitable gift annuity tends to reflect the second posture. Because the gift is irrevocable, it signals that the donor is not merely responding to this year’s appeal but entrusting a portion of their estate to a mission they believe will remain faithful.

This impulse is often strongest among donors who have watched ministries drift theologically or operationally over time. The desire is not simply to fund activity, but to support a work that will remain anchored in historic Christian faith while demonstrating competence and integrity. That is part of the reason donors seek verification and third-party assessment, not only compelling storytelling.

Verification matters because annuities create obligations

Across our verification work at Most Trusted, we observe that donors often evaluate charities as if every gift were a one-way transfer with no ongoing obligation. A charitable gift annuity changes the moral and financial texture of the relationship. The ministry is now a payer. The donor is now a contract holder. This does not make the relationship mercenary; it makes it more accountable.

The ministries that meet The Most Trusted Standard tend to treat accountability as a spiritual discipline: clear governance, appropriate reserves, transparent reporting, and leadership practices that protect mission over personality. Those qualities are not decorative. They are the kind of institutional strength a donor should want behind a decades-long payment promise. For donors evaluating this broader landscape, our coverage of Christian Stewardship Services addresses common decision points where financial planning and Christian conviction intersect.

Charitable gift annuities can reduce complexity compared to other planned gifts

Not every donor needs another moving part

Planned giving has expanded in sophistication. For some donors, donor-advised funds, trusts, complex beneficiary designations, and multi-asset strategies are appropriate. For others, additional complexity increases the risk of error, family misunderstanding, or unintended consequences.

A charitable gift annuity is often appealing because it is comparatively straightforward: a single agreement, a fixed payout, and a clear charitable remainder. The donor’s calculus can remain focused on stewardship and ministry confidence rather than on managing an intricate structure.

But simplicity does not eliminate due diligence

Even a simple contract can be unwise if the counterparty is weak. Donors should ask direct questions about how the annuity obligation is funded, what reserves the organization maintains, whether the organization participates in state annuity regulation where applicable, and how the nonprofit reports its financial position.

The following questions are generally reasonable for a donor to ask before signing a CGA agreement:

- How are annuity reserves held, and what investment policy governs them?

- What portion of total liabilities is represented by annuity obligations?

- Does the organization provide audited financial statements, and are they current?

- What is the organization’s history of meeting annuity payments through market cycles?

- Who on the board has explicit oversight of planned giving obligations?

These are not adversarial questions. They are questions of stewardship. Proverbs commends the wisdom of understanding one’s affairs clearly (Proverbs 27:23–24), and the same principle applies when Christian generosity takes contractual form.

Christian donors weigh charitable gift annuities differently in a higher-interest and higher-longevity environment

Payout rates and the cost of permanence

Charitable gift annuity payout rates in the United States are commonly influenced by the suggested rates published by the American Council on Gift Annuities. Those suggested rates are designed to balance donor value and charitable remainder expectations over time, and they have been revised in response to changing economic conditions. The Council publishes its guidance and history at acga-web.org.

Higher interest rates in the broader economy can make fixed-income alternatives more attractive, which may reduce the relative appeal of a CGA for some donors. At the same time, a CGA’s charitable component and relational commitment to a ministry may be precisely what differentiates it from a purely financial product. Christian donors are rarely making an “investment” decision in the narrow sense; they are choosing how to hold assets under the Lordship of Christ.

Longevity reshapes the donor’s responsibilities

Americans are living longer, and longevity risk is one reason donors may want dependable lifetime income. The U.S. Social Security Administration notes that life expectancy has increased dramatically over the last century, though with important differences by cohort and demographic factors; its public-facing resources summarize these trends at ssa.gov.

Longer lives can mean longer generosity, but they can also mean greater late-life costs and greater vulnerability to financial manipulation. Christian donors should account for those realities when deciding what to make irrevocable. A CGA that is too large relative to the household balance sheet can create pressure later and become a burden rather than a blessing.

For donors seeking ministries capable of bearing these obligations with integrity, our coverage in Christian Stewardship Services and Planned Giving addresses the governance and transparency signals that deserve attention when planned gifts create long-term commitments on both sides.

FAQs for Why Christian donors use charitable gift annuities

Are charitable gift annuities appropriate for every Christian donor?

No. A charitable gift annuity is most appropriate when a donor can make an irrevocable gift without compromising household obligations, and when the donor has high confidence in the ministry’s long-term stability and integrity. Some donors will be better served by simpler outright giving, beneficiary designations, or other structures. Wisdom is situational, and Scripture’s call is faithfulness rather than uniformity.

How should we evaluate a ministry before funding a charitable gift annuity?

Donors should evaluate a ministry’s theological clarity, governance, audited financials, and transparency about outcomes and risks. Because a CGA creates a contractual payment obligation, donors should also ask how reserves are held and overseen and whether the organization has a track record of honoring annuity commitments through economic downturns. Independent verification can strengthen this evaluation by applying consistent criteria and documenting evidence rather than relying on reputation alone.

A charitable gift annuity is a stewardship decision before it is a financial technique

Why Christian donors use charitable gift annuities is not reducible to tax benefits or payout rates. Many donors are searching for a faithful way to give substantially without pretending that aging, family responsibility, and economic volatility are unreal. A CGA can be a morally serious instrument when it is proportionate, well-advised, and placed with a ministry that merits long-term trust.

Christian generosity is not helped by naïveté, and Christian prudence is not helped by fear. When donors hold both together—seeking counsel, verifying institutional integrity, and giving as an act of worship—planned gifts can become one more way the church learns to handle money as disciples rather than as consumers.