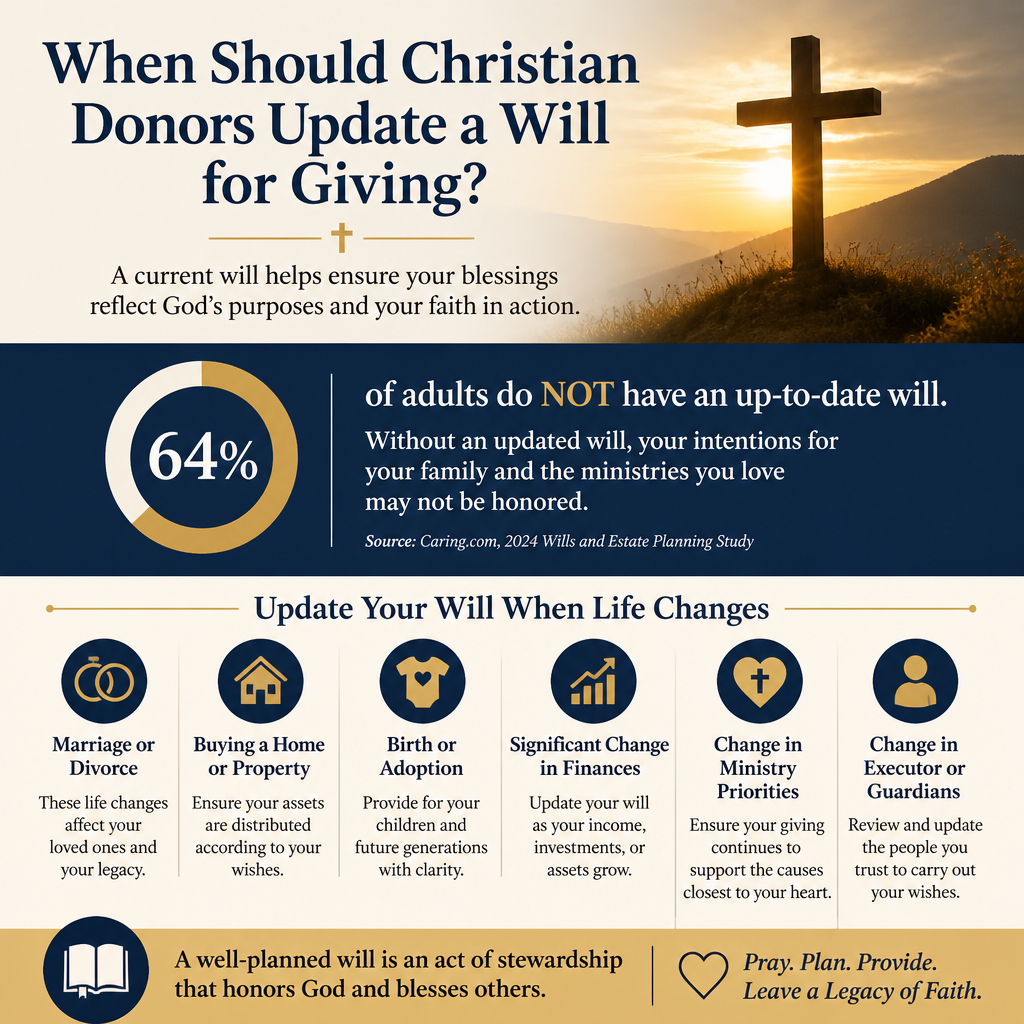

When should Christian donors update a will for giving? The best answer is not “when life calms down,” but when a Christian’s responsibilities, relationships, or charitable convictions have materially changed. A will is not merely a legal document; it is one of the last places where stewardship is made concrete for heirs, for churches, and for ministries that will carry on work long after a donor is gone.

Scripture’s teaching on stewardship is not sentimental. Jesus repeatedly connects money with allegiance, trust, and the Kingdom of God (Matthew 6:19–24). A mature planned giving practice treats a will as part of discipleship, not an administrative footnote. What this means in practice is periodic, disciplined review—especially at moments when the story of a household changes.

Major life changes are the most common and most urgent triggers

Across many countries and legal systems, estate plans do not fail because donors lacked good intentions. They fail because the donor’s plan was built for an earlier season of life. Christian donors are often balancing family obligations, church commitments, and a growing sense of responsibility toward high-impact ministry. When those factors shift, the will should shift as well.

Family structure changes

Marriage, divorce, remarriage, and the birth or adoption of children are not only emotional transitions; they are fiduciary transitions. Guardianship provisions, contingent beneficiaries, and the distribution logic of the estate may need a full reset. When blended families are involved, clarity becomes an act of love. Ambiguity may feel charitable, but it often produces conflict.

Even in stable families, adult children’s circumstances can change. A child who develops a disability, struggles with addiction, or faces chronic financial instability may require thoughtful provisions or a trust structure rather than a simple equal split. Christian charity does not require naïveté about human frailty.

Loss, illness, and capacity concerns

The onset of serious illness, cognitive decline, or a significant caregiving burden should prompt an early review, not a delayed one. The window in which a donor can update documents with full clarity and uncontested capacity can be shorter than families expect. For donors who want their giving intentions honored, timeliness is a form of stewardship.

In the United States, the Internal Revenue Service provides general guidance on estate and gift considerations that often shapes charitable planning decisions, including bequests and beneficiary designations. See the IRS overview at Internal Revenue Service.

Financial and asset changes often require more than a simple edit

Most donors think of a will as a distribution list. In reality, a will is also an instruction set for administering complexity. When the estate’s asset mix changes, the will’s charitable provisions can become unintentionally distorted.

A new home, business, or concentrated stock position

Real estate purchases, the sale of a business, or the accumulation of a concentrated stock position can move a household from “straightforward” to “complex” overnight. A percentage-based charitable bequest may become too large or too small relative to family needs. A specific-dollar bequest can become outdated by inflation, especially over long time horizons.

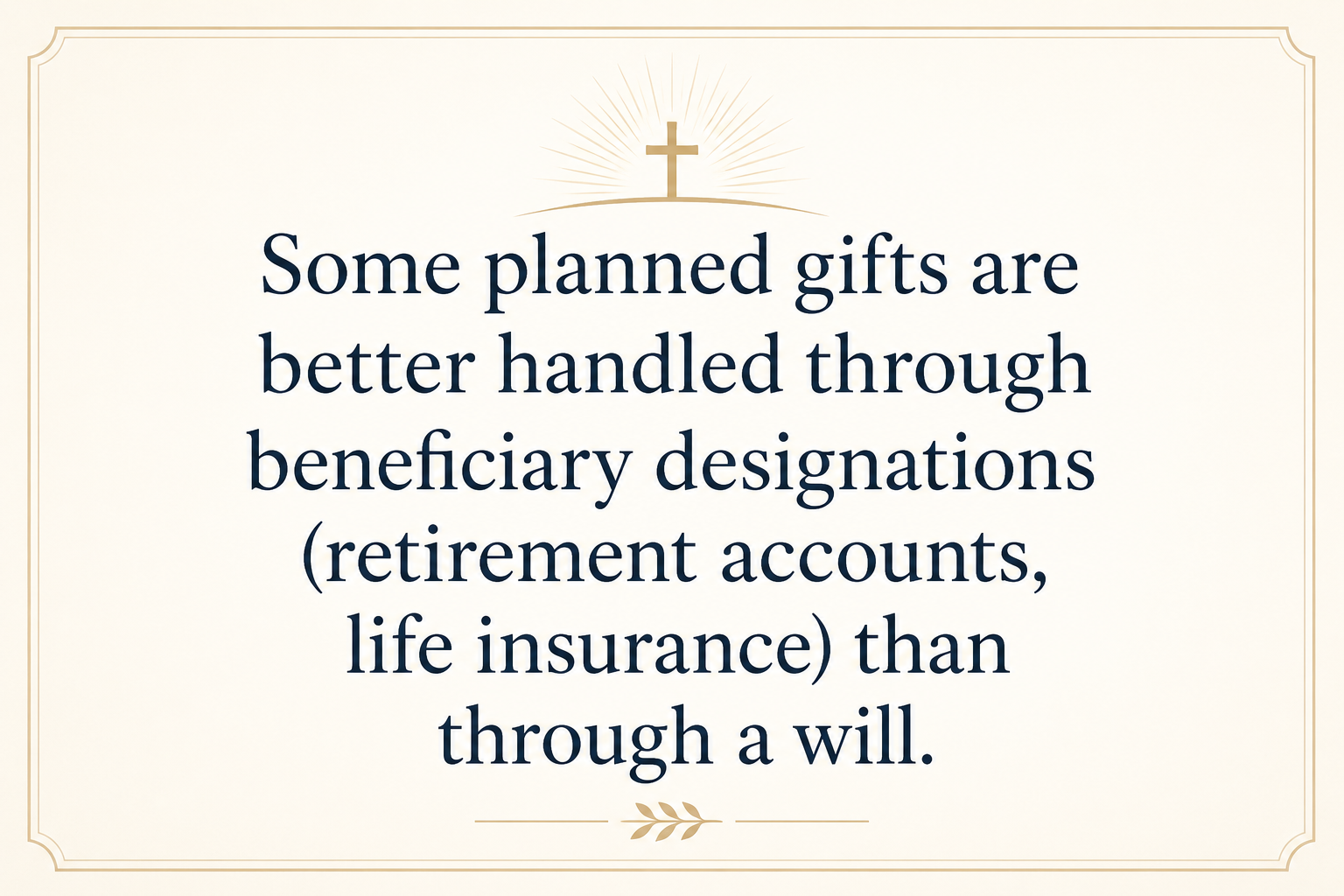

Some planned gifts are better handled through beneficiary designations (retirement accounts, life insurance) than through a will. Many donors are surprised to learn that beneficiary designations can bypass a will entirely. If charitable intent is expressed only in a will while the bulk of wealth sits in accounts transferred by designation, the will may not accomplish what the donor believes it will accomplish.

Debt, liquidity, and administrative burden

Christians sometimes assume that a charitable bequest will “sort itself out” after expenses. But estates require liquidity to settle taxes, debts, and administrative costs. If the estate is illiquid—heavy in property or private business interests—the executor may be forced into sales that harm both heirs and charitable goals. Updating a will can include adding specific instructions for how charitable distributions should be funded or sequenced.

Donors who want to understand the legal architecture of bequests and beneficiary designations in a U.S. context can consult the American Bar Association’s public information resources at American Bar Association.

Ministry convictions change, and wills should reflect mature discernment

Christian giving is not static across a lifetime. Many donors begin with a wide charitable spread and, over time, narrow toward ministries they believe are both faithful and effective. That narrowing is often the fruit of prayer, experience, and sober assessment of outcomes. When convictions have changed, an estate plan that remains unchanged becomes a mismatch between belief and practice.

When a donor’s giving priorities become more defined

A will can express long-term commitments that a donor wants to outlive them: local church support, global missions, theological education, crisis relief, foster care, prison ministry, pregnancy resource centers, Bible translation, or other works of mercy. Christians genuinely disagree about the relative priority of some causes. What mature donors can do is ensure their estate reflects their settled convictions, not yesterday’s defaults.

This is also where responsible verification matters. A bequest is often the largest single gift a donor will make to a ministry. It deserves more than a warm brand impression. Most Trusted exists to help donors give with confidence by evaluating ministries against The Most Trusted Standard, a 15-criteria framework that tests faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. The question is not merely whether a ministry inspires, but whether it can be trusted to steward what it receives.

When a named ministry’s reality changes

Ministries merge, rebrand, close, or drift from their founding commitments. Some experience governance failure. Others remain faithful but change program emphasis. A will that names a ministry without any contingency can create confusion or litigation if the organization no longer exists or no longer matches the donor’s intent.

What this means in practice is writing charitable clauses that are clear about purpose and flexible about the vehicle. Donors may, for example, direct funds to a ministry “for pastoral training in underserved contexts,” with a backup charitable beneficiary if the primary cannot fulfill the purpose. Skilled counsel is essential here; donors should not draft these provisions casually.

Good governance includes reviewing the executor and decision-makers

Estate planning is often treated as a distribution problem when it is also a governance problem. A will is executed by people under pressure, often in grief. If the wrong people are empowered, even a sound plan can become contentious or ineffective.

Executors, trustees, and successor roles

When an executor relocates, becomes elderly, experiences health decline, or demonstrates unreliability, an update is warranted. The same is true if the donor’s chosen executor has a conflict of interest with charitable distributions. It is neither unspiritual nor unkind to choose a more competent fiduciary. Prudence is a biblical virtue.

A practical review cadence and a short checklist

Many estate attorneys recommend reviewing an estate plan periodically and after major life events. Donors can hold that rhythm without becoming anxious or obsessive. A simple discipline is often sufficient:

- Review the will after any marriage, divorce, remarriage, birth, or adoption.

- Reassess after a major asset change such as a home purchase, business sale, or inheritance.

- Confirm beneficiary designations align with charitable intent and do not unintentionally override the will.

- Verify named ministries still exist and still match the donor’s theological and program convictions.

- Confirm the executor and any trustees remain capable, willing, and appropriately independent.

Donors who want a broader view of how stewardship practices intersect with planned giving decisions can engage the wider context in Christian Stewardship Services and Planned Giving without treating estate planning as an isolated task.

Tax and legal changes can reshape what is wise and what is possible

Christian donors should resist making estate plans purely tax-driven. At the same time, tax policy affects what heirs receive and how charitable gifts are administered. Ignoring legal changes is not spiritual; it is imprudent.

When laws change, revisit the mechanics

Federal and state estate tax thresholds, required minimum distribution rules for retirement accounts, and nonprofit compliance standards can change. Charitable strategies that were straightforward a decade ago can become less efficient or require different documentation. A periodic legal review helps ensure that the intended charitable outcomes remain intact.

When the question is trust, not only tax

Even when a charitable bequest is tax-advantaged, the deeper question is whether the recipient will steward the gift faithfully. Donors often feel this tension acutely: they want to fund gospel work, yet they have watched public ministry scandals erode confidence. This is a place where verification work is directly relevant. In our evaluations at Most Trusted, we see patterns: ministries that meet The Most Trusted Standard tend to document board oversight more clearly, communicate financials more transparently, and show stronger alignment between stated mission and measurable activity. That does not eliminate risk, but it improves a donor’s odds of honoring both generosity and prudence.

For donors seeking a broader stewardship framework that integrates convictions, discernment, and accountability, Christian Stewardship Services provides a context for thinking about giving as a long-term practice rather than a series of isolated transactions.

FAQs for When should Christian donors update a will for giving

Should a charitable bequest be a specific dollar amount or a percentage?

Both can be appropriate, and the better choice depends on the donor’s asset mix and the priority of the gift. A percentage often adjusts more naturally over time as the estate grows or shrinks, while a specific amount can protect heirs from unintended dilution when the estate increases dramatically. Donors who want both clarity and flexibility sometimes use a percentage with a cap or include secondary beneficiaries with clear sequencing, drafted with counsel.

Should donors name a ministry directly, or route the gift through a donor-advised fund or foundation?

Naming a ministry directly can be simple and aligned when the ministry is stable, well-governed, and the donor’s intent is narrow. Routing through a donor-advised fund or foundation can add flexibility if the donor anticipates ministry changes over time or wants successors to direct grants. The trade-off is that additional entities add additional governance questions. Whatever structure is chosen, the same stewardship principle applies: verify the integrity and accountability of the organizations that will control the funds.

Updating a will is one of the clearest forms of downstream stewardship

Christian donors update a will for giving when the realities that shape stewardship have changed: family responsibilities, assets, convictions, decision-makers, or the ministries themselves. A will is one of the last opportunities to practice ordered love—providing for household obligations while honoring the work of Christ’s kingdom beyond one’s lifetime. The discipline is not driven by fear, but by a desire for faithfulness that is durable under pressure.