What tax receipts Christian camps should provide is not a minor administrative question. For donors, a receipt is where spiritual intent meets legal clarity: a ministry acknowledges a gift, the donor substantiates a deduction, and both parties preserve integrity before God and neighbor.

Christian camps often carry a unique mix of giving: scholarship funds, capital projects, missionary staff support, in-kind donations, and a steady stream of parent payments for summer programs. That mixture creates predictable points of confusion. When receipts are vague or inconsistent, donors bear the risk, and the camp’s credibility erodes. What sober stewardship requires is straightforward documentation, issued promptly, consistent with IRS requirements, and aligned with the camp’s actual practices.

Receipts are not merely paperwork for serious Christian stewardship

Giving is worship and the record should be truthful

Scripture’s insistence on honest weights and measures applies to modern charitable giving as surely as it did to marketplace trade. Receipting is not a spiritual ornament; it is part of telling the truth about what was given, what was received, and what—if anything—was provided in return. When ministries treat receipts casually, they inadvertently teach donors that financial truthfulness is negotiable.

Christian donors also need documentation for civil obligations. The IRS requires donors to keep a bank record or written communication from the charity for any cash contribution, regardless of amount, and it requires a contemporaneous written acknowledgment from the charity for contributions of $250 or more. These rules are not optional guidelines; they are binding conditions for deductibility. See IRS Publication 526, “Charitable Contributions,” for the baseline substantiation framework: IRS.

The camp’s credibility is built in small, verifiable acts

Across our verification work at Most Trusted, we observe that ministries that meet The Most Trusted Standard tend to treat donor receipting as part of transparency, not as a necessary nuisance. The camp that can produce clear acknowledgments, consistent valuation policies, and defensible donor communications is usually the camp that can answer harder questions as well—about governance, restricted funds, and outcomes.

Donors who want a broader view of how camps are structured and evaluated across the sector often begin with Christian Camps and Conferences. The same disciplined habits that build a trustworthy receipts process tend to appear in the camp’s financial reporting and board oversight.

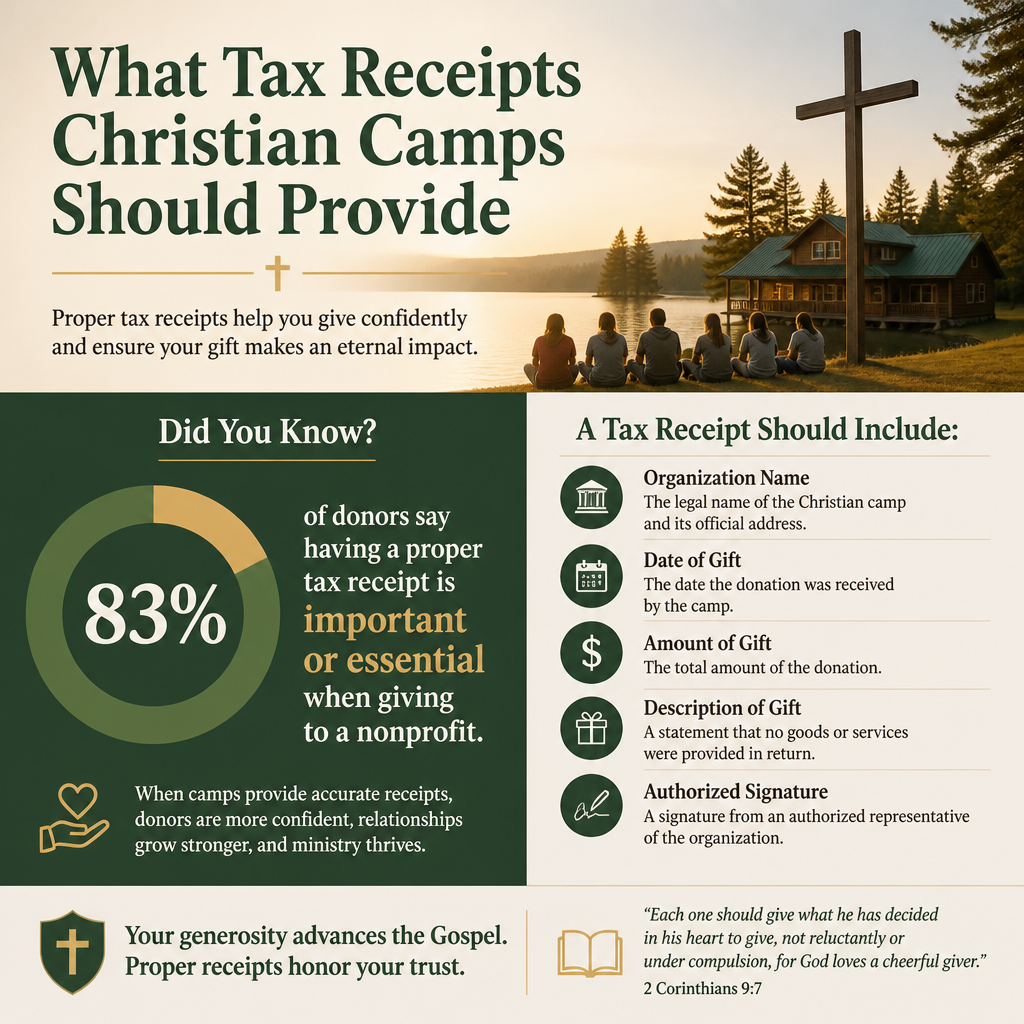

What a compliant Christian camp receipt must include for cash gifts

The required elements for gifts of 250 dollars or more

For any single contribution of $250 or more, the donor must receive a contemporaneous written acknowledgment from the charity. “Contemporaneous” means the donor receives it by the earlier of the date the donor files the return or the due date of the return, including extensions. The acknowledgment must state (1) the amount of cash and a description of any property contributed, (2) whether the organization provided any goods or services in exchange, and (3) if goods or services were provided, a good-faith estimate of their value (or a statement that only intangible religious benefits were provided). These requirements are laid out in IRS Publication 1771: IRS.

Cash gifts include checks, credit card gifts, ACH transfers, online payments, and payroll deductions. A camp that issues annual consolidated receipts should still be careful: a consolidated receipt must clearly itemize dates and amounts and include the required quid pro quo statement.

A short checklist camps should consistently follow

A well-formed receipt for a cash gift generally includes the following components, in plain language:

- The camp’s legal name and EIN

- The date the contribution was received and the amount

- A statement that no goods or services were provided in exchange, if that is true

- If goods or services were provided, a good-faith estimate of their value

- If applicable, a statement that only intangible religious benefits were provided

Christian camps sometimes omit the goods-or-services language because it feels awkward. Yet that sentence is often the difference between a receipt that merely thanks and a receipt that protects. The donor should not have to infer whether a benefit existed.

Quid pro quo is where camps most often confuse donors

Program fees and event payments are usually not charitable gifts

Parents paying for camp are typically purchasing services. If a family pays $800 for a week of camp for a child, that payment is generally not a charitable contribution simply because the organization is a ministry. The payment may become partly deductible only when the family pays more than the fair market value of what they received and intends the excess as a gift. The camp then has the responsibility to communicate clearly about the value provided and the portion that may be deductible.

IRS guidance on quid pro quo contributions and the need for written disclosure for certain contributions is addressed in Publication 1771. It includes the core principle: if a donor receives goods or services in return for a payment, only the amount exceeding the fair market value of the benefit may be deductible. See: IRS.

Common camp situations that require careful receipting

What this means in practice is that camps should be explicit in scenarios such as these:

Banquets and fundraising dinners. If a table sponsor receives a meal, the receipt should disclose the fair market value of the meal per attendee and separate the deductible portion.

Golf tournaments or benefit events. Green fees, meals, and swag packages are benefits; the camp should estimate value in good faith and communicate it plainly.

Premiums and thank-you gifts. If a camp sends a book, hoodie, or other item tied to a donation, it must evaluate whether it constitutes a benefit requiring valuation and disclosure. Some small items may fall under IRS “token” exceptions, but camps should not assume. When uncertain, conservative disclosure is safer than creative silence.

Camperships and sponsorships. Donors often want to “sponsor a camper.” The key question is whether the donor is paying for a specific individual’s benefit in a way that becomes a personal gift rather than a charitable contribution. Camps should design scholarship funds so that the camp retains full discretion and control over distribution, then describe that reality clearly in donor communications.

Noncash gifts, stock, and in-kind donations require different language

The camp should describe property but not assign a value

When donors give noncash property—equipment, vehicles, supplies, or other goods—the camp’s receipt should describe what was received but should generally not state a dollar value. Valuation is ordinarily the donor’s responsibility. A vague “thank you for your generous donation” is not sufficient. A defensible receipt describes the item in a way that an outside reviewer can recognize, such as “one used riding lawn mower” or “twelve cases of canned food,” and includes the date of receipt and the goods-or-services statement.

IRS Publication 526 addresses noncash contributions, including the donor’s responsibility for determining fair market value and the substantiation rules. See: IRS.

Special cases donors ask about often

Gifts of stock. Many mature Christian donors give appreciated securities for tax efficiency. The camp’s receipt should identify the name of the security and the number of shares (or units) transferred, along with the date received, but should not state value. Donors typically use the fair market value on the date of transfer for their deduction, subject to applicable rules.

Vehicles. Vehicle donations can trigger additional forms and reporting depending on what the charity does with the vehicle. Camps should ensure they understand the IRS requirements for acknowledgments when a vehicle is sold or used, and donors should be encouraged to consult qualified tax counsel for larger gifts.

In-kind services. Donors cannot deduct the value of volunteered services, even if highly skilled, though they may deduct certain unreimbursed expenses if substantiated. Camps should avoid issuing receipts that imply a deduction for the value of labor. IRS Publication 526 covers this distinction: IRS.

Receipting practices signal whether a camp is prepared for major gifts and planned giving

Restricted gifts require precision, not goodwill

Major donors frequently designate gifts: “for the dining hall renovation,” “for camperships,” “for the endowment.” The receipting itself does not create a restriction; the donor’s intent and the charity’s acceptance do. Still, the receipt and follow-up communication should accurately reflect what was agreed. When camps casually acknowledge a designation they cannot or will not honor, they place future reporting and donor trust at risk.

Across our evaluation work, weak receipting often correlates with weak restricted-fund discipline. The camp may mean well, but good intentions do not reconcile accounts. Donors funding ministry for the long term should expect the same clarity a prudent board expects in its financial statements.

Planned gifts need documentation and coordination

Planned giving introduces additional documentation layers: bequests, beneficiary designations, charitable gift annuities, and complex gifts of property. Receipts may be only one part of the paper trail, but they still matter, particularly when gifts are received through an estate or when a donor makes a partial-interest gift.

Donors considering these instruments often benefit from reviewing how camps handle larger and longer-horizon gifts within Planned Giving and Major Gifts for Christian Camps. Healthy camps coordinate between development, finance, and legal counsel so that donor intent, accounting treatment, and donor communications agree with one another.

A necessary tension should be named plainly: donors sometimes want a receipt that is “helpful” rather than accurate—one that implies deductibility where the law does not support it. A camp faithful to Christian ethics will resist that pressure. Truthfulness is part of witness.

FAQs for What tax receipts Christian camps should provide

Should a Christian camp issue a receipt for camp tuition or registration fees?

If the payment is a fee for services received, it is generally not a charitable contribution and should not be receipted as a donation. If a payer gives more than the fair market value of what they receive, the camp should provide a written acknowledgment that discloses the value of goods or services provided so the payer can determine any deductible portion under IRS quid pro quo rules.

Can a camp receipt say a donor received no goods or services if the donor attended a banquet?

No. If the donor received a meal or other benefits, the acknowledgment should disclose that goods or services were provided and include a good-faith estimate of their value. The deductible portion is generally the amount paid minus the fair market value of the benefits received, consistent with IRS requirements.

The aim is integrity that donors can verify

Christian donors give because they believe the gospel bears fruit through ordinary institutions: boards, budgets, staff, and programs. A camp’s tax receipts are one of the most repeatable tests of whether that institution treats truth carefully.

When camps issue clear acknowledgments, disclose benefits without evasion, and handle noncash gifts with appropriate restraint, donors are not merely protected from audit problems. They are invited into a relationship marked by transparency. That is the kind of credibility that can sustain scholarships, facilities, and faithful ministry for decades.