Fees are the hidden theology of Christian donor-advised funds: they reveal what a sponsor believes it costs to steward other people’s giving. When Christian donor-advised funds charge fees, the question is not merely whether fees exist, but whether they are proportionate, transparent, and aligned with the donor’s calling to give wisely.

Most donors accept that administration, compliance, and reporting have real costs. The harder question is whether a particular fee structure serves faithful stewardship or quietly erodes it—especially when layered with investment expenses, payment processing costs, and operational rules that can change how and when grants reach ministries.

How Christian donor-advised funds typically structure fees

A donor-advised fund sponsor can charge in several ways, and the choices are rarely neutral. Some structures reward scale and long-term balances; others are designed to keep the sponsor financially whole on small accounts. Christian donors often care about this because fee design can incentivize behavior that competes with generosity: keeping assets under management rather than moving gifts to ministry.

Administrative fees

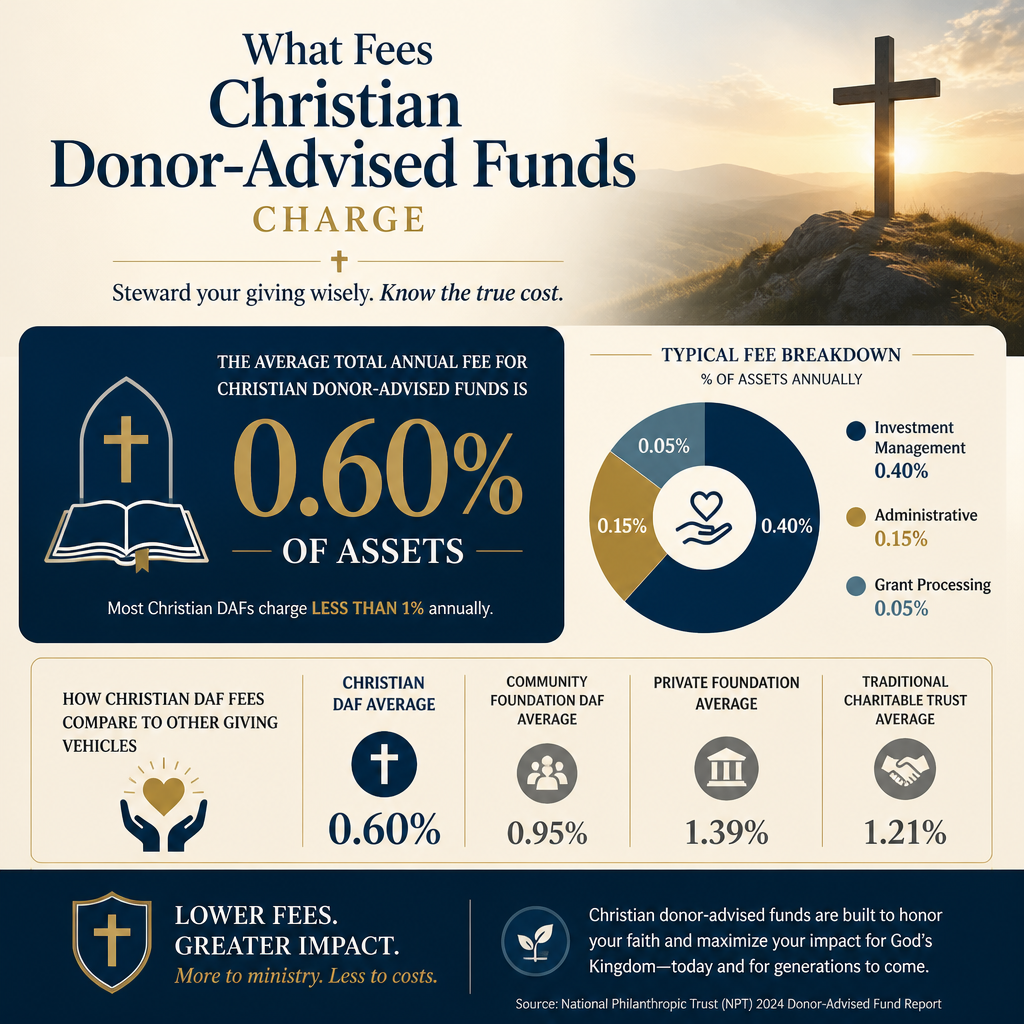

Many sponsors charge an annual administrative fee, commonly expressed as a percentage of assets in the account, sometimes with a minimum dollar amount. This fee is often described as covering recordkeeping, tax receipting, compliance, grant processing, and donor support. In practice, donors should read what is included and what triggers additional charges, because “administration” can be a narrow category.

Investment-related costs

Even if the sponsor’s administrative fee seems modest, underlying investment expenses can materially affect net performance. These costs may include the expense ratios of mutual funds or ETFs and, in some cases, additional management fees if proprietary or actively managed strategies are used. The sponsor may disclose these in a separate schedule from the administrative fee, which is why donors should evaluate total cost, not marketing headlines.

Grant and transaction fees

Some sponsors charge per-grant fees, check fees, wire fees, or fees for complex grants (for example, international grants that require expenditure responsibility processes). Others charge credit card or ACH processing fees when donors contribute via card or bank transfer. These fees can matter for donors who prefer frequent, smaller grants or who support many local ministries.

A practical checklist for reading a fee schedule

- Identify the sponsor’s administrative fee and any minimum annual charge.

- Add underlying fund expense ratios or advisory fees to estimate total annual drag.

- Ask whether grantmaking has per-transaction costs or thresholds.

- Confirm whether the sponsor retains any portion of investment returns or cash yields.

- Locate policies on inactive accounts, termination, or required minimum balances.

Why fee design matters for Christian stewardship

Christian giving is not simply philanthropy; it is worshipful stewardship of resources entrusted by God. Scripture’s warnings about wealth do not only address hoarding; they address the subtle ways money acquires spiritual weight. Fee structure matters because it is one of the mechanisms that can either support disciplined generosity or normalize delay, complexity, and opacity.

Fees and the temptation to treat a DAF as a permanent warehouse

Donor-advised funds can help donors give more thoughtfully, especially after a liquidity event or a year of unusual income. They can also become permanent warehouses. The broader field has debated payout and warehousing for years, and serious donors should acknowledge that the incentives can be misaligned when sponsors’ revenue depends on assets staying put.

For context on scale: donor-advised funds in the United States held roughly $251.5 billion in assets in 2023, according to the National Philanthropic Trust’s annual report (National Philanthropic Trust). This figure does not prove any single sponsor is unhealthy, but it clarifies why fee design and sponsor incentives deserve careful scrutiny.

Fees as a governance and transparency question

At Most Trusted, our work centers on verifying ministries against The Most Trusted Standard, with particular attention to financial integrity, governance, and transparency in communication. A DAF sponsor is not the same as a ministry receiving a grant, but the principle transfers: mature stewardship requires clarity about where costs sit, how they are justified, and who bears them.

Donors who already evaluate ministries for clarity and candor should apply a similar lens to the giving vehicle itself. When a sponsor cannot present a single, comprehensible view of total fees—administrative plus investment plus transactional—the problem is not complexity; it is disclosure.

Common fee models and the trade-offs they create

Fee schedules are moral documents in the sense that they create incentives. The question is not whether a sponsor must cover real costs; it is whether the model nudges donors toward faithful patterns of giving and whether the sponsor’s margin is earned in a way consistent with Christian witness.

Tiered percentage of assets

A tiered assets-under-management model charges a higher percentage on the first tranche of assets and lower percentages as balances rise. This can be fair if actual service costs are front-loaded, but donors should ask how the tiers were derived and whether the effective fee declines meaningfully as accounts grow. For high-balance accounts, even a “low” percentage can represent a significant annual cost in absolute dollars.

Flat annual fees

A flat annual fee can be more equitable for donors who grant frequently and do not want the sponsor’s revenue to grow simply because the market rose. The risk is that small accounts may be priced out, or donors may be encouraged to keep a higher balance to “justify” the flat fee. Donors should evaluate whether the sponsor provides appropriate service at the flat rate and whether the policy is stable over time.

Minimums, additional charges, and policy friction

Minimum account sizes, inactivity fees, and special handling charges are not necessarily wrong. They may reflect genuine operational costs. But donors should treat them as signals about the sponsor’s intended donor profile and their willingness to support ordinary, church-shaped patterns of giving—frequent grants, modest account sizes, and responsiveness to local needs.

Understanding how these choices function in the broader ecosystem is part of understanding How Christian Donor-Advised Funds Work, especially when donors want a DAF to serve both planned generosity and timely support for ministries.

Fees should be weighed alongside ministry verification

A sponsor’s fee schedule is only one side of stewardship. The other side is whether grants are reaching ministries that are faithful, well-governed, and transparent about results and setbacks. Christian donors are often disappointed not by the idea of overhead, but by preventable opacity: unclear financial statements, weak boards, or reporting that trades evidence for sentiment.

Do not confuse low fees with high trust

A low-fee sponsor can still facilitate giving to organizations that cannot withstand scrutiny. Likewise, a higher-fee sponsor may provide meaningful diligence tools, grant processing safeguards, or support that reduces donor risk. The point is not to pay more; it is to pay only for what actually strengthens stewardship.

In the broader nonprofit sector, leading evaluators have argued against simplistic overhead ratios as a proxy for effectiveness. The “overhead myth” consensus statement was signed by Charity Navigator, Candid (GuideStar), and the BBB Wise Giving Alliance (Charity Navigator). Christian donors should take that critique seriously while also refusing the opposite error: treating any level of fees as automatically justified.

Where Most Trusted fits in a donor’s process

Most Trusted exists to help donors give with confidence by evaluating ministries against The Most Trusted Standard. A DAF is a tool; it does not absolve donors of discernment about recipients. When donors pair a clear-eyed understanding of DAF costs with careful verification of the ministries they support, the result is not perfection, but a more mature posture: disciplined generosity with fewer avoidable surprises.

For donors building a long-term giving strategy, connecting the mechanics of a DAF with the theological aims of generosity is part of the larger conversation about Christian Donor-Advised Funds.

Questions to ask a Christian DAF sponsor before opening an account

Fee disclosures can be technically accurate and still leave donors in the dark. Mature sponsors should welcome direct questions, answer them without defensiveness, and provide written documentation that matches what was said. Donors should expect clarity because they are not purchasing a luxury service; they are entrusting a sponsor with a channel for charitable funds.

Questions that surface total cost and incentives

Start with the question, “What will we pay in a typical year?” and insist on an answer that includes administrative fees, underlying investment expenses, and transaction costs. Then move to incentives: “How does the sponsor make money, and what behaviors does that reward?” A sponsor that cannot speak plainly about these matters is not ready to carry the weight of Christian stewardship.

Questions that surface operational integrity

Ask how long grants typically take to process, what due diligence is performed on recipient organizations, and what policies govern grants to churches, international ministries, or individuals in crisis. Some sponsors are restrictive; others are permissive. Neither posture is automatically faithful. The faithful posture is the one that is transparent, legally compliant, and aligned with the donor’s intent without exposing the donor or the recipient to preventable risk.

FAQs for What fees Christian donor-advised funds charge

Are fees for Christian donor-advised funds tax-deductible?

Typically, fees charged inside a donor-advised fund are paid from charitable assets already contributed, not treated as a separate charitable gift. That means donors usually do not receive an additional charitable deduction for fees beyond the deduction associated with the original contribution. Because fee treatment can vary by sponsor structure and by how contributions are processed, donors should confirm the sponsor’s policy in writing and consult a qualified tax professional for their specific situation.

Is a higher-fee Christian DAF ever the wiser choice?

It can be, if the added cost corresponds to measurable value that strengthens stewardship: clearer reporting, better grant processing, stronger controls, more transparent investment options, or services that help donors give more faithfully and efficiently. A higher fee is not a virtue, but neither is the lowest possible price. The standard is whether the total cost is proportionate, understandable, and aligned with the donor’s purpose to support faithful ministry.

Choosing a fee structure that serves generosity

Christian donors rarely regret paying for legitimate accountability; they often regret paying for complexity that produces little clarity. The wisest approach is to treat DAF fees as part of a stewardship audit: understand total cost, identify incentives, and insist on transparency that respects the donor and honors the ministries funded. When the giving vehicle is clear and the recipients are verified with care, donors are better positioned to give with both conviction and prudence.