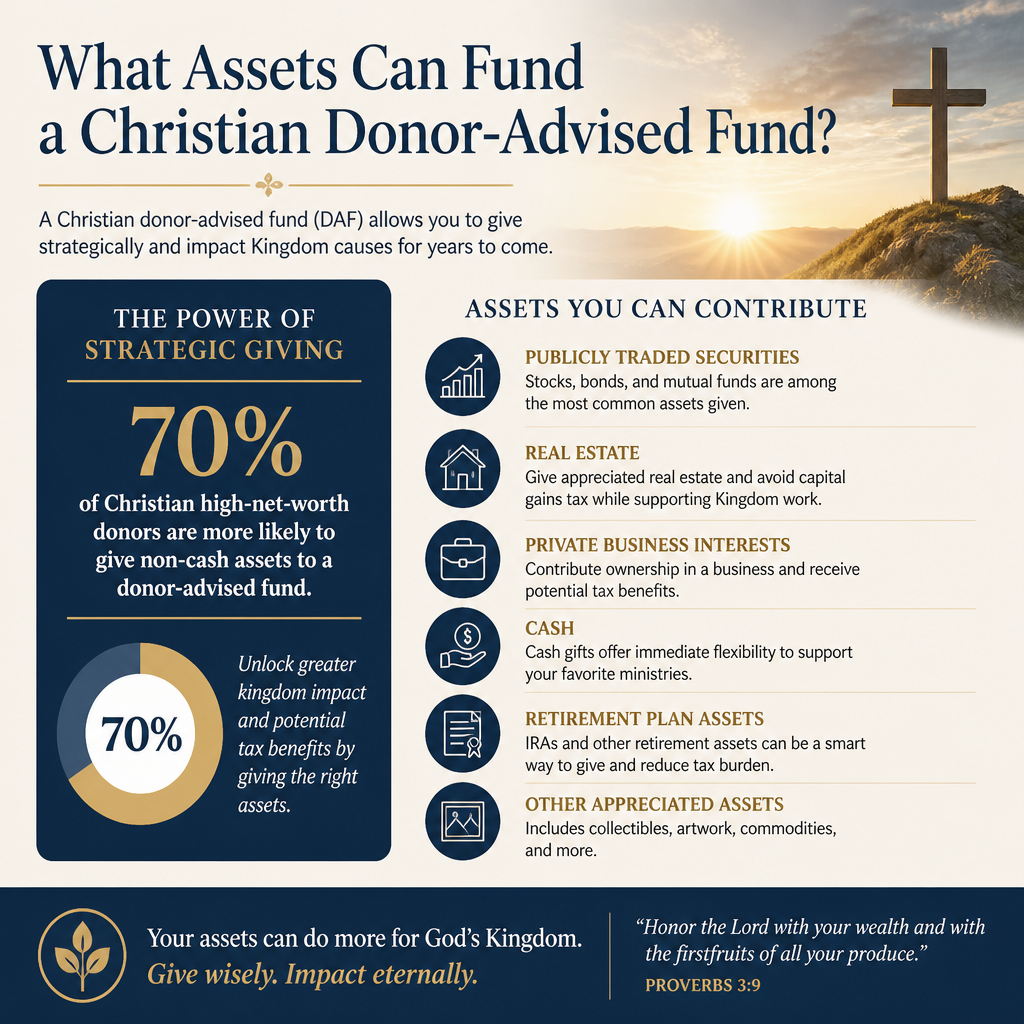

What assets can fund a Christian donor-advised fund is not a narrow technical question. It is a stewardship question with spiritual and practical consequences, because the asset you contribute determines the tax outcome, the administrative burden, and often the long-term capacity of your giving.

Many Christian donors arrive at donor-advised funds after a season of heightened attention to generosity: a liquidity event, an appreciated investment portfolio, a growing desire to simplify recurring gifts, or a renewed conviction that Christian giving should be planned rather than reactive. A donor-advised fund can serve that intent well. But it is only as disciplined as the inputs you choose and the ministries you support.

Start with the stewardship objective, not the asset list

Giving is worship, and worship deserves forethought

Scripture speaks with unusual clarity about money because money so often reveals what we love. Jesus’ warnings about treasure and the heart do not merely caution against greed; they call believers to intentional stewardship that resists drift. For donors considering which assets to contribute, the spiritual question sits beneath the financial one: will this act of giving increase freedom for cheerful generosity, or will it create new forms of complexity and self-protection?

A Christian donor-advised fund is typically most helpful when it supports a clear objective: accelerating giving in a high-income year, shifting from cash-only giving to more tax-wise giving of appreciated property, or building a disciplined grantmaking plan for a set of ministries over multiple years. Without that objective, donors can overcomplicate contributions, underfund near-term ministry, or allow a philanthropic account to become a substitute for actual giving.

Tax rules are real, but they are not the point

Donor-advised funds sit within the charitable framework of U.S. tax law. The Internal Revenue Service regulates donor-advised funds under rules that vary depending on the sponsoring organization and the type of asset contributed. Tax considerations matter because they shape capacity: giving appreciated assets can often avoid capital gains tax that would otherwise reduce what could be deployed to ministry. But mature Christian stewardship keeps tax wisdom in its place. We give because God is generous, not because the tax code is.

What this means in practice is that the “best” asset is the one that aligns with your convictions, your financial situation, and the actual needs and trustworthiness of the ministries you intend to support. For donors who want the broader context and common strategies, our editorial work on Christian Donor-Advised Funds addresses how donor-advised funds fit into long-term Christian giving.

Cash and cash equivalents remain the simplest and most overlooked option

Cash is frictionless, which is not the same as small

Cash contributions—via check, ACH, wire, or sometimes card—are the most straightforward way to fund a donor-advised fund. They typically settle quickly, are easy for the sponsor to receipt, and involve minimal valuation questions. That simplicity can be an advantage for donors who want to act promptly in response to conviction, crises, or time-sensitive ministry needs.

Some donors treat cash as a “less strategic” asset, but that assumption can be misguided. Cash can be the right answer when you are already giving appreciated assets elsewhere, when your investment holdings are not meaningfully appreciated, or when the giving timeline is short and the cost of processing non-cash assets would erode the value of the gift.

When cash is not wise

Cash is often not the most tax-efficient asset when a donor holds significantly appreciated securities. Selling an appreciated asset to generate cash can trigger capital gains tax, leaving less available for ministry than if the appreciated asset were contributed directly. The general tax principle is widely understood, but its practical application depends on the asset, the size of the gain, and the sponsor’s ability to accept the contribution.

Donors should also weigh liquidity prudently. Christian generosity does not require financial recklessness, and wisdom literature commends foresight. Funding a donor-advised fund with cash that will be needed for near-term obligations can create pressure that later constrains generosity.

Publicly traded securities are often the most tax-wise for many donors

Appreciated stocks and ETFs can increase what reaches ministry

For many donors, contributing long-term appreciated publicly traded securities—individual stocks, mutual funds, and ETFs—is the most efficient way to fund a donor-advised fund. The reason is straightforward: the donor may generally claim a charitable deduction for the fair market value of the asset and avoid capital gains tax on the appreciation, subject to applicable IRS limitations and personal circumstances.

In practice, this means donors can often turn the same market value into more charitable capacity than they could by selling first and giving cash. The IRS explains the general treatment of charitable contributions in Publication 526.

Governance and timing questions donors should not ignore

Stock gifts are simple operationally, but they still involve real judgment calls. Concentrated stock positions can create outsized risk if held too long; donors and sponsors sometimes disagree about how quickly to liquidate. If you are funding a donor-advised fund in a volatile market season, your giving plan should not depend on a single day’s price.

There is also a moral dimension to investment holdings that sophisticated Christian donors take seriously. Christians genuinely disagree about the best approach to faith-aligned investing—screening, engagement, or a more limited emphasis on investment ethics in favor of grantmaking outcomes. A donor-advised fund can accommodate different approaches, but it cannot remove the responsibility to think clearly about the witness of one’s holdings and the integrity of one’s grantmaking.

Complex assets can fund a donor-advised fund, but they require discernment

Real estate, privately held business interests, and restricted property

Many donor-advised funds can accept non-cash, non-publicly traded assets, though policies vary significantly by sponsor. Common examples include real estate, privately held C-corp or S-corp shares, interests in LLCs or partnerships, restricted stock, and certain alternative investments. These gifts can be powerful, especially around business transitions or estate planning, but they are rarely simple.

Complex assets raise questions of valuation, marketability, environmental or legal liability, and time to liquidation. A sponsor may require a qualified appraisal and may decline assets that create undue risk or administrative burden. For donors, the most important discipline is to keep the gift’s complexity from consuming energy that should be directed toward actual charitable impact.

Non-cash gifts must serve the ministry, not the donor’s convenience

Some donors are tempted to contribute “difficult” assets because they are hard to sell or emotionally burdensome to unwind. A Christian donor-advised fund is not a disposal mechanism; it is a charitable instrument. The asset should be something the sponsor can receive responsibly and convert into charitable capacity without hidden costs that effectively reduce the value of the gift.

When the asset is complex, we recommend building a short decision grid before proceeding:

- Can the sponsor accept this asset under its written policy?

- Is there a clear and timely path to liquidation or productive use?

- Are there credible valuation and appraisal pathways?

- Does the asset introduce legal, environmental, or reputational risk?

- Will processing costs meaningfully reduce what reaches ministry?

Donors who treat these questions as spiritual stewardship rather than mere process tend to give with greater clarity and less regret.

Align the funded assets with ministries you can trust

A donor-advised fund does not solve the trust problem

A donor-advised fund can simplify giving, improve tax efficiency, and create space for deliberate grantmaking. It cannot verify whether a ministry is theologically grounded, financially honest, or governed with integrity. That question remains, and it has become more pressing as donors face growing volumes of appeals, emotionally charged storytelling, and uneven transparency across the Christian nonprofit landscape.

Across our verification work at Most Trusted, we observe that the ministries that meet The Most Trusted Standard tend to treat donor trust as a sacred obligation rather than a marketing problem. They document program outcomes candidly, avoid manipulative fundraising, maintain meaningful board oversight, and present financial reporting that does not require donors to guess where funds go.

Let the asset choice serve a disciplined giving practice

Asset selection and ministry selection should reinforce each other. If you are contributing appreciated securities because you want to increase charitable capacity, it follows that you should apply equal seriousness to where that capacity goes. The New Testament’s insistence on honesty, accountability, and tested character is not confined to personal ethics; it bears directly on institutional stewardship.

For donors mapping out practical approaches and trade-offs, our coverage of Giving Strategies Using Christian Donor-Advised Funds addresses how different funding choices support different giving goals, including recurring grants, multi-year commitments, and season-of-life planning.

FAQs for What assets can fund a Christian donor-advised fund

Can we fund a Christian donor-advised fund with cryptocurrency?

Some donor-advised fund sponsors accept cryptocurrency, typically by receiving the asset, liquidating it, and crediting the proceeds to the fund. Policies differ, and donors should expect heightened compliance review and potential minimums. The IRS treats virtual currency as property for federal tax purposes, which shapes the general logic of donating appreciated property rather than selling first; the IRS position is outlined in IRS guidance on virtual currencies. Because sponsor acceptance, valuation methods, and timing can vary, donors should confirm the sponsor’s written crypto policy before initiating a transfer.

Can we contribute life insurance or retirement assets to a donor-advised fund?

Retirement assets generally pass through beneficiary designations, and many donors name charities as beneficiaries because qualified retirement accounts can be tax-inefficient to leave to heirs. Life insurance can sometimes be donated or used in charitable planning, but donor-advised fund sponsors vary widely in what they will accept and how they administer such gifts. These are areas where legal and tax counsel are particularly important, because the planning mechanics can be complex and the consequences can be difficult to reverse.

A disciplined funding plan is part of faithful giving

What assets can fund a Christian donor-advised fund is ultimately a question about readiness: readiness to give with intention, readiness to simplify what should be simple, and readiness to bring both wisdom and conviction to the material resources God has entrusted. Cash and publicly traded securities cover most donors’ needs, while complex assets can be appropriate when the gift is truly charitable in purpose and responsibly administrable.

When the funding choice is paired with careful ministry selection, a donor-advised fund can support a giving life marked by steadiness rather than impulse. That steadiness is not merely financial prudence. It is one way Christians honor the Lord with their wealth and direct more of it, over time, toward work that is worthy of trust.