Tax-smart giving is one of the few places where Christian donors can increase ministry impact without increasing spending. Done well, it is simply stewardship: arranging our affairs so that more of what we have been entrusted with moves toward the work of the Kingdom, rather than unnecessarily toward the tax bill.

The stakes are not merely financial. Scripture treats money as a spiritual diagnostic because it reveals what we trust, what we fear, and what we value (Matthew 6:21). At the same time, tax law is not a discipleship curriculum, and wise donors must resist the temptation to let a deduction become the reason for a gift. The order matters: we give because Christ has given himself for us; tax planning is a tool that can help our giving travel farther.

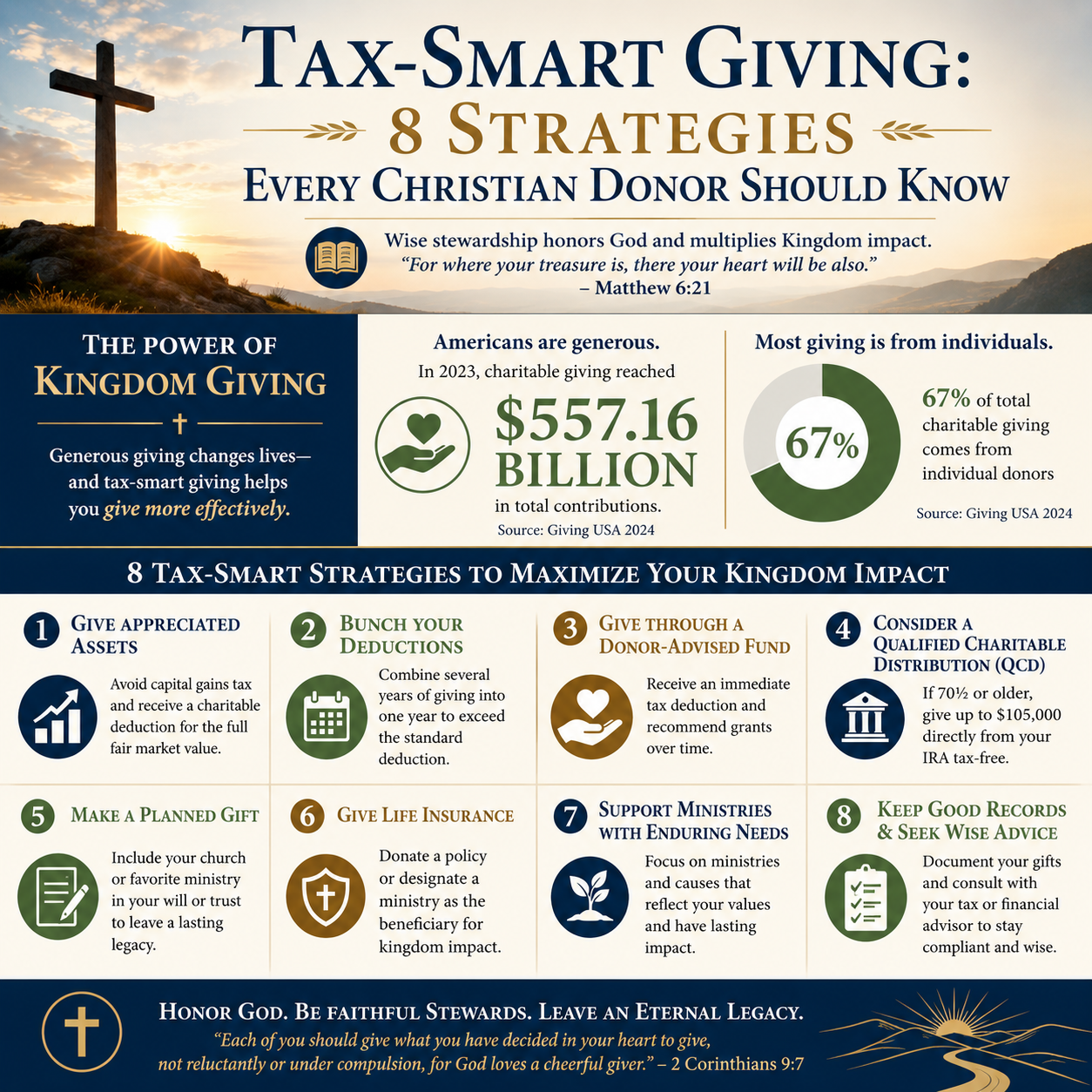

Eight strategies consistently serve serious Christian givers well: giving appreciated assets, using donor-advised funds carefully, bunching itemized deductions, directing required distributions, aligning giving with estate plans, funding charitable trusts when appropriate, giving from business interests with proper diligence, and building documentation and governance discipline into every gift. Each strategy has benefits and trade-offs, and the strongest approach is integrated: tax planning, ministry due diligence, and theology of stewardship working together.

Begin with the spiritual and the legal before the tactical

Tax-smart giving starts with two commitments that protect donors and ministries alike. First, giving remains worship and obedience, not a financial maneuver (2 Corinthians 9:7). Second, tax law must be handled precisely. The Internal Revenue Service has tightened substantiation and appraisal expectations over time, and the fastest way for a well-intentioned donor to create needless risk is to treat these rules as informal.

What this means in practice is that we should plan gifts in a way that is both theologically ordered and administratively clean. Generosity that creates confusion, pressure, or ambiguous restrictions often burdens the very ministries it intends to strengthen. The mature donor aims for gifts that are mission-aligned, properly documented, and realistic for the recipient to administer.

Across our verification work at Most Trusted, we observe that ministries with strong financial controls and transparent reporting tend to receive complex gifts more smoothly. They know how to receipt properly, how to communicate restrictions clearly, and how to avoid the quiet mission drift that can occur when funding becomes overly complicated.

Strategy 1 and 2: Give appreciated assets and use donor-advised funds with intention

For many donors, the largest tax efficiency gains come not from changing the amount given, but from changing the asset given. Cash is simple, but it is not always the most tax-wise instrument.

1. Donate appreciated securities instead of cash

When we give publicly traded stock that has appreciated in value and has been held long enough to qualify for long-term capital gains treatment, we can often avoid capital gains tax while still claiming a charitable deduction for the fair market value, subject to IRS limitations. This is a common strategy for donors who have significant taxable investment accounts and a consistent pattern of giving.

The pastoral wisdom here is straightforward: if the same gift can be made with fewer tax costs, we are freeing capital for additional generosity or other faithful obligations. The tactical wisdom is equally important: transfer mechanics, timing, and documentation matter, and the recipient ministry must be able to receive and liquidate securities responsibly.

2. Use a donor-advised fund to separate the tax year from the ministry timetable

A donor-advised fund, or DAF, allows donors to contribute in one tax year (potentially taking the deduction then) while recommending grants to ministries over time. For donors with fluctuating income, a liquidity event, or a desire to give thoughtfully without rushing, that separation can be valuable.

Christians genuinely disagree about DAFs because they can be used in two very different spirits. They can be a disciplined way to plan long-term generosity, or they can become a warehouse of charitable intent that never reaches the field. Many DAF sponsors encourage granting, and some donors build personal policies to distribute a defined percentage each year. The point is not perfection; it is preventing drift from generosity into indefinite holding.

Strategy 3 and 4: Time deductions wisely and direct required distributions

The tax code rewards itemizing deductions, but many households take the standard deduction in most years. That does not mean giving becomes tax-inefficient; it means timing matters.

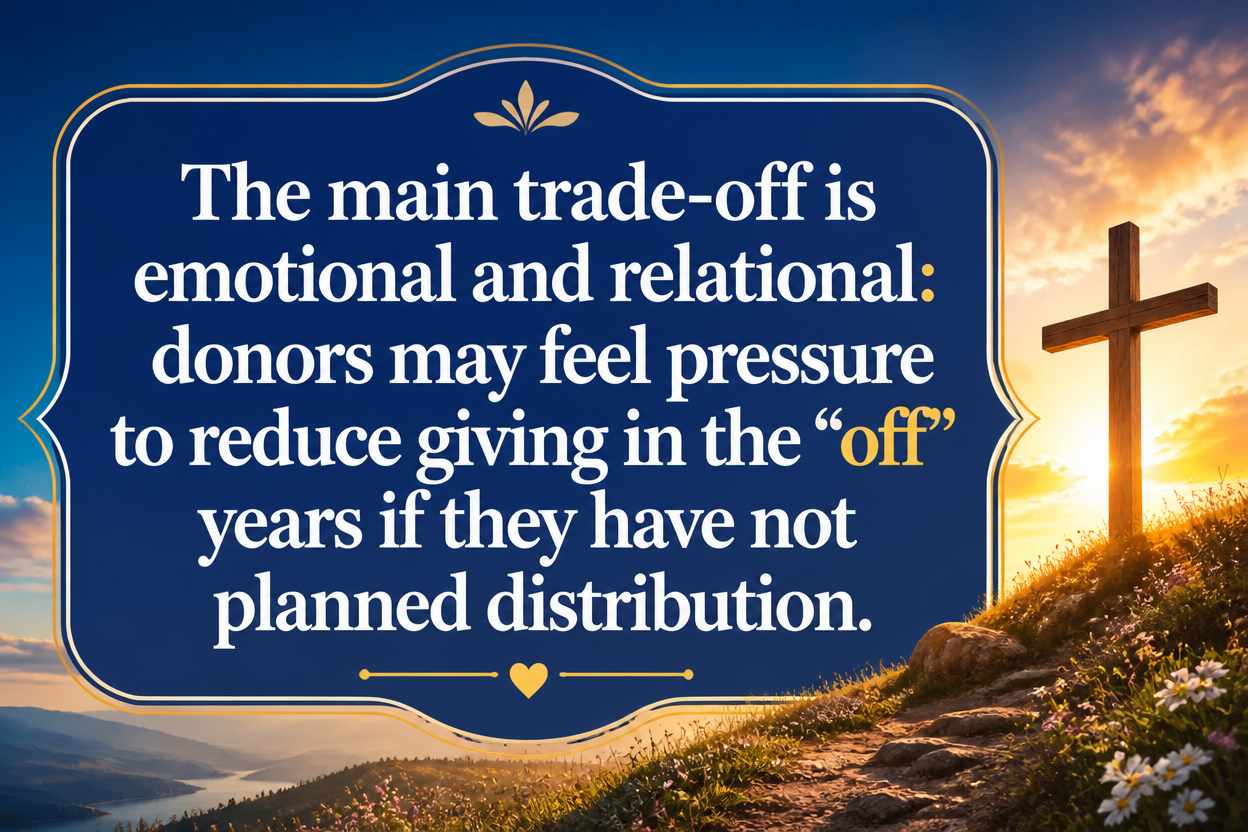

3. Bunch giving to exceed the standard deduction in selected years

Some donors concentrate multiple years of charitable giving into one year to cross the threshold for itemizing deductions, often pairing this with a DAF to maintain steady support for ministries in subsequent years. This approach can reduce taxable income in a high-income year while keeping ministry funding stable.

The main trade-off is emotional and relational: donors may feel pressure to reduce giving in the “off” years if they have not planned distribution. A DAF can help, but the deeper discipline is deciding that tax strategy will serve generosity, not govern it.

4. Use qualified charitable distributions if you are over the eligible age

For donors who are eligible, a qualified charitable distribution, or QCD, allows certain gifts to be made directly from an IRA to a qualified charity. This can be especially valuable because it may reduce taxable income by satisfying required minimum distribution obligations without counting the distribution as income in the first place. This is a different benefit than an itemized deduction, and for some households it can be meaningfully more efficient.

Because QCD rules are specific and the mechanics require direct transfer to the charity, donors should coordinate carefully with the IRA custodian and the receiving ministry. Ministries that handle receipting and designation clearly reduce the risk of administrative errors that create frustration at tax time.

Strategy 5 and 6: Put generosity into your estate plan and consider charitable trusts carefully

Many Christians intend to be generous at death but never formalize those intentions. Estate planning is not merely about protecting heirs. It is also a chance to set a coherent legacy that reflects what we believe the world is for.

5. Name ministries in your will, trust, or beneficiary designations

Bequests can be structured in several ways: a specific dollar amount, a percentage of the estate, a residuary gift, or beneficiary designations on accounts such as IRAs or life insurance policies. Each has distinct implications for flexibility and for how an estate handles market fluctuations.

A mature approach includes two safeguards. First, confirm the ministry’s legal identity and current standing. Second, articulate restrictions with care. Highly restrictive bequests can force ministries into awkward choices, especially if programs evolve. Many of the healthiest ministries can honor donor intent precisely because they communicate clearly about what they can and cannot promise long term.

6. Consider charitable remainder trusts or charitable lead trusts for complex situations

For donors with concentrated wealth in appreciated assets, charitable trusts can sometimes provide a blend of philanthropic and family outcomes. A charitable remainder trust may provide income to the donor or other beneficiaries for a term, with the remainder going to charity. A charitable lead trust can direct income to charity for a period, with remaining assets going to heirs. These structures are not “better giving.” They are tools for particular circumstances.

The harder question is whether the complexity serves the mission and the family faithfully. Charitable trusts carry legal costs, administrative demands, and long-term assumptions. They should be pursued with capable counsel and with the humility to prefer a simpler gift when the additional structure is not clearly warranted.

Strategy 7 and 8: Give from business interests thoughtfully and keep documentation disciplined

Some of the most significant giving in the American church comes from business owners and families with private assets. These gifts can be powerful, and they can also create unintentionally high risk if donors and ministries treat them casually.

7. Explore giving from business interests with rigorous valuation and governance

Donating closely held business interests, private equity, or other non-cash assets may offer tax advantages, but it introduces valuation and liquidity questions that are far more complex than giving publicly traded stock. A ministry must be able to receive such assets legally and responsibly, and the donor must meet substantiation and appraisal requirements.

This is also an area where governance matters. Across the nonprofit sector, the strongest boards anticipate complex gifts by establishing gift acceptance policies and conflict-of-interest safeguards. Christian ministries are not exempt from these best practices; if anything, our public witness requires a higher standard of clarity and integrity.

8. Treat receipts, appraisals, and restrictions as spiritual discipline, not paperwork

Tax-smart giving collapses quickly when documentation is sloppy. Receipts must reflect what was actually given, and donors must not receive impermissible benefits in exchange for a deductible gift. Non-cash gifts may require qualified appraisals, and timelines can matter. These are not merely compliance concerns. They are part of honest dealing.

We recommend that significant givers maintain a repeatable internal process: confirm the ministry’s charitable status, clarify any restrictions in writing, obtain acknowledgments promptly, and keep records centralized. Ministries that operate with transparency and tested financial controls make this easier for donors. That is one reason verification is not a luxury for Christian philanthropy; it is a practical guardrail.

How to apply these strategies without funding weak ministries

Tax efficiency can create a subtle temptation: to treat the recipient as interchangeable. Mature Christian giving rejects that. The recipient matters because the mission matters, and because accountability is part of love for neighbor. A tax-advantaged gift to an ungoverned or opaque ministry is not wise stewardship.

In our work at Most Trusted, we evaluate ministries against The Most Trusted Standard, a 15-criteria framework spanning four domains: Faith Foundation, Financial Integrity, Governance and Leadership, and Transparency and Effectiveness. Tax-smart giving is most powerful when it is paired with ministry-smart giving. The donor who gives appreciated assets to a ministry with weak controls may still reduce taxes, but the Kingdom outcome becomes harder to defend.

What to scrutinize before making complex gifts

Financial integrity and controls. Does the ministry publish audited financial statements when appropriate for its size and complexity? Are related-party transactions disclosed? Are fundraising costs and program costs described clearly rather than obscured by marketing language?

Governance and leadership. Is there a functioning, independent board with meaningful oversight? Are conflicts of interest managed? Is the founder’s authority bounded by accountable structures?

Transparency and effectiveness. Does the ministry communicate outcomes credibly, avoiding both triumphalism and vagueness? Are financials, leadership, and program claims consistent across public reporting?

How to preserve donor intent without harming the ministry

Restrictions can be righteous when they protect mission fidelity. They can also be damaging when they force ministries into narrow, unstable funding. We recommend clarity and realism: define the purpose, confirm that the ministry can execute it, and allow reasonable flexibility for program evolution. A restricted gift that cannot be implemented faithfully often becomes an administrative burden that drains resources from the very people the donor intended to serve.

How to avoid the common failure modes

Substituting tax logic for discernment. The best tax strategy does not redeem a poor ministry choice. Verify the ministry with the same seriousness with which you verify the tax mechanics.

Overcomplicating the gift. Complexity is justified only when it clearly increases long-term generosity or mission effectiveness. Complexity for its own sake tends to enrich advisors more than beneficiaries.

Neglecting family formation. For many Christian households, the deeper work is not a sophisticated vehicle but a coherent family practice of generosity. Estate gifts and trusts can be part of formation, but only if the family understands the theological rationale, not merely the legal structure.

FAQs for Tax-Smart Giving: 8 Strategies Every Christian Donor Should Know

Is tax-smart giving spiritually compromised or less faithful?

No. Scripture commends wisdom and faithful management of resources, and the church has long recognized prudence as a moral good when ordered toward love of God and neighbor. The spiritual danger is not planning; it is allowing tax benefit to become the motive or allowing efficiency to replace discernment about the ministry’s integrity.

Should we stop giving cash and only give appreciated assets?

Not necessarily. Many ministries need predictable cash flow, and some donors do not hold appreciated assets in taxable accounts. A balanced approach often works well: maintain consistent cash giving for regular support while using appreciated assets for larger gifts when feasible.

Do donor-advised funds reduce accountability because money can sit idle?

They can, depending on donor practice. A DAF is a tool, not a moral category. Donors who establish a clear granting policy and who remain attentive to ministry needs can use DAFs to give more thoughtfully and more generously. Donors who use a DAF to postpone actual generosity should treat that as a spiritual concern, not merely a philanthropic one.

How can we ensure a complex gift does not create administrative burden for a ministry?

Start by asking whether the ministry has the operational capacity and governance to receive the asset. Confirm gift acceptance policies when applicable, clarify restrictions in writing, and coordinate timing so the ministry can receipt and process the gift properly. When a ministry is transparent, financially disciplined, and well governed, the gift is more likely to bless rather than strain the organization.

Tax strategy is strongest when it serves worshipful stewardship

Tax-smart giving is not a substitute for generosity, and it is not a shortcut around discernment. It is a form of stewardship that can increase the resources available for ministry when applied carefully and in proper order. The Christian donor’s aim is not merely to give efficiently, but to give faithfully: to support ministries worthy of trust, to strengthen the church’s witness, and to direct more of what God has entrusted to us toward the works of mercy and proclamation that Scripture commends.