How to give to Christian financial service ministries is ultimately a stewardship question: whether our money will be treated as a tool for neighbor-love under Christ’s lordship, or as a private instrument of control and security. Because these ministries sit at the intersection of discipleship and personal finance, the practical details matter—fees, lending terms, compliance, donor restrictions, and reporting—alongside spiritual intent.

The field is also complicated. Some Christian financial service ministries operate like charities with donor-supported programming. Others function more like financial institutions or member organizations that may include religious purpose, but rely on capital, interest, or service revenue. Christians genuinely disagree about where to draw lines between “ministry” and “financial product,” and reasonable donors will weigh those questions differently. What we can do, as a matter of integrity, is give in ways that are transparent, accountable, and consistent with biblical ethics.

Begin with a Christian account of money and the kind of ministry you are funding

Scripture treats money as spiritually potent: a rival master (Matthew 6:24), a test of faithfulness (Luke 16:10–13), and a means of mercy (2 Corinthians 8–9). Christian financial service ministries typically form people and institutions around one of three aims: (1) financial discipleship and education, (2) relief from predatory or crushing debt, or (3) capital access for families, churches, and mission-aligned enterprises. Those aims are not interchangeable, and donors should name which problem they are trying to address.

Across our verification work at Most Trusted, the healthiest donor-ministry relationships begin with clarity about what is being funded. A ministry may be addressing a genuine need—such as avoiding exploitative lending—or it may be offering a faith-branded version of what the market already provides. The donor’s task is not cynicism, but discernment: to understand the ministry’s theory of change, its economic model, and its moral commitments.

Distinguish charitable gifts from capital participation

A donation is a gift: you relinquish control for the sake of a mission, typically with tax-deductible treatment when made to a qualified 501(c)(3). Capital participation is different: deposits, notes, loan funds, or investment-like vehicles can carry repayment expectations, liquidity constraints, and risk. Some Christian financial ministries offer both, and the same website can present them with similar spiritual language. Mature giving asks a simple question: “Is this a contribution to a charitable purpose, or is it a financial instrument?”

For donors who want to understand tax treatment, the IRS overview of charitable contributions provides a baseline on what is deductible and what is not, including the requirements for a qualified organization and proper documentation (IRS).

Ask whether the ministry’s financial model reinforces dignity

Not every “help” is dignifying help. The When Helping Hurts framework, articulated by Steve Corbett and Brian Fikkert, has shaped a generation of Christian development thinking by warning against aid that unintentionally weakens local agency and reciprocal responsibility (When Helping Hurts). Financial services are particularly susceptible to this tension: rescue can become dependency, and empowerment can become abandonment if the ministry withdraws relational support.

Practically, donors can look for programs that combine financial assistance with durable formation: budgeting, coaching, accountability structures, and church-based community. The question is not whether a ministry “believes in responsibility,” but whether it has designed systems that actually cultivate it without coercion or shame.

Evaluate trustworthiness with evidence, not sentiment

Christian donors often feel an understandable pull toward ministries that speak their language. But shared vocabulary is not shared accountability. Many of the failures that have harmed Christian witness in the last two decades did not begin with overt doctrinal denial; they began with weak governance, conflicted boards, opaque finances, and spiritualized leadership cultures that resisted scrutiny.

Most Trusted exists because donors deserve more than assurances. We evaluate ministries against The Most Trusted Standard, a 15-criteria framework across four domains: Faith Foundation, Financial Integrity, Governance and Leadership, and Transparency and Effectiveness. The point is not to impose a single style of ministry, but to identify verifiable markers that a donor can reasonably trust.

Watch for governance structures that can withstand pressure

Financial service ministries face recurring pressure points: borrower defaults, fraud risk, conflicts of interest, and reputational incentives to tell only success stories. Strong boards and documented policies are not bureaucratic obstacles; they are safeguards for the vulnerable and for the gospel’s credibility.

In practice, donors should look for clear board independence, meaningful financial oversight, documented conflict-of-interest policies, and audited financials when the organization’s size warrants it. If a ministry cannot explain who holds leadership accountable, it is asking you to underwrite a trust gap with your generosity.

Resist simplistic overhead assumptions and demand clarity instead

Christians sometimes treat “low overhead” as synonymous with faithfulness. The sector has had to reckon with how misleading that can be. The Overhead Myth letter—signed by Charity Navigator, Candid (formerly GuideStar), and the BBB Wise Giving Alliance—warns donors not to overemphasize overhead ratios and instead to consider governance, transparency, and results (Charity Navigator).

What this means in practice is not that overhead is irrelevant. It is that donors should ask better questions: Are staff trained to handle sensitive financial and pastoral situations? Does the ministry invest appropriately in compliance, data security, and internal controls? Does it report outcomes in ways that can be checked?

Seek transparency appropriate to the kind of financial work being done

Transparency for a food pantry and transparency for a lending ministry are not identical. Financial services bring privacy concerns and regulatory constraints. But donors can still expect meaningful disclosure: how funds are used, how risks are managed, what fees exist, and what accountability mechanisms govern client-facing decisions.

Before giving, donors should read Form 990s when available, review audited statements when provided, and test whether the ministry explains its model plainly. When the only available information is promotional, donors should slow down until they can obtain primary-source documentation.

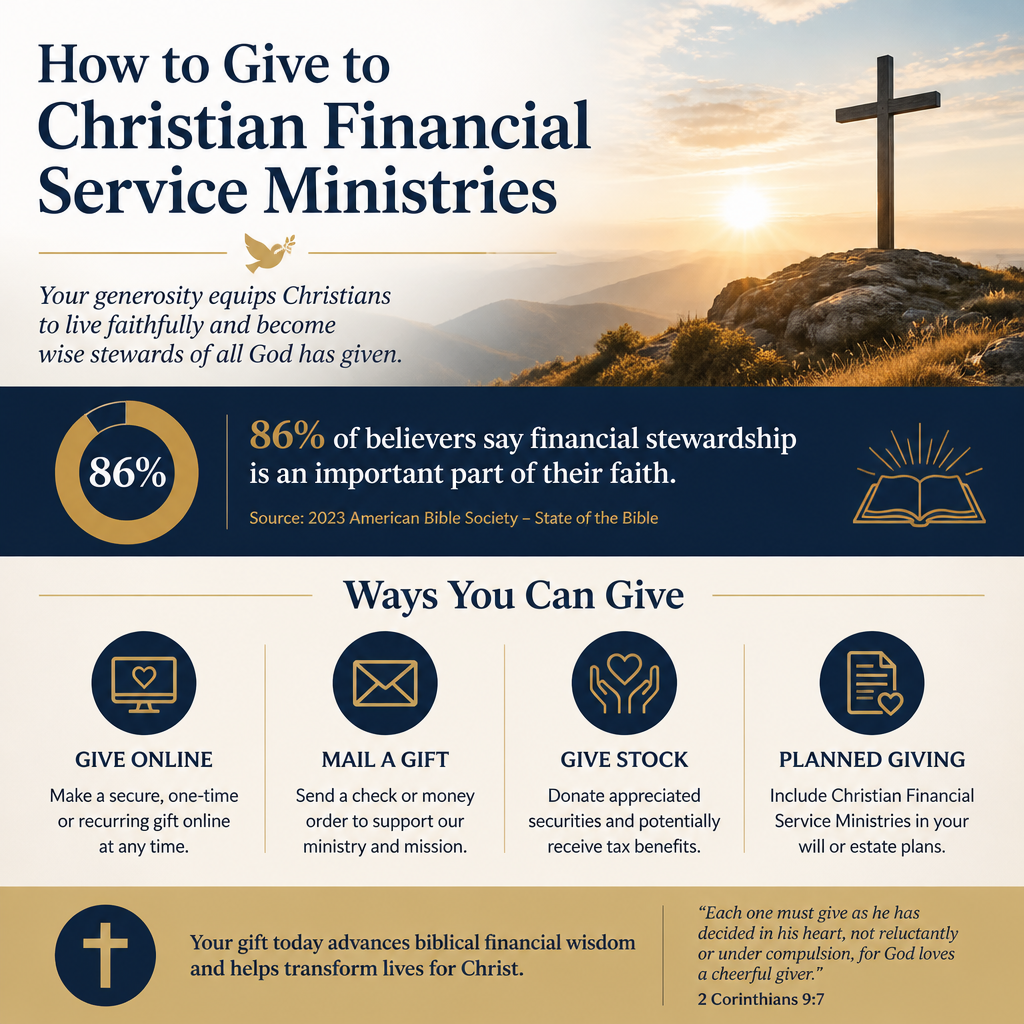

Choose a giving method that matches the ministry’s economics and your stewardship goals

Different forms of giving create different kinds of stability. Christian financial service ministries often run programs where continuity matters: counseling relationships, long-term debt repayment plans, capital reserves, and financial literacy cohorts. The more a ministry’s work depends on multi-month engagement, the more valuable reliable funding becomes.

Donors should also be candid about their own constraints. Not every household can give monthly. Not every donor should contribute appreciated stock. Not every estate plan needs a charitable component. Faithful stewardship is not uniformity; it is obedience in context, grounded in prudence and generosity.

Monthly giving can underwrite long-term formation

Recurring gifts are particularly aligned with ministries that provide ongoing coaching, counseling, or community-based programs. A steady stream of support can reduce the pressure to chase short-term fundraising spikes and can help leadership plan staffing and program capacity with fewer abrupt contractions.

For donors, monthly giving also clarifies intention. It converts a moment of compassion into a sustained posture of responsibility. That is often closer to the New Testament pattern of shared life than sporadic crisis-response alone (Acts 2:44–47).

One-time gifts can fund infrastructure and expansion, but should be designated carefully

One-time gifts are appropriate for matching campaigns, emergency assistance funds, technology upgrades, and new program launches. They can also create distortions when donors require a ministry to grow faster than its governance and controls can support. Designation is sometimes wise, but donors should avoid imposing restrictions that force an organization into accounting gymnastics or mission drift.

A disciplined approach is to ask the ministry what it would fund if it had an additional, non-restricted gift, and then evaluate whether that use aligns with your priorities and the ministry’s stated strategy.

Stock gifts and donor-advised funds can strengthen tax-wise generosity

For donors with appreciated assets, giving stock can be an efficient way to support ministry while potentially avoiding capital gains taxes and receiving a charitable deduction when eligible. Donor-advised funds can simplify multi-year giving and can be particularly useful for donors who want to bunch giving in high-income years while distributing grants over time. Fidelity Charitable’s overview offers a clear explanation of how donor-advised funds work and how grants are recommended to charities (Fidelity Charitable).

Financial service ministries sometimes have additional compliance steps for complex gifts, and donors should expect that. What matters is whether the ministry can explain timelines, receipting, and any limitations without confusion or pressure.

Ask questions that honor both spiritual intent and fiduciary reality

Christian donors should not be embarrassed to ask hard questions. Love “rejoices with the truth” (1 Corinthians 13:6), and financial ministry work is full of places where unclear claims can become spiritual manipulation. The goal is not suspicion; it is sober-minded care for the people a ministry serves and for the integrity of Christian witness.

We recommend a due-diligence posture that matches the scale of your giving. A modest gift may warrant a modest review. A major gift, a planned gift, or a large DAF relationship should come with deeper inquiry, written documentation, and clarity about reporting expectations.

Core questions to ask before you give

- What exactly is the ministry’s service? Education, coaching, debt relief, lending, investment participation, or a blend?

- How is the work funded? Donations, fees, interest income, grants, or capital instruments? What incentives does that create?

- Who is accountable? How does the board oversee leadership? Are conflicts of interest disclosed and managed?

- How are outcomes measured? What does “success” mean—reduced delinquency, increased savings, sustained budgeting habits, restored relationships—and how is it verified?

- How are clients protected? What safeguards exist against coercive practices, privacy breaches, or spiritually manipulative fundraising?

Planned giving belongs in this conversation

For donors thinking beyond annual giving, planned gifts can be a faithful expression of long obedience. Christian financial service ministries may be well positioned to receive bequests when their mission is enduring and their governance is stable. The caution is that planned giving intensifies the trust question: you are not only supporting current work; you are endorsing a ministry’s long-term future.

That is where verification becomes particularly valuable. A ministry that meets The Most Trusted Standard tends to show durable signs of institutional health: doctrinal clarity without novelty, controls that reduce misuse of funds, governance that withstands leadership transitions, and public-facing transparency that treats donors as adults rather than as marketing targets.

Do not confuse financial sophistication with spiritual maturity

Some ministries speak with impressive financial vocabulary and still operate with thin theological grounding or weak ecclesial accountability. Others are deeply pastoral but underdeveloped in risk management. Donors should not romanticize either side. The best ministries hold competence and character together.

For donors seeking a broader sense of the landscape, our research across Christian Financial Service Ministries is designed to help you compare organizations with consistent criteria and verifiable documentation.

Giving that strengthens trust and strengthens the church

Christian financial service ministries can be a quiet force for good: freeing families from destructive debt, forming habits of stewardship, and providing ethical alternatives to exploitative systems. They can also become places where money-talk eclipses discipleship, or where organizational opacity harms the very people the ministry claims to serve.

How to give well, then, is not merely a question of which tool you choose—monthly, one-time, stock, DAF, or planned giving. It is whether your generosity is joined to truth: clear purpose, accountable governance, transparent reporting, and theological seriousness about what money does to the soul. That kind of giving does not only fund programs; it strengthens trust in the church’s public witness.