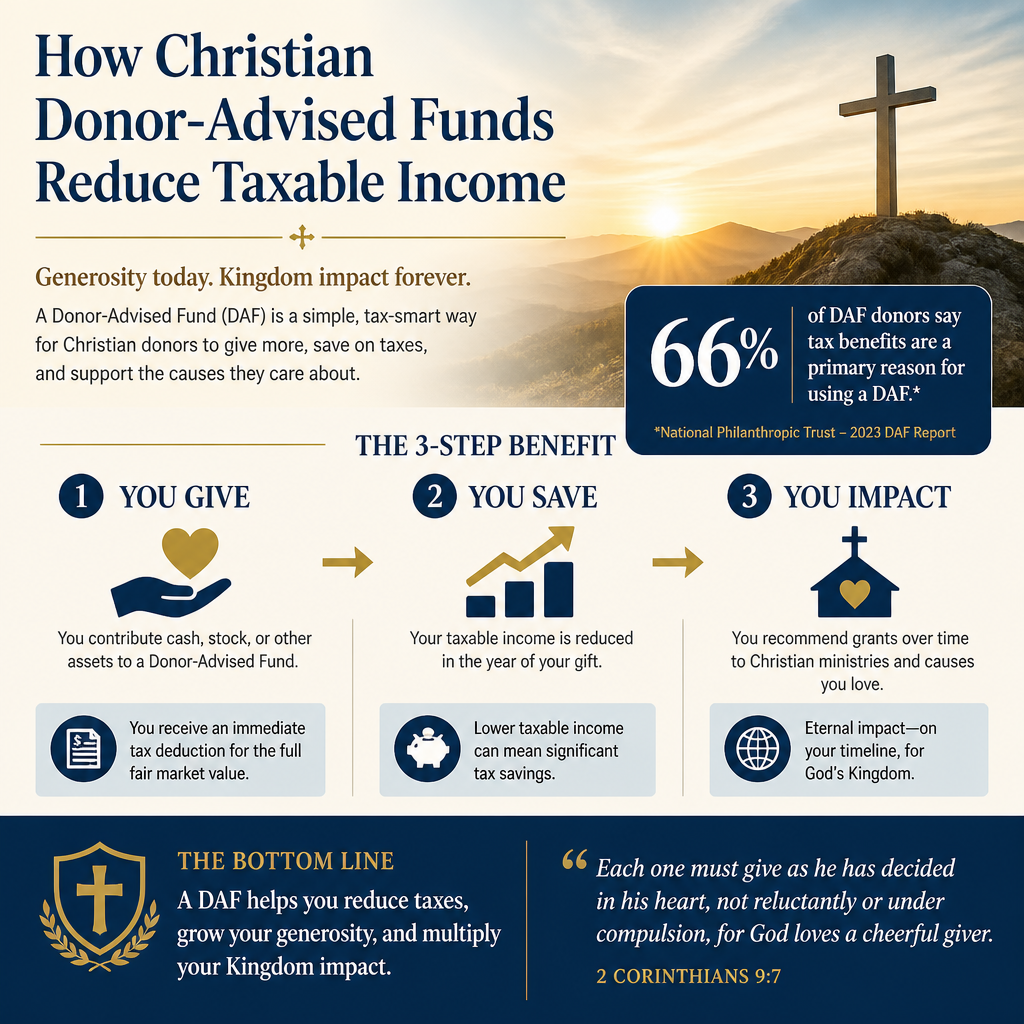

How Christian donor-advised funds reduce taxable income is not a peripheral question for serious stewards; it sits at the intersection of discipleship, compliance, and long-horizon generosity. A donor-advised fund can create a legitimate tax deduction in the year of the contribution while allowing charitable distributions to be made over time, but its usefulness depends on how the gift is structured, what is contributed, and whether the donor’s larger tax picture makes the deduction meaningful.

Scripture never treats tax reduction as a moral end in itself. Yet it does treat stewardship as a moral obligation. Jesus’ parable of the talents assumes that faithful servants think carefully about what is entrusted to them, not impulsively or negligently. A well-governed donor-advised fund can serve that purpose when it supports thoughtful giving, disciplined recordkeeping, and a sober posture toward legal and ethical boundaries.

1 The tax mechanics of a Christian donor-advised fund

A donor-advised fund is a charitable vehicle, not a private account

A donor-advised fund is maintained and operated by a sponsoring organization, typically a public charity. When a donor contributes to a donor-advised fund, the contribution is generally treated as a completed charitable gift to that public charity. The donor retains advisory privileges over future grants, but not legal control of the assets. That distinction matters: the tax deduction follows the completed gift to the public charity, not the later grant recommendations.

For Christian donors, this structure often creates a disciplined separation between the moment of giving and the later discernment about where to distribute. The strength of the model is also its temptation: a donor can feel as though the funds remain “theirs” because they can advise on distributions. A mature donor treats the advisory role as stewardship under a charity’s governance, not as continued ownership.

The deduction depends on itemizing and on the type of gift

Most donors only realize a federal income tax benefit from charitable contributions if they itemize deductions rather than take the standard deduction. The Internal Revenue Service explains itemized deductions and the standard deduction framework in its guidance for individuals at IRS.gov. What this means in practice is that a donor-advised fund may be most impactful in years when giving is “bunched” into one tax year to exceed the standard deduction, especially for households with relatively stable charitable intentions but uneven income events.

The deduction rules also vary by the type of asset contributed. A cash gift is straightforward. A gift of long-term appreciated securities can be particularly tax-efficient because the donor may avoid capital gains tax on the appreciation while also receiving a charitable deduction, subject to applicable limits and substantiation rules. The IRS’s charitable contributions guidance includes the governing rules and documentation expectations at IRS.gov.

2 Timing and bunching strategies that meaningfully reduce taxable income

Why timing matters more than many donors expect

A donor-advised fund can reduce taxable income in the year the contribution is made, not the years when grants are distributed to ministries. This is often the central planning advantage. Many Christian households give steadily each year, but their income is not steady. Business owners may have a strong year. Employees may receive a large bonus. A family may realize significant capital gains from selling appreciated stock or property. In those moments, contributing to a donor-advised fund can shift a portion of that year’s taxable income into a charitable deduction.

The harder question is whether the donor’s pattern of giving and the household’s broader deductions justify itemizing. If not, the spiritual discipline of generosity can still be pursued, but the incremental tax benefit may be minimal. This is not a failure of the donor-advised fund; it is simply the reality of the tax code’s structure.

Bunching charitable deductions through a donor-advised fund

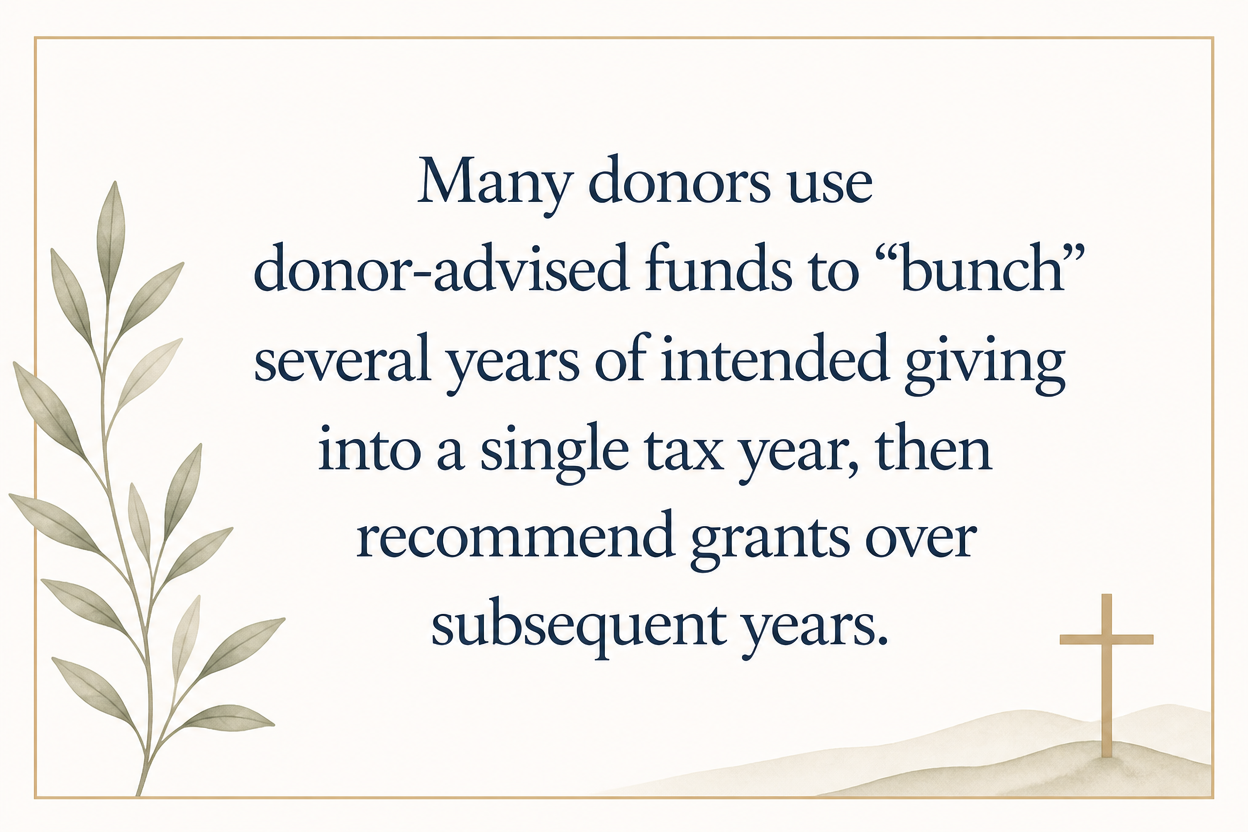

Many donors use donor-advised funds to “bunch” several years of intended giving into a single tax year, then recommend grants over subsequent years. Fidelity Charitable describes this common use and the mechanics of bunching at FidelityCharitable.org. The concept is simple: concentrate deductions into a year when they are most valuable, then preserve a measured, prayerful grantmaking pace that aligns with a church or ministry’s actual needs and the donor’s discernment.

This approach often resonates with Christian donors who want to avoid reactive giving driven by fundraising cycles. A donor-advised fund can create a planned reserve for generosity while still requiring the donor to make deliberate decisions about each grant.

- High-income year planning when bonuses, business distributions, or capital gains raise taxable income

- Multi-year pledge fulfillment by funding the donor-advised fund in one year while granting over time

- Year-end giving discipline by separating the act of charitable contribution from the pressure of last-minute appeals

- Family generosity formation by creating a structured way to discuss grants without treating giving as an afterthought

- Reduced administrative burden through consolidated receipts and centralized recordkeeping from the sponsor

3 What you give matters as much as when you give

Appreciated securities can reduce both income tax and capital gains exposure

For donors with appreciated stock held longer than one year, contributing the shares to a donor-advised fund can be more tax-efficient than selling the stock and giving cash. The donor may avoid recognizing capital gains on the appreciation and may receive a charitable deduction for the fair market value, within applicable limits and subject to substantiation requirements. The IRS addresses gifts of appreciated property and the related rules in its charitable contribution guidance at IRS.gov.

Many Christian donors accumulate appreciated securities in retirement or brokerage accounts without a clear plan for unwinding them. A donor-advised fund can become a disciplined outlet for giving those assets in a way that is both lawful and economically coherent, leaving more capital available for charitable purposes rather than taxes.

Complex assets demand more counsel and more restraint

Some donor-advised fund sponsors accept complex assets such as closely held business interests, real estate, or cryptocurrency. The tax implications and compliance burdens can be substantial. Valuation, unrelated business income tax concerns, and liquidation timelines can all affect whether such gifts are prudent. Christians genuinely disagree about how aggressive a donor should be in pursuing advanced charitable planning. What is not optional is integrity: the donor must be committed to accurate valuation, proper documentation, and the sponsor’s due diligence.

Because donor-advised fund contributions are irrevocable charitable gifts, donors should not treat complex-asset funding as a way to park assets during uncertainty. A donor-advised fund is not a liquidity tool. It is a charitable vehicle.

4 The ministry discernment question after the deduction is secured

Tax efficiency is not the same as ministry effectiveness

A donor-advised fund can reduce taxable income, but it cannot verify whether a ministry is faithful, well-governed, and effective. That question remains, and for serious donors it often becomes more pressing once giving is consolidated into a single charitable vehicle. When donors bunch contributions, the size of the funds under advisement can increase quickly. The consequences of weak due diligence increase with it.

Across our verification work at Most Trusted, we see that donors often assume that a well-known ministry is necessarily a well-governed ministry. The sector’s history does not support that assumption. Governance failures, weak financial controls, and opaque reporting have harmed donors and, more importantly, harmed the people ministries exist to serve.

Verification strengthens the moral clarity of giving

Our purpose at Most Trusted is to help donors give with confidence by evaluating ministries against The Most Trusted Standard, a 15-criteria framework across Faith Foundation, Financial Integrity, Governance and Leadership, and Transparency and Effectiveness. A donor-advised fund can make giving more efficient; verification helps make giving more trustworthy. Those aims belong together, especially for donors who want their generosity to be both biblically grounded and accountable.

When donors are evaluating where to recommend grants, it is often helpful to revisit the broader landscape of Christian Donor-Advised Funds so that vehicle decisions and ministry decisions remain connected rather than drifting into separate conversations.

5 Limits, trade-offs, and common misunderstandings

The deduction has ceilings, and the benefit can be smaller than expected

Charitable contribution deductions are subject to adjusted gross income limitations that vary by gift type and recipient category. Donor-advised funds are generally treated as gifts to a public charity, which can allow higher limits than gifts to certain other entities, but the specifics depend on facts and circumstances. The IRS provides the controlling rules, including percentage limitations, at IRS.gov.

What this means in practice is that a very large donor-advised fund contribution in a single year may not be fully deductible in that year, and the carryforward rules may come into play. A donor can still accomplish the charitable objective, but the taxable-income impact may be spread across multiple years.

A donor-advised fund is not a substitute for counsel, and it is not a blank check

Serious donors should expect to coordinate donor-advised fund decisions with qualified tax counsel. Certain grant recommendations are prohibited or restricted, including grants that provide more than incidental benefit to the donor. The sponsoring organization also has its own policies, review processes, and required documentation. These constraints are not an inconvenience to be worked around; they are part of the integrity of charitable giving under law.

For donors who want a deeper view of compliance questions and the boundaries of charitable planning, the category on Tax and Legal Basics of Christian Donor-Advised Funds provides additional context that can help prevent costly misunderstandings.

FAQs for How Christian donor-advised funds reduce taxable income

Does contributing to a donor-advised fund always reduce taxable income?

No. A donor-advised fund contribution generally creates a charitable deduction, but the deduction only reduces taxable income if the donor can use it. Many donors take the standard deduction rather than itemize, and charitable deductions are also subject to adjusted gross income limits. The result is that the spiritual value of giving can be present without a significant incremental tax benefit in a given year.

Can a donor-advised fund reduce taxes if we give appreciated stock?

Often, yes. When donors contribute long-term appreciated securities, they may avoid recognizing capital gains on the appreciation and may be eligible for a charitable deduction for fair market value, subject to applicable limits and substantiation requirements. The exact outcome depends on holding period, the asset type, and the donor’s broader tax situation, which is why coordination with qualified counsel matters.

A faithful approach to tax reduction through donor-advised funds

Christian donor-advised funds reduce taxable income most reliably when donors understand the mechanics: the deduction is tied to the year of contribution, depends on itemizing, and is shaped by the type of asset given and the donor’s income limitations. The deeper stewardship question is what follows after the deduction: disciplined discernment, sound due diligence, and a commitment to support ministries whose faithfulness and governance can bear scrutiny. Tax wisdom can serve generosity, but it cannot replace integrity.