How Christian donor-advised funds affect capital gains is often the difference between giving from after-tax appreciation and giving from pre-tax assets. For donors who want to fund ministry without surrendering a significant portion of growth to taxes, the capital gains treatment of donated assets is one of the most consequential features of a donor-advised fund.

That said, a Christian donor’s aim is not tax avoidance as an end in itself. Scripture does not treat Caesar’s claims lightly (Romans 13:7), and yet it commends wise stewardship and foresight (Proverbs 21:5). The question is whether a donor-advised fund can help a believer direct more of an appreciated asset’s value toward the work of the Kingdom rather than to tax friction, while still giving carefully to ministries that are worthy of that trust.

Capital gains and charitable giving are bound together

What capital gains taxation changes about generosity

Capital gains tax is triggered when an appreciated asset is sold. If a donor gives cash that came from selling a long-held stock position, real estate, or a concentrated holding, the donor may have already created a tax event. By contrast, giving the appreciated asset directly to a charitable vehicle often avoids realizing the gain at the donor level.

The details depend on whether the asset is long-term or short-term, whether the asset is publicly traded, and whether the recipient is a public charity. Donor-advised funds are typically housed within a public charity, which is why they are widely used for gifts of long-term appreciated securities.

Why this matters disproportionately for high-conviction Christian donors

Many Christian givers have a small number of ministries they support with unusual intensity: a church planting network, a pregnancy resource center, Bible translation, prison ministry, or global missions. That focus often correlates with larger gifts, irregular giving patterns tied to liquidity events, and assets that have appreciated over time.

When a donor’s giving is built around appreciated assets, the decision to donate cash versus donate the asset can meaningfully change how much support reaches ministry. The IRS rules do not make a donor righteous, but they do shape what is possible when a donor wants to be both generous and prudent.

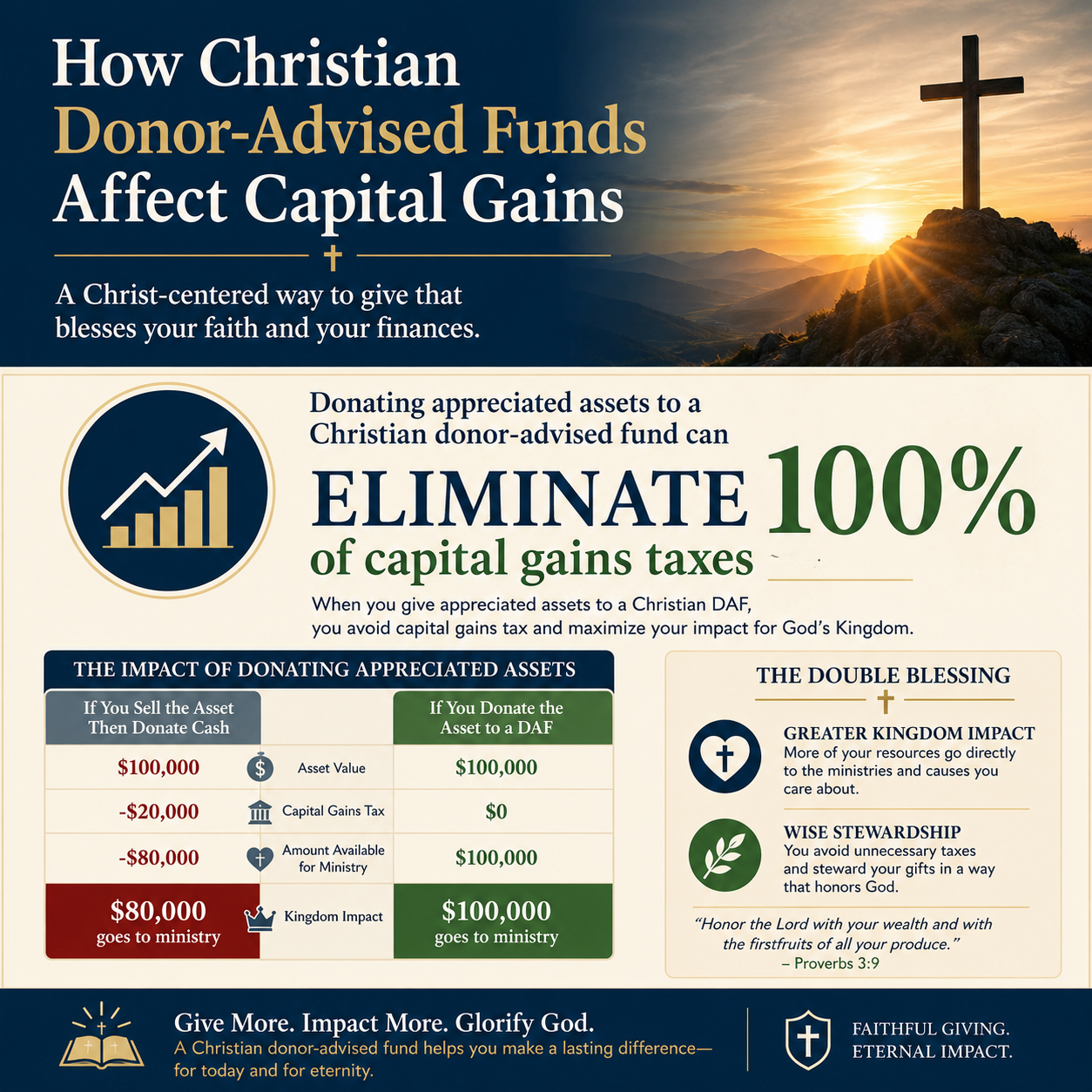

How a donor-advised fund can reduce or eliminate capital gains on donated assets

The basic mechanism for publicly traded securities

When a donor contributes long-term appreciated stock to a donor-advised fund, the donor generally receives a charitable deduction (subject to applicable AGI limits), and the fund can sell the securities without incurring capital gains tax as a taxpayer would. The practical outcome is that the full fair market value—rather than the after-tax proceeds—can be recommended onward to operating charities over time.

The IRS describes the charitable contribution rules and limits in Publication 526. For many donors, that publication is the plainest starting point for understanding how the charitable deduction interacts with gifts of property.

What changes if the asset is short-term or complex

Not all appreciation is treated equally. If the asset has been held for one year or less, the deduction is generally limited to cost basis rather than fair market value, and the capital gains advantage is often muted. Complex assets—closely held business interests, certain real estate, restricted stock, cryptocurrency in some settings—can still be given, but they introduce valuation, due diligence, and liquidity constraints that vary by sponsor.

Christian donors should be particularly cautious about assuming that every donor-advised fund sponsor will accept every asset, or that every accepted asset will be liquidated quickly. Some sponsors will decline certain gifts entirely. Others will accept but impose fees, require qualified appraisals, or delay liquidation pending legal review. The timing affects both grantmaking plans and the donor’s own tax picture for the year.

The trade-offs donors must weigh beyond the capital gains benefit

Timing, control, and the moral weight of stewardship

A donor-advised fund separates the tax deduction from the timing of grants. That can be wise when a donor has a high-income year, wants to “bunch” giving, or needs time for discernment. It can also become a way to defer actual generosity indefinitely. Christians genuinely disagree about where the line is between prudent pacing and functional hoarding, but the ethical question is real because the assets have been irrevocably given to charity while the recommendations can be delayed.

The sponsor legally controls the funds, even though most sponsors generally follow donor recommendations. Donors should read sponsor policies carefully, particularly around successor advisors, grant approval criteria, and what happens if a recommended grantee is not eligible.

Fees, minimums, and sponsor practices are not spiritually neutral

Every dollar absorbed by avoidable friction is a dollar not available to strengthen the church, serve the vulnerable, or proclaim the gospel. Fees are sometimes reasonable—administration, compliance, investment oversight—and sometimes unnecessarily high. Minimum grant sizes can constrain smaller, high-impact ministries. Investment options can raise conscience questions for Christians who care about alignment with biblical ethics.

What this means in practice is that donors should compare sponsors with the same seriousness they apply to comparing ministries. That includes reading fee schedules and evaluating whether the sponsor’s grantmaking standards serve faithful giving or merely convenience.

- Confirm whether the sponsor is a public charity and how it defines grant eligibility.

- Review the fee schedule, including administrative and investment fees.

- Ask what assets are accepted and what due diligence is required for non-cash gifts.

- Clarify policies for anonymous grants, international grantmaking, and scholarship-related requests.

- Understand succession plans and what happens if no advisor remains.

Giving with confidence requires more than tax efficiency

The temptation to let tax strategy outrun ministry due diligence

Capital gains relief can make a donor-advised fund feel like the centerpiece of faithful giving. But tax efficiency is morally thin if the downstream grants are poorly vetted. Across our verification work at Most Trusted, we observe that donors often assume that because a ministry is well-known, it is well-governed; because it is emotionally compelling, it is financially disciplined; because it is active overseas, it is accountable at home. Those assumptions can fail.

Donor-advised funds can intensify this risk because the donor experiences the “completion” of giving at the moment of contribution, while the discernment about grantees happens later. A mature process reverses the instinct: clarify the mission convictions, verify the ministries, and then use the donor-advised fund as a tool that serves those convictions.

A framework for evaluating grantees before recommending grants

Most Trusted exists to help Christian donors give with confidence by evaluating ministries against The Most Trusted Standard, a 15-criteria framework spanning faith foundation, financial integrity, governance and leadership, and transparency and effectiveness. The aim is not suspicion for its own sake. The aim is stewardship that can withstand scrutiny, protect the vulnerable, and honor the name of Christ in the public square.

Readers who want broader context on the vehicles and practices commonly used in this space can review Christian Donor-Advised Funds as a reference point for how donors typically structure giving when appreciated assets and long-term grantmaking are involved.

Common scenarios for Christian donors with appreciated assets

Concentrated stock positions and the discipline of diversification

Some donors hold a concentrated position in an employer’s stock or a single company that has appreciated substantially. Selling can create a capital gains burden and emotional hesitation. Contributing shares to a donor-advised fund can support diversification inside the charitable account while increasing the amount available for grants, assuming the shares are long-term appreciated and accepted by the sponsor.

This is not merely a financial question. Concentration risk can tempt donors to delay giving until a “better time,” which sometimes never arrives. A donor-advised fund can provide a disciplined way to convert volatility into steady ministry support.

Business exits, real estate, and the complexity donors should not rush

Liquidity events—selling a business, exercising options, selling real property—often create large gains and large giving opportunities in the same year. Donor-advised funds are frequently used in these moments, but the planning must be done before the sale is binding. Once a contract is executed, the IRS may treat the gain as already realized for the donor even if the asset is later contributed.

Because these rules are fact-specific, donors should consult qualified tax counsel. For a category-level orientation to the legal and tax issues that tend to arise, see Tax and Legal Basics of Christian Donor-Advised Funds. That context helps donors ask better questions of their advisors and avoid mistakes that are both expensive and preventable.

FAQs for How Christian donor-advised funds affect capital gains

Does donating appreciated stock through a donor-advised fund always eliminate capital gains tax?

It commonly eliminates capital gains tax at the donor level when the donor contributes long-term appreciated publicly traded securities to a donor-advised fund sponsored by a public charity, because the donor is not selling the asset. However, outcomes vary for short-term holdings, complex assets, or situations where the asset is effectively already sold. Donors should confirm the holding period, the sponsor’s status, and the sponsor’s acceptance policies, and consult a qualified tax professional for transaction-specific guidance.

Can a donor claim a deduction and still control the money in a donor-advised fund?

A donor can generally claim a deduction when the contribution to the donor-advised fund is complete and irrevocable, but the donor does not retain legal control of the funds. The donor typically retains advisory privileges to recommend grants and, in many programs, to recommend investment allocations among available options. The sponsor has final authority over grants and must ensure they meet IRS requirements. The IRS overview of donor-advised funds is a helpful reference point at IRS Charities and Nonprofits.

A faithful use of a donor-advised fund keeps the mission central

Christian donor-advised funds affect capital gains by making it more feasible to give appreciated assets without converting appreciation into taxable gain first. That advantage can strengthen long-term generosity, especially when a donor’s wealth is tied to assets rather than cash flow. The more searching question is whether the donor’s process—before and after the contribution—treats stewardship as a moral calling: giving promptly, verifying ministries carefully, and directing resources toward work that is both spiritually faithful and operationally trustworthy.